Bootstrapping SaaS in Canada is both high risk and high reward, and the outcome depends almost entirely on who you are as a founder. The upside is real: bootstrapped SaaS companies typically retain 80% or more of their equity, operate with 70-85% gross margins, and once they hit scale, grow at rates nearly matching VC-backed competitors.

Canada adds a meaningful layer of advantage through programs like SR&ED, which now offers a 35% refundable tax credit on qualifying R&D expenses up to a $6 million expenditure limit after the 2025 federal budget expansion. The risk is equally real: top-quartile bootstrapped SaaS companies reach $1M ARR in roughly two years, while median founders often take three years or more, and without external capital, every cash flow gap is a founder problem to solve.

The decision is not about whether bootstrapping works in Canada. It does. It is about whether it is the right path for your specific situation, market, and tolerance for slow, self-funded growth.

Key Takeaway:

- Bootstrapping a SaaS business in Canada can be highly rewarding because founders retain full equity, maintain strategic control, and build sustainable growth through customer revenue rather than investor capital.

- The biggest advantages include high gross margins, access to Canadian innovation incentives such as SR&ED tax credits, and the ability to reinvest profits into product development, marketing, and customer retention.

- Success depends on validating demand early, staying close to users, prioritizing retention, and focusing only on features that directly improve recurring revenue and product-market fit.

- The main risks include slower growth, founder burnout, limited hiring capacity, and cash flow pressure during the early months before stable MRR is established.

- For most Canadian founders, bootstrapping works best when the product solves a clear niche problem, customer acquisition costs remain lean, and profits are consistently reinvested into growth.

Bottom Line: Bootstrapping SaaS in Canada is high risk but potentially high reward. Founders who prioritize product-market fit, retention, and disciplined reinvestment often build stronger long-term businesses while keeping full ownership.

Bootstrapping SaaS in Canada is one of the most consequential decisions a Canadian founder can make, and the answer is rarely black and white. This guide breaks down the real risks, real rewards, and the specific financial advantages Canada offers, so you can decide with clarity rather than optimism.

What Bootstrapping SaaS Actually Means

The Core Definition

Bootstrapping means building a company using your own resources: personal savings, revenue from early customers, and reinvested profits rather than outside investment. There are no investors to answer to, no board seats to negotiate, and no equity to give away on day one.

Bootstrapping does not mean staying small forever. It means maintaining control while you build. Some of the most successful software companies in history, including Mailchimp, Basecamp, and Zoho, bootstrapped for years before becoming category leaders. Zoho, as one example, is now fully bootstrapped with over $1.4 billion in annual revenue.

In Canada specifically, several now-iconic SaaS companies, including FEEDOUGH, Clio, and Hootsuite, all validated revenue first and scaled strategically before large investment rounds entered the picture. Overfunding was never a prerequisite for their success.

Why SaaS Is Built for Bootstrapping

SaaS has four structural properties that make it more bootstrap-friendly than almost any other business model.

- Predictable recurring revenue. Monthly and annual subscriptions create a plannable cash flow. Once you have a baseline of paying customers, you know what next month looks like.

- High gross margins. SaaS companies typically operate at 70-85% gross margins. More of every dollar stays in the business compared to physical products or services.

- Low marginal cost. Serving your 500th customer costs almost nothing more than serving your 50th. This is the compounding engine bootstrapped founders can lean on.

- AI-driven efficiency. In 2025, AI tools will allow bootstrapped SaaS founders to build, support, and market products with teams a fraction of the size that was required five years ago.

Bootstrapping vs. VC: A Practical Comparison

The most common early question Canadian founders wrestle with is not how to build a SaaS. It is whether to bootstrap or raise. Here is an honest side-by-side view, drawn from current benchmarks comparing bootstrapped and VC-backed SaaS companies.

| Factor | Bootstrapped | VC-Backed |

| Equity retained | ~80% or more | Founders often diluted to 40-60% by Series A |

| Growth speed | Steady, often 20-25% annually at scale | Faster initially; median 25-30% at scale |

| Marketing spend | Lean, revenue-funded | 90-100% more than bootstrapped peers |

| Profitability | Often profitable or near break-even early | Usually operating at a loss to fuel growth |

| Control | Full founder control | Board and investor input on key decisions |

| Fundraising time | None | Median 142 days to close a seed round in 2025 |

| Failure risk style | Cash flow gaps; slow death | Runway pressure; hard cutoffs |

| Best for | Niche, recurring revenue, patient founders | Winner-take-all markets, rapid scaling needs |

One figure worth internalising: only about 0.05% of startups ever raise venture capital. The other 99.95% bootstrap, borrow, or shut down. Bootstrapping is not plan B. For most founders, it is the only realistic plan on the table.

Bootstrapped SaaS in Canada: The Real Numbers

Growth Rates, Margins and Real Benchmarks

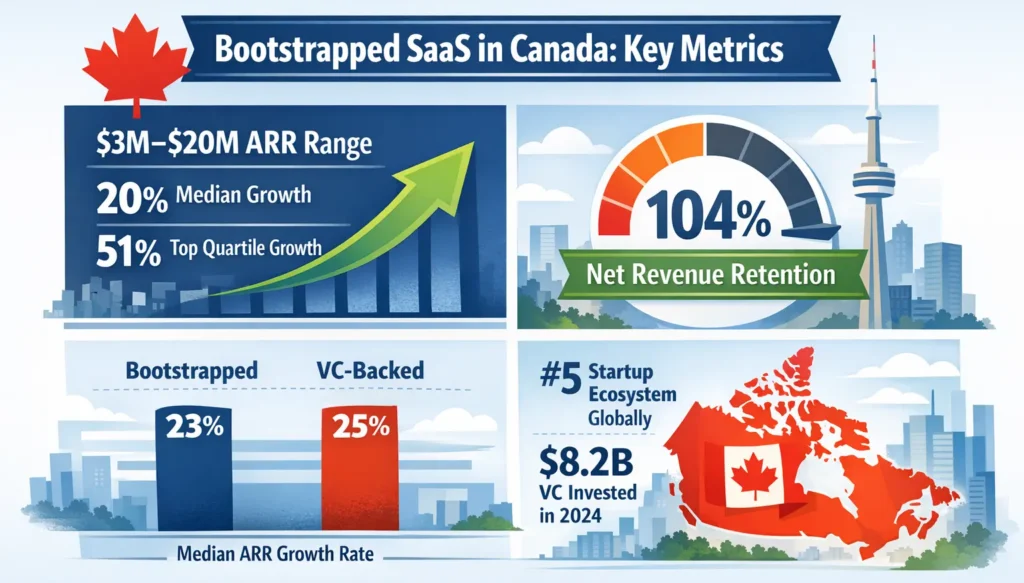

According to SaaS Capital’s 2025 benchmarking survey of over 1,000 private SaaS companies, bootstrapped SaaS companies in the $3M to $20M ARR range carry a median annual growth rate of 20%, with top-quartile performers reaching 51%. Getting to $3M ARR without outside capital is genuinely rare. It means a founder has found product-market fit, built an efficient go-to-market motion, and maintained cost discipline that many VC-backed peers never develop.

Median net revenue retention for bootstrapped SaaS at this scale is 104%, meaning on average these companies are growing their existing customer base slightly year over year. That is a healthy sign for long-term stability.

For early-stage bootstrappers, the growth gap between funded and self-funded shrinks more than most founders expect. Bootstrapped companies report a median ARR growth rate of 23%, compared to 25% for VC-backed peers. The difference is real but not the canyon most people assume.

Canada’s Ecosystem Context

Canada now ranks fifth globally in startup ecosystem strength according to StartupBlink’s 2025 index, with over $8.2 billion in venture capital deployed in 2024. The country has produced 30+ unicorns, with enterprise SaaS companies like Clio, FreshBooks, and PointClickCare among them.

More relevant to bootstrappers: the Canadian SaaS ecosystem strongly favours a revenue-first approach. As Inovia Capital’s Chris Arsenault put it at SaaS North 2024, the companies that survive are not just the best-funded. They are the best prepared. Treat capital as a strategy, not a lifeline, and you have a durable foundation regardless of market conditions.

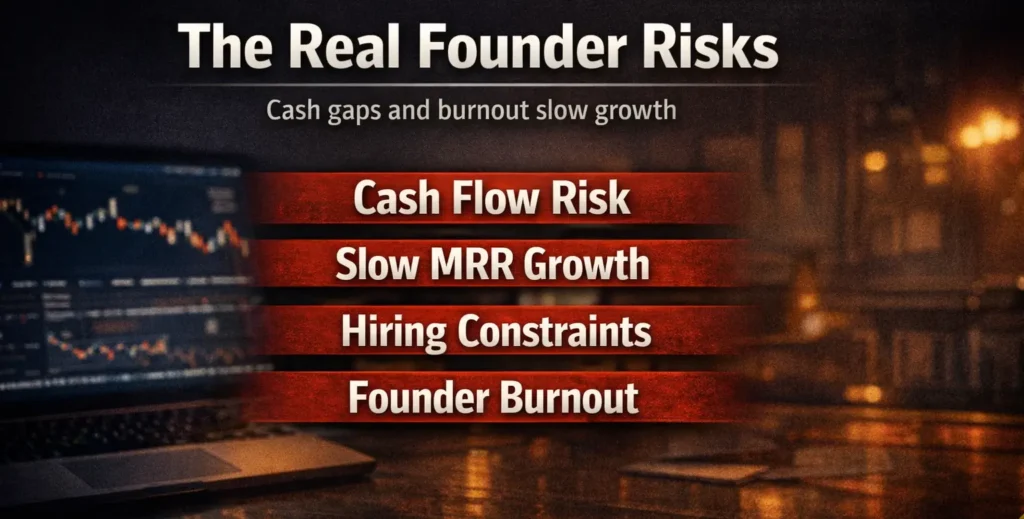

The Hard Truth Most SaaS Founders Ignore

Most bootstrapping content online reads like a success montage. What you see less often are the honest mechanics that separate founders who make it from those who do not.

- Product-market fit is not a phase. It is an ongoing negotiation. Without investor capital to force growth, you will face long stretches of uncertainty where you genuinely do not know if the product is working or if you just have not marketed it properly yet.

- Early MRR growth is painfully slow. Most bootstrapped SaaS companies take three or more years to reach $1M ARR. The median is not two years. The top quartile is. Most founders are not in the top quartile.

- Churn pressure is unforgiving. Every churned customer is your money leaving. Without a runway cushion, customer retention is not a metric. It is a survival mechanism.

- Founder burnout is underreported. You are the product manager, the sales team, the support rep, and the CFO. That identity pressure is real and sustained.

- Long sales cycles hurt more without capital. B2B SaaS deals can take 60-180 days to close. When you are funding the business from your own revenue, those gaps cost you growth and sometimes cost you sleep.

None of this means bootstrapping is the wrong choice. It means you need to go in clear-eyed, not optimistic.

The Real Risks Before You Start

Cash Flow as Your Single Point of Failure

The most underestimated risk in bootstrapped SaaS is not competition or market size. It is cash timing. You might have a product people want, a growing list, and a clear path to revenue, but if three enterprise deals are delayed and two subscribers churn in the same month, you have a problem that no pivot can solve quickly.

The solution is not to avoid risk. It is to understand your burn rate and build your financial model conservatively. Know your personal runway. Know your business runway. Keep those two numbers visible at all times.

Growth Ceiling and Talent Constraints

VC-backed SaaS companies spend roughly 90% more on sales and 89% more on marketing than their bootstrapped counterparts, according to SaaS Capital’s spending analysis. That gap compounds. If you are in a market where speed of distribution determines winners, bootstrapping may be structurally disadvantaged.

Every hire is also funded by revenue, not a fundraiser. You cannot offer equity-heavy packages without diluting yourself. That limits the calibre of talent you can attract in competitive markets like Toronto or Vancouver, where VC-backed startups are paying aggressively.

The US Salary Gap and Retention Risk

This is a 2026-specific risk that deserves its own honest conversation. Canadian bootstrapped SaaS founders are increasingly competing with US-funded remote startups that can offer materially higher salaries, often in USD, to the same pool of Canadian developers and marketers.

A mid-level engineer in Toronto or Waterloo is fielding offers from well-funded US remote teams with compensation packages that a bootstrapped Canadian founder, paying from MRR, simply cannot match in early stages. This is not a reason to avoid bootstrapping. It is a reason to think carefully about your hiring sequence and whether you can serve early customers with a smaller, focused team for longer than originally planned.

The founders who navigate this well tend to compete on culture, ownership, and mission rather than base salary. Offering meaningful early equity to key hires is one lever. Targeting talent who genuinely want to build something, not just earn more, is another.

The Psychological Weight

The internal pressure of bootstrapping is rarely discussed honestly. When you remove the external accountability of investors and board meetings, you lose structure. Many founders discover that the limiting beliefs and identity blocks that slowed them down in a corporate career follow them into their startup. Self-doubt does not disappear when you become your own boss. Often it gets louder.

This is exactly the gap that gets ignored in the ‘just build something’ conversation. The founder’s psychology is the highest-leverage variable in any bootstrapped business.

How Canada Reduces Your Bootstrapping Risk

One of the most overlooked advantages of bootstrapping a SaaS in Canada is the non-dilutive funding ecosystem available to Canadian Controlled Private Corporations (CCPCs). This is not theoretical money. It is real cash that reduces your burn rate without costing you equity.

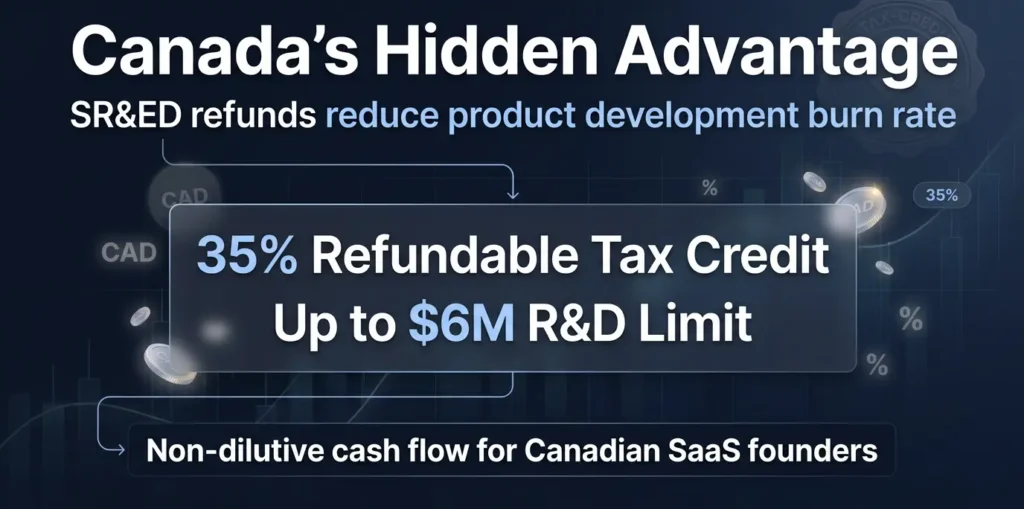

SR&ED: Canada’s Most Valuable Non-Dilutive Tool

The Scientific Research and Experimental Development program is Canada’s largest innovation tax incentive, distributing over $4 billion annually to more than 18,000 claimants. For a bootstrapped SaaS founder, it changes the economics materially.

After the 2025 federal budget, the expenditure limit for the enhanced 35% refundable SR&ED credit doubled from $3M to $6M. That means qualifying corporations can now earn up to $2.1 million in refundable credits annually, a significant increase in available cash flow for R&D-intensive Canadian startups.

Most SaaS companies qualify, including pre-revenue ones. Eligible activities include software development, algorithm experimentation, failed or unfinished R&D projects, and novel technical problem-solving. Track your developer hours and technical documentation from day one, even before you have a single customer.

IRAP and Provincial Stacking

The Industrial Research Assistance Program (IRAP) offers non-repayable contributions up to $1 million for businesses developing innovative products and services. Unlike SR&ED, IRAP should generally not be combined with SR&ED claims on the same work due to overlap risk, but the two programs can complement each other across different project scopes.

Provincial programs add another layer. Ontario’s OIDMTC offers up to 40% refundable credits on qualifying labour and production costs for interactive digital media. BC and Quebec have parallel programs. These credits are stackable with federal SR&ED, and together they can meaningfully reduce the effective cost of building your product in Canada versus bootstrapping from scratch in most other markets.

The Founder Mindset That Makes or Breaks You

Why Constraints Build Better Products

Bootstrapping forces a clarity that outside funding often delays. When every dollar is your dollar, you build features customers will actually pay for, not features that impress investors in a pitch deck. One founder described it directly: every feature has to justify itself in customer value because there is simply no budget for nice-to-have vanity projects.

This constraint-driven discipline is one reason that bootstrapped companies tend to recover faster from market downturns than VC-backed peers. Without a cash cushion to soften decisions, bootstrappers adapt faster. They have to.

The Identity Shift Required

Building a bootstrapped SaaS is as much an identity challenge as a technical or commercial one. One of the most common patterns in entrepreneurship coaching for Canadian founders is the gap between wanting to build a business and being mentally ready to sustain one without external validation or structure.

Darren came to James struggling with a specific version of this gap. He had the ambition and the skill, but goal blocks around income and abundance were keeping him stuck. He could not move toward starting his own business even though the desire was there. After working through those internal barriers with NLP techniques, the shifts were radical. His thinking changed, his actions changed, and critically, his relationship with risk changed. That is the inner work bootstrapping demands.

Developing the right entrepreneurial mindset is not a soft add-on. It is the foundation that the entire business rests on.

Who Should Bootstrap a SaaS in Canada?

Bootstrapping is a genuine fit when most of these are true for you:

- Niche market fit. You have identified a specific, paying niche. The tighter the problem, the faster you reach revenue without a large acquisition budget.

- Equity-first mindset. You value ownership and long-term control over speed-to-scale. You are building a business, not positioning for a fast exit.

- Personal runway. You have 12-18 months of personal financial runway and a household situation that can absorb sustained uncertainty.

- Viable price point. Your SaaS targets a B2B problem where buyers pay $29-$299 per month. That range creates sustainable unit economics without enterprise sales cycles.

- Deep domain knowledge. You are already operating in your target market as a practitioner, operator, or consultant. Founder-led sales convert faster when you speak the customer’s language.

- Revenue discipline. You are committed to learning how to reinvest revenue strategically rather than spending reactively as MRR grows.

Who Should Avoid Bootstrapping

Bootstrapping is likely the wrong move if:

- Winner-take-all market: Your market rewards speed over margins. In those dynamics, VC capital buys distribution that self-funded growth simply cannot match fast enough.

- High pre-revenue capital: Your product needs significant infrastructure, regulatory compliance, or hardware before it can generate a dollar. Bootstrapping and high upfront costs are a poor structural fit.

- Thin personal runway: You have less than six months of personal financial runway with dependents relying on your income. Financial pressure compounds the natural stress of building a product and degrades decision quality.

- Team-heavy delivery: Your core product requires a large team to build or support. Services-heavy SaaS and bootstrapping fight each other at the unit economics level from day one.

- Zero validation: You have not yet confirmed that real customers will pay for the solution. Bootstrapping without willingness-to-pay evidence is expensive hope, not a strategy.

Data and Findings

According to Unleash Your Power’s review of 2025 benchmarking data from SaaS Capital, ChartMogul, and the Canadian startup ecosystem:

| Metric | Bootstrapped | VC-Backed |

| Median ARR growth ($3-20M range) | 20% annually (2025 benchmark) | 25-30% annually |

| Marketing spend vs. bootstrapped | Baseline | 90-100% more |

| Sales spend vs. bootstrapped | Baseline | ~89% more |

| Equity retained at scale | ~80%+ | 40-60% after seed + Series A |

| Gross margins (SaaS average) | 70-85% | 70-85% (structural advantage shared) |

| Avg. time to $1M ARR (median) | 3+ years | Faster with capital deployed |

| Top-quartile time to $1M ARR | ~2 years | Faster |

VC funding declined 30% in Q1 2024, marking one of the weakest quarters since 2018. In that climate, bootstrapped businesses proved they were growing as fast as venture-backed startups while spending roughly one quarter as much on customer acquisition. The structural argument for bootstrapping in Canada has strengthened considerably in the post-2021 funding environment.

The R.O.O.T. Framework for Canadian SaaS Founders

Before you write a single line of code or commit to bootstrapping, run your idea through the R.O.O.T. Framework. Each gate is a checkpoint. If you cannot pass one, it does not mean bootstrapping is off the table. It means you need to solve that problem first.

| Gate | Key Question | Pass Criteria |

| Revenue-first validation | Will people pay before you build fully? | 3-5 paying customers or pre-orders before scaling the build |

| Own your equity deliberately | What am I willing to give up, and when? | Clear personal threshold for dilution vs. control |

| Optimize lean before hiring | Can I reach $10K MRR with the team I have? | Proven unit economics before each significant hire |

| Time your growth triggers | What milestone justifies the next major spend? | Each growth phase funded by the revenue of the previous one |

Step 1: Revenue-first validation.

Do not build a full product before you have paying customers. Build a landing page, a Notion doc, or a consulting offer that solves the same problem manually. Three to five paying customers before you scale development is the baseline proof you need to bootstrap confidently.

Step 2: Own your equity deliberately.

Know your dilution threshold before you are emotionally invested in a term sheet. Many founders accept bad deals because they never decided what they were willing to give up. Clarity on this question before the pressure hits is a decision quality issue, not just a financial one.

Step 3: Optimise lean before hiring.

Your first hires should be funded by proven revenue, not projections. Many bootstrapped founders hire too early based on growth optimism rather than unit economics discipline. The question is not ‘can we afford this person?’ It is ‘have we proven we need this person to deliver existing demand?’

Step 4: Time your growth triggers.

Each meaningful spend increase should be funded by the revenue plateau you have already hit. If you are at $5K MRR and want to invest in paid acquisition, the question is not whether it will work. It is whether your current retention, conversion, and support infrastructure can absorb the growth before it breaks something.

So, Is Bootstrapping Right for You?

Bootstrapping a SaaS in Canada is not a compromise. It is a deliberate strategy with a clear upside: equity, control, profitability, and the kind of discipline that makes companies last.

The risk is real, too. Cash flow gaps, slow growth ceilings, and the sustained psychological pressure of building without a safety net are not small challenges. They are the work.

Before you commit time, capital, or code, score your idea against the R.O.O.T. Framework. If you pass all four gates, you have a viable bootstrapping path. If you stall on one, that is not a signal to quit. It is the exact problem to solve first.

And if what is really slowing you down is not the business model but the founder behind it, that is a different conversation entirely. The self-doubt, the risk aversion, the identity shift from employee to owner: those are the barriers we work on inside Unleash Your Power’s business coaching programs. If you are serious about building, book a call and let’s find out exactly what is standing between you and the version of this that actually works.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.

Frequently Asked Questions

Is bootstrapping SaaS in Canada realistic without a technical co-founder?

Yes, but your path looks different. Non-technical founders bootstrapping a SaaS in Canada typically take one of three routes: no-code platforms like Bubble or Webflow to build a functional MVP, a revenue-share arrangement with a contract developer funded by early customer deposits, or a productized service model where you sell the outcome manually before automating it into software. The critical point is that you do not need to write code to validate willingness to pay. Proof of demand comes before the technical build, not after.

How much money do I need to bootstrap a SaaS startup in Canada?

The honest range is $10,000 to $50,000 for a lean first version, depending on whether you are building it yourself or contracting development. That covers incorporation, basic tooling, early marketing, and three to six months of runway for part-time execution. If you plan to work on it full-time from day one, factor in 12 to 18 months of personal living expenses on top. Canada’s SR&ED program can recover a meaningful portion of your eligible R&D spend as a refundable credit, which effectively reduces your true cost of building once you are incorporated as a CCPC.

What is the biggest mistake Canadian SaaS founders make when bootstrapping?

Building before validating. The most common failure pattern is a founder spending six to twelve months and significant personal capital building a product that real customers never asked for and will not pay for at a price that works. The R.O.O.T. Framework addresses this directly: three to five paying customers before you scale the build is the minimum bar. Willingness to pay is not the same as willingness to use a free tool. Validate the former before committing to either.

Can a bootstrapped SaaS in Canada compete with US-funded competitors?

In niche, well-defined markets, yes. The founders who compete effectively against funded US competitors do so by being more specialised, more responsive, and more deeply embedded in a specific industry or geography. Competing directly on feature breadth or marketing reach against a well-funded US SaaS is a losing game for a bootstrapper. Competing on depth of understanding of a niche problem, faster iteration, and direct founder-to-customer relationships is where bootstrapped Canadian SaaS companies consistently outperform.

Does SR&ED apply to SaaS companies that are not yet profitable?

Yes. The SR&ED program is specifically designed to support early-stage companies, including pre-revenue ones. Canadian Controlled Private Corporations qualify for a 35% refundable credit on eligible expenditures, which means you receive the credit as a cash refund even if your company has no taxable income. Eligible SaaS activities include software architecture development, algorithm design, novel technical problem-solving, and even failed experiments that advanced your technical understanding. The key requirement is documentation: track developer hours, technical decisions, and project progress from day one.

How long does it realistically take to reach $10K MRR bootstrapping a SaaS in Canada?

For most founders, twelve to thirty-six months, depending on niche, price point, and how much time you can commit. Top-quartile bootstrapped SaaS companies reach $1M ARR in roughly two years, which works out to approximately $83K MRR. Reaching $10K MRR first is a meaningful milestone that most serious bootstrappers hit within the first year if they are founder-led, selling into a validated niche. If you are not doing direct outreach and relying solely on inbound or organic traffic from day one, that timeline extends significantly. Understanding how to reinvest revenue strategically at each MRR milestone is what separates founders who stall at $5K MRR from those who compound through it.