Canada’s Big 5 banks (Royal Bank of Canada, Toronto-Dominion Bank, Bank of Montreal, Scotiabank, and Canadian Imperial Bank of Commerce) treat sole proprietors differently from corporations in three concrete ways: they limit credit access, apply activity-based fee structures that grow expensive as your business grows, and charge foreign exchange markups of 2.5 to 3 percent on international transactions.

Because sole proprietors are legally the same entity as their business, banks assess lending risk through personal credit history rather than business credentials. This restricts access to the financial tools that actually help businesses scale.

Understanding how these structural differences work in practice gives you what you need to reduce costs, negotiate smarter, and choose banking infrastructure that fits how your business actually operates.

Key Takeaway:

- For Canadian sole proprietors, the Big 5 banks offer strong credibility, lending access, branch support, and full-service business banking tools but usually come with higher monthly fees and transaction costs. [1]

- Traditional banks like RBC, TD, BMO, CIBC, and Scotiabank are often best suited for businesses needing cash deposits, business credit, merchant terminals, payroll services, or in-person banking support. [2]

- Many early-stage sole proprietors prefer digital or low-fee banking alternatives because they reduce overhead costs, simplify online payments, and often provide unlimited or lower-cost electronic transactions. [3]

- The best banking choice depends on transaction volume, cash handling needs, financing goals, and whether the business values low fees or long-term banking relationships more heavily. [4]

- As a sole proprietor grows, many eventually transition toward larger banks to access business loans, lines of credit, and broader financial services that support scaling operations.

Bottom Line: Big 5 banks provide stability, lending power, and full-service support for Canadian sole proprietors, but lower-cost digital banking solutions may be a better fit during early growth stages when minimizing fees and maximizing flexibility matter most.

- Source: Best Business Bank Accounts for Sole Proprietorships in Canada

- Source: Best Business Bank Accounts in Canada (2026)

- Source: Reddit Discussion – Business Bank Accounts for Sole Proprietors

- Source: Finder Canada – Business Banking Comparison Guide

Sole Proprietor vs Corporation: Banking Differences at a Glance

Not all business owners walk into a bank on equal footing. The moment you disclose your business structure, the bank’s internal systems place you into a risk and product category that shapes everything from your credit options to the fees you will pay.

| Feature | Sole Proprietor | Corporation |

| Legal Status | Same as owner | Separate legal entity |

| Credit Assessment | Personal credit history only | Business and personal history |

| Lending Access | Personal lines, capped limits | Business credit, scalable LOCs |

| FX Rates | Standard retail: 2.5% to 3% | Negotiable at volume |

| Account Features | Basic tiers | Full product suite |

| Fee Waiver Threshold | $65,000 or more | $65,000 or more |

| Deposit Insurance | CDIC up to $100,000 | CDIC up to $100,000 |

The core issue is not that banks dislike sole proprietors. Their pricing and product structures were built around existing clients. You are being assessed like a consumer while paying business account fees.

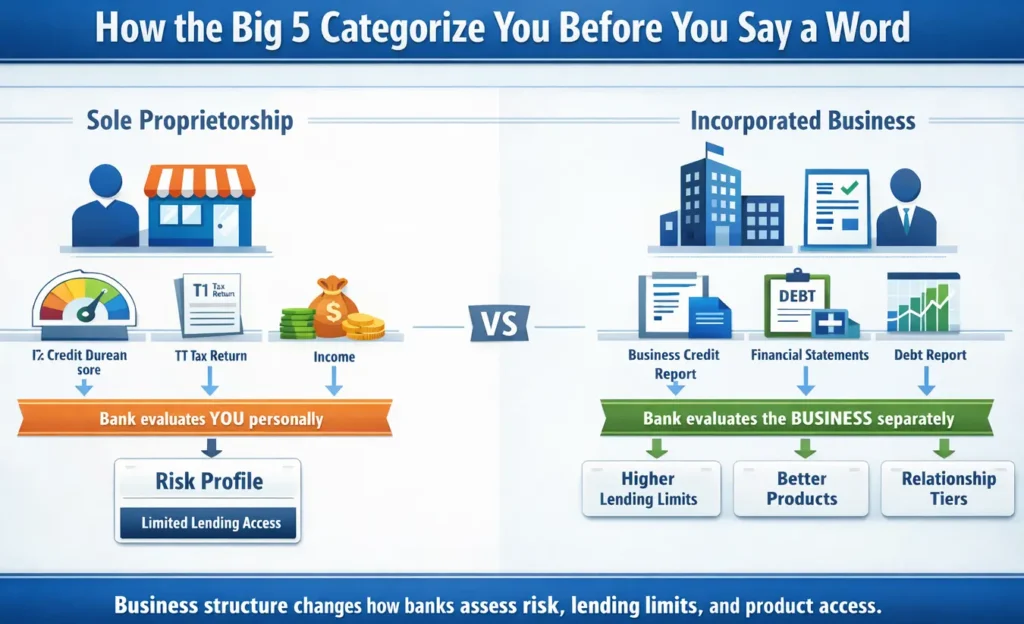

How the Big 5 Categorize You Before You Say a Word

Canadian banks sort every business client into a risk profile before any conversation happens. For sole proprietors, that profile is built entirely on your personal finances, not your business performance.

Since there is no legal separation between you and your business under a sole proprietorship, lenders treat your credit application the same way they would treat a personal loan. Your personal credit score, your personal income on your T1 tax return, and your personal assets form the basis of every decision the bank makes about your business.

For incorporated businesses, the bank assesses the company separately. A corporation can build a distinct credit history, carry its own debt, and present formal financial statements that give lenders a cleaner picture of business performance. That institutional separation unlocks products, lending limits, and relationship tiers that are not available to sole proprietors. Not because you have done anything wrong, but because you do not fit the model the bank was built around.

The Real Reason Banks Prefer Corporations

Most business owners assume banks prefer corporations because corporations are bigger or more established. That is not quite right.

Banks prefer corporations because they are predictable. A corporation files standardized financial statements, carries separate assets, and represents a longer-term lending relationship with predictable fees, interest, and service revenue. From the bank’s perspective, corporations are more profitable clients over time. Their entire product suite is designed to attract and retain them.

The system is not biased against you personally. It is optimized for a different kind of client. Knowing that changes how you navigate it. You are not fighting an unfair institution. You are working around a structure that was never designed with your needs in mind.

As research from the Business Development Bank of Canada consistently shows, the legal form you choose affects everything from your tax treatment to your ability to access capital. The banks understand this clearly. Most sole proprietors find out the hard way.

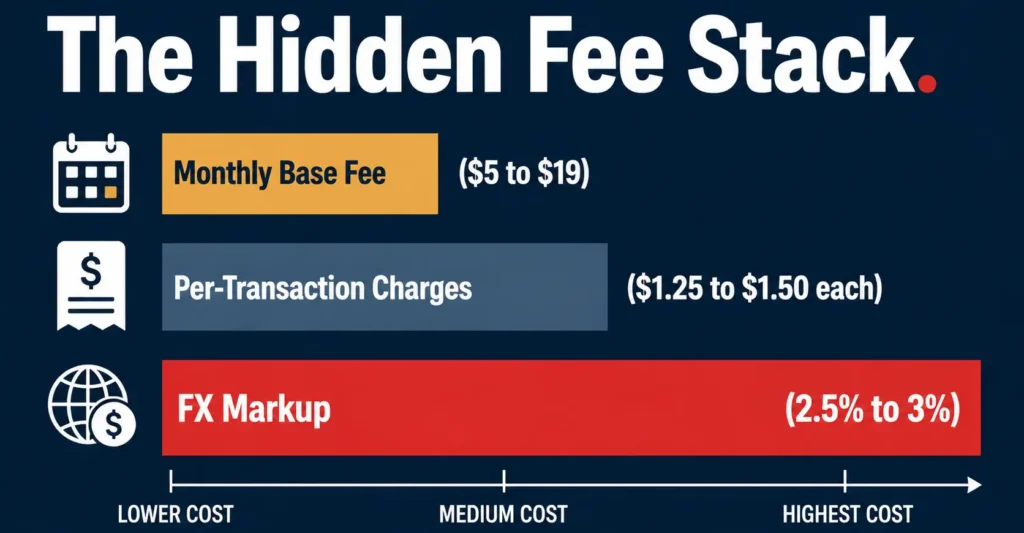

The Hidden Fee Stack Most Sole Proprietors Never See Coming

The monthly fee on a Big 5 business account looks manageable on paper. RBC’s entry-level business account starts around $6 a month. TD’s Basic Business Plan is about $5. That is not where the real cost lives.

The real cost is in activity-based pricing, fees that accumulate every time your business moves money. Per-transaction charges typically run $1.25 to $1.50 for each item beyond your monthly included allocation. Bill payments, e-Transfers, and debit purchases all count toward that cap.

The FX markup is where costs become serious for any business with international exposure. All five major banks apply a foreign exchange markup of approximately 2.5 to 3 percent on top of the mid-market rate. On a $50,000 USD transaction, that is between $1,250 and $1,500 in markup alone. Charged quietly. Disclosed in fine print. Rarely explained at account opening.

Data from banking analysts suggests that Canadian business owners who do not actively monitor their fee structure can pay $200 to $500 annually in charges they never anticipated. For sole proprietors operating with tight margins, that is not a rounding error. It is the real cost of banking with the wrong provider.

To find your actual monthly cost, pull 90 days of statements, identify every charge, and divide by three. Most sole proprietors are genuinely surprised by the number.

The “Free Account” Trap: What BMO’s eBusiness Plan Reveals

BMO’s eBusiness Plan is the only no-monthly-fee business account offered by a major Canadian bank. For sole proprietors watching every dollar, “no monthly fee” sounds like the obvious choice.

Here is what the fine print shows. Every Interac e-Transfer costs $1.50, with no free allocation included. If you send 50 e-Transfers in a month (paying contractors, receiving client payments, covering vendors) that is $75 in transfer fees on an account advertised as free. At 100 transfers a month, you are paying $150. One consultant who made the switch noted she was paying more on her “free” account than she would have paid on a standard business plan elsewhere.

The FX markup on BMO eBusiness sits at approximately 2.9 percent, in line with the rest of the Big 5. And to waive monthly fees on standard Big 5 business accounts, most banks require minimum balances exceeding $65,000. That threshold exists. It is just rarely mentioned upfront.

The lesson is not that BMO eBusiness is a bad product. It works well for digital businesses with low e-Transfer volumes and no FX exposure. The lesson is that “free” in banking is always conditional. The conditions are just not on the front page of the brochure.

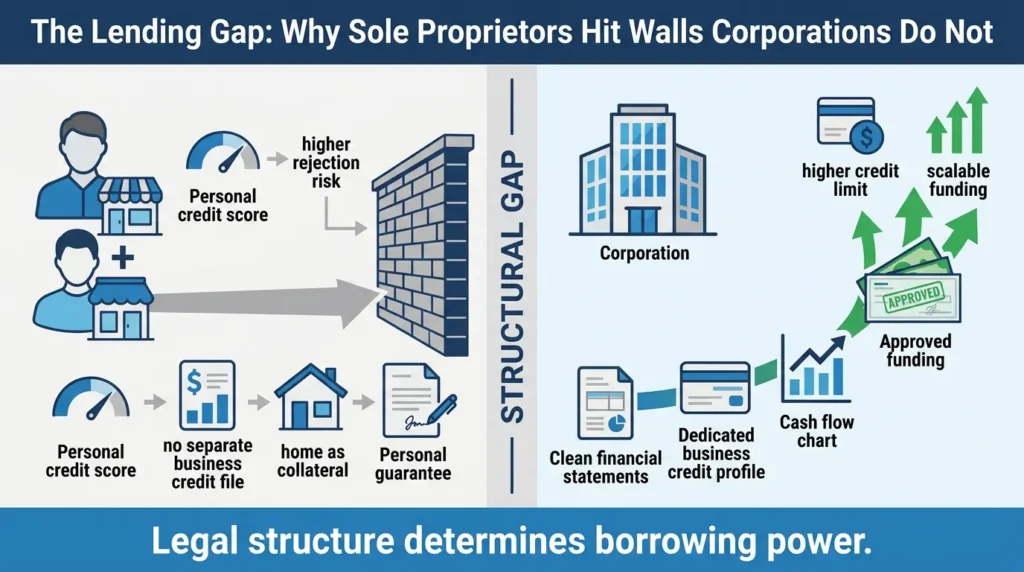

The Lending Gap: Why Sole Proprietors Hit Walls Corporations Do Not

Access to credit is where the structural gap between sole proprietors and corporations becomes most consequential for growth.

For sole proprietors, personal credit is business credit. Lenders look at your personal credit score, your personal income history, and your personal assets when evaluating any business financing request. There is no separate business credit file to build, no corporate balance sheet to present, and no institutional history to leverage.

Research from the Canadian Federation of Independent Business makes the financing picture stark: over half of micro businesses that apply for financing are required to provide a personal guarantee. More than one in four are asked to pledge their primary residence as collateral. The smaller the business, the higher the likelihood of rejection.

Corporations can present formal financial statements, build separate credit profiles, and demonstrate business performance independently of the owner’s personal finances. Even then, Canadian banks often still require personal guarantees for small private corporations. But incorporation improves optionality. It creates the infrastructure for a business to eventually borrow on its own credibility.

Without that legal separation, your business cannot build the independent financial track record that unlocks scalable credit. That ceiling is invisible until you try to push through it. You can also explore the bank accounts for Canadian startups guide for a side-by-side look at how different structures affect account access.

Account Features They Quietly Reserve for Corporations

Certain banking features are technically available to sole proprietors. They are just not proactively offered or prominently advertised unless you fit a certain profile.

Merchant services are a practical example. Providers like Moneris typically require a dedicated business account and often prefer incorporated entities for full service access. Multi-currency accounts and real USD banking infrastructure are another gap. RBC and TD are the strongest among the Big 5 for Canada-US business banking, but navigating that setup as a sole proprietor involves more friction than it does for a corporation.

Accounting integrations vary as well. CIBC has invested in digital infrastructure, including unlimited Interac e-Transfers on certain business account tiers. Most Big 5 accounts offer some level of QuickBooks or Xero connectivity, but the depth of automation scales with account tier. The top tiers are priced for larger corporate clients.

These gaps are not intentional exclusions. They are the result of product design that starts with incorporated businesses and works backward. If you want the full feature set as a sole proprietor, you need to ask specifically and know exactly what to ask for.

Your Real Options: Big 5 Banks, Credit Unions and Fintechs Compared

The right banking choice depends on where your business is now and where it is heading. Here is how the three main paths compare across the criteria that matter most to sole proprietors.

| Criteria | Big 5 Banks | Credit Unions | Fintechs |

| Monthly Base Fee | $5 to $30 or more | $0 to $10 (waived at $3K balance) | $0 |

| e-Transfer Fees | $1.25 to $1.50 each | Limited free allocation | Often unlimited and free |

| FX Markup | 2.5% to 3% | 2% to 2.5% | 0.25% to 0.5% |

| Interest on Balances | Effectively zero | Low but positive | 2.25% to 4% |

| Lending Access | Full (LOCs, term loans) | Strong, especially local | Limited to none |

| Fee Waiver Threshold | $65,000 or more | $3,000 | Not applicable |

| Deposit Insurance | CDIC up to $100,000 | Provincial (often unlimited) | Varies by platform |

| USD or Multi-Currency | Available with friction | Limited | Strong |

| Accounting Integration | QuickBooks, Xero (basic) | Basic | Deep, automated |

| Best For | Businesses scaling toward credit | Cost-conscious sole proprietors | FX-heavy or international businesses |

Big 5 Banks

make the most sense when you anticipate needing a business line of credit, equipment financing, or a commercial lending relationship. Business banking fees at Big 5 banks are often negotiable, particularly for businesses with meaningful deposit volume. Most sole proprietors never ask.

Credit Unions

like Desjardins, Meridian, Alterna, and Coast Capital typically charge lower fees and require far lower minimum balances to waive monthly charges. Many provincial credit unions also offer higher or unlimited deposit insurance through provincial insurers, compared to CDIC’s $100,000 per category limit.

Fintech Platforms

have shifted the calculus in 2026. Some pay 2.25 to 4 percent interest on held business balances. FX rates can run as low as 0.25 percent versus the 2.5 to 3 percent charged by traditional banks. The tradeoff is lending access. Most fintechs still lack the credit infrastructure that banks offer, so businesses that need lines of credit will need to maintain a traditional banking relationship alongside a fintech platform.

Big 5 banks make money on your account balance sitting idle. Fintechs compete by paying you for it. That is a meaningful difference if your business carries working capital reserves.

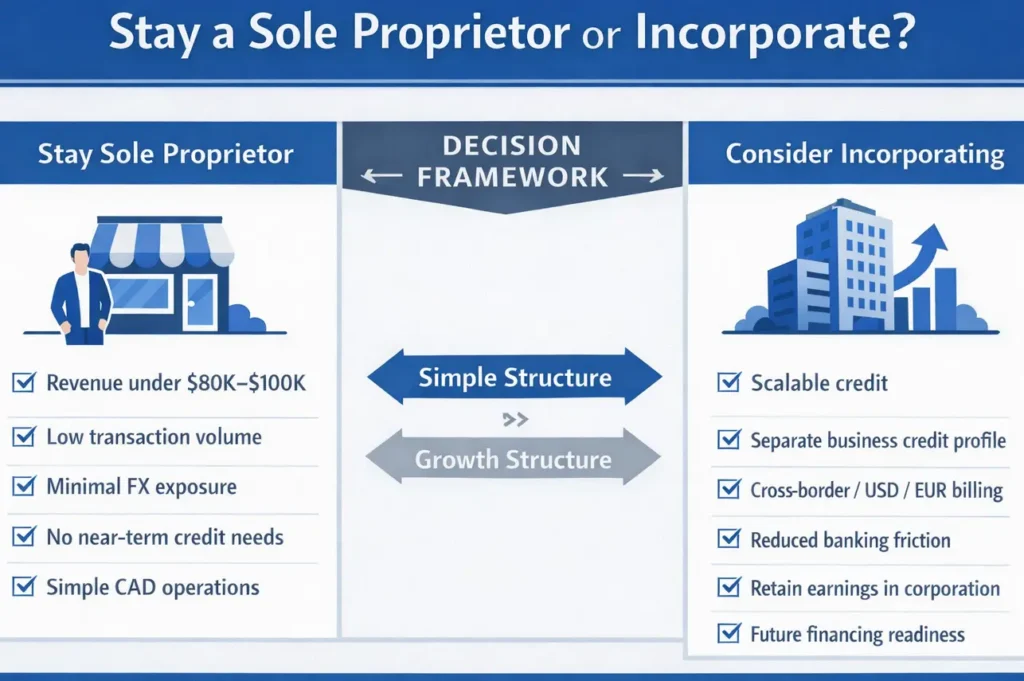

Should You Stay a Sole Proprietor or Incorporate? The Banking Lens

This is one of the most consequential structural decisions you will make as a Canadian entrepreneur, and banking is one of the clearest lenses for evaluating it.

Stay a sole proprietor if:

- Your annual revenue is below $80,000 to $100,000 and the tax savings from incorporation do not yet exceed the administrative costs

- Your FX exposure is minimal and you operate primarily in Canadian dollars

- You do not anticipate needing a business line of credit in the near term

- Your transaction volume is low enough that per-transaction fees are not yet material

Consider incorporating if:

- You need scalable credit and want to build a business credit profile independent of your personal finances

- You are operating cross-border or billing in USD, EUR, or other currencies at a meaningful volume

- Banking friction (fees, transfer limits, FX costs) is starting to constrain how your business operates

- You are generating more income than you personally need and want to retain earnings inside a lower-taxed corporate entity

As RBC’s own business advisors acknowledge, incorporation starts to make strategic sense when your business generates more income than you personally need. Retained earnings inside a corporation can strengthen your balance sheet for future financing. The banking system is designed around that structure. At some point, staying a sole proprietor stops being simple and starts being a structural ceiling.

The Mindset Shift That Changes Everything

In more than 20 years of coaching entrepreneurs through growth decisions, the pattern that shows up most consistently is not a skills gap or a strategy gap. It is the belief that the terms they were given are the terms they have to accept.

Most sole proprietors ask what they qualify for. Smart operators ask what they can negotiate.

Banking fees at the Big 5 are often negotiable, especially for sole proprietors with healthy deposit volumes or consistent transaction history. Banks have discretion in how they price relationships, and few business owners ever sit down with a small business advisor and push for bundled pricing. Those conversations exist. Most people just never have them.

Darren G. came to James feeling blocked in his career and income, unable to access the growth he knew was possible. The breakthrough was not finding better opportunities externally. It was recognizing the assumptions he had never examined. Banking decisions work exactly the same way. The accounts most sole proprietors are in are not the only options available. They are just the ones nobody challenged.

Three questions worth asking before your next banking appointment: What is my true all-in monthly cost, including per-transaction charges? What is the minimum balance required to waive fees on this account? What does my lending eligibility look like if I need a line of credit in the next 12 months?

Those three questions shift you from customer to client. That is a fundamentally different conversation. For more on how smart goal setting drives business growth, that resource goes deeper on the strategic thinking that separates reactive operators from decisive ones.

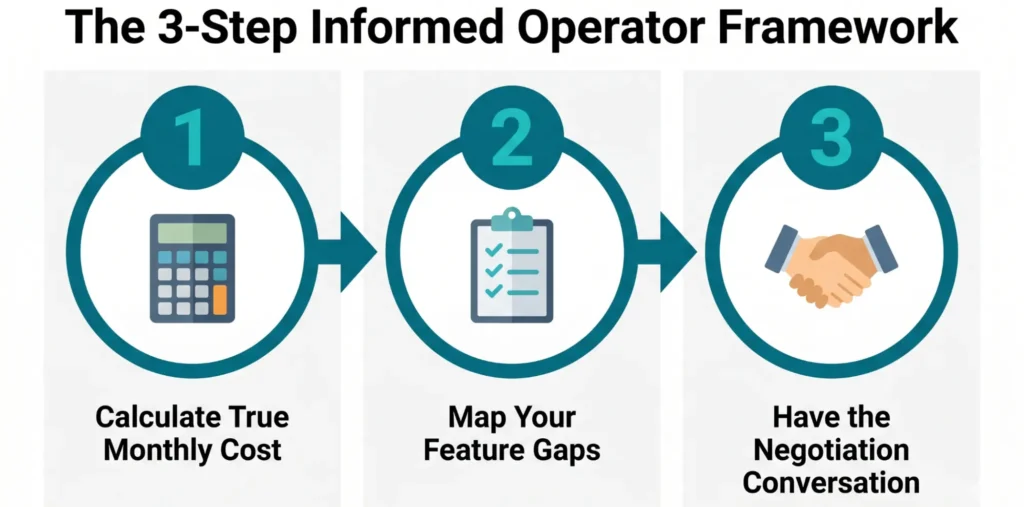

The 3-Step Informed Operator Framework

This framework applies whether you are evaluating your current bank, preparing to switch, or deciding whether incorporating makes sense for your business right now.

Step 1: Calculate Your True Monthly Cost

Do not rely on the advertised monthly fee. Pull 90 days of bank statements, identify every charge category, and divide by three. Include monthly fees, per-transaction charges, e-Transfer fees, wire fees, and FX markup on international activity. Most sole proprietors find that their actual cost is 30 to 70 percent higher than the listed account fee.

Step 2: Map Your Feature Gaps

List the banking features your business actually needs over the next 12 months: USD account access, accounting software integration, merchant services, credit facility access, and unlimited e-Transfers. Then check honestly whether your current account delivers these or whether you are working around limitations every single month.

Step 3: Have the Negotiation Conversation

Before switching banks, request a meeting with a small business advisor, not a general banking rep. Ask specifically about bundled pricing, fee waivers based on deposit volume, and lending eligibility. Many Big 5 banks have discretion on pricing for business clients who ask. That conversation costs you 45 minutes. The savings can be significant.

Data and Findings

Research consistently shows that small businesses in Canada face a compounding disadvantage as they grow within the wrong banking structure.

Data from the Canadian Federation of Independent Business found that over half of micro businesses required to seek financing had to provide a personal guarantee, and more than one in four had to pledge their primary residence. Smaller businesses face higher rejection rates for financing than larger ones, and that gap has widened over the past decade.

A 2023 CFIB report found that 10 percent of Canadian business owners switched banks at least once between 2019 and 2022, with banking fees and customer service as the top two reasons. One in ten small business owners switching banks in a three-year window signals structural dissatisfaction, not marginal frustration.

Per-transaction charges of $1.25 to $1.50 each, combined with a 2.5 to 3 percent FX markup, can push a sole proprietor’s real banking costs to $200 to $500 annually beyond the advertised account fee. For businesses with significant e-Transfer or international transaction volume, that figure climbs substantially higher.

The Canada Small Business Financing Program has disbursed over $11 billion in loans to small businesses over the past decade and is fully available to sole proprietors. Applications go through participating financial institutions, and lenders make independent approval decisions. Knowing this option exists before you need it changes how you approach your entire banking relationship. The best bank accounts for small businesses guide on this site provides additional context on finding the right account fit for your stage.

Frequently Asked Questions

Can a sole proprietor use a Big 5 business account in Canada?

Yes. All five major Canadian banks offer business accounts to sole proprietors. You may need a trade name registration or business licence to open the account, depending on the bank and account type. The products, fees, and features available to sole proprietors differ meaningfully from those offered to incorporated businesses, particularly around credit access and account tiers.

What is the cheapest business bank account in Canada for a sole proprietor?

BMO’s eBusiness Plan is the only no-monthly-fee business account offered by a Big 5 bank, but e-Transfer fees of $1.50 each can make it expensive for active businesses. Among all providers, credit unions like Alterna Bank and online platforms like EQ Bank offer competitive low-fee or no-fee structures with lower balance requirements than the major banks.

Do Canadian banks treat sole proprietors differently from corporations?

Yes. Because sole proprietors and their businesses are the same legal entity, banks assess lending risk through personal credit history rather than business performance. This affects credit access, product eligibility, and relationship tiers. Corporations can build separate credit profiles and access a wider range of business financial products over time.

Why do banks require personal guarantees from sole proprietors?

A personal guarantee makes the business owner personally responsible for repaying business debt if the business defaults. For sole proprietors, this is essentially automatic since there is no legal separation protecting personal assets. For corporations, banks often still require personal guarantees on small business loans, but incorporation creates more flexibility as the business grows and builds its own financial credibility independently.

What happens to my banking when I incorporate my sole proprietorship?

When you incorporate, you create a new legal entity with its own Business Number from the CRA. That entity requires its own business bank account. Corporations cannot legally use the owner’s personal account for business transactions. Your sole proprietor account does not transfer automatically. You will need to open a new corporate account, update all payment arrangements, and register the corporation separately for GST/HST and payroll accounts if applicable.

Conclusion

The Big 5 are not broken. They are just designed for a different client, and most sole proprietors discover that mismatch quietly, one fee at a time.

The information here gives you what banks do not hand you at account opening: a clear picture of how the system categorises you, what it costs you, and what your real options are. From there, the next move is yours. Do the math on your true monthly cost. Ask about fee waivers before accepting the rate card. Explore what a credit union or fintech could offer your specific business model. And if your banking structure is starting to feel like a ceiling on your growth, it is time to evaluate seriously what incorporating could unlock.

This is the kind of strategic reinvestment thinking that confident business operators use to build durable margin. If you want to support building that clarity across every dimension of your business, working with a business coach in Toronto gives you a structured path to make decisions with confidence, not guesswork. NLP training for business takes that further, building the mindset and communication tools that let you advocate for yourself in every room, including the bank.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.