Most Canadian business owners don’t stay with the wrong bank because they love it. They stay because switching feels risky. When it comes time to switch Canadian business banks, that fear makes sense. Payroll has to go out on time. CRA remittances can’t bounce. Vendors need to get paid. The thought of touching any of that sends most business owners right back to their overpriced, under-featured account for another year.

But here’s what I’ve seen after working with entrepreneurs and business leaders for over 20 years: the problem isn’t switching banks. The problem is switching without a plan.

Hidden fees are eating into your margins. Interac e-Transfer limits are slowing your cash flow. Accounting software that refuses to sync cleanly. Poor customer support when you actually need answers. These aren’t minor inconveniences. There are quite a few constraints on your growth, and they compound over time.

Key Takeaway:

- Canadian businesses should consider switching banks when they experience high fees, restrictive transaction limits, poor customer support, outdated digital tools, or limited financing options that no longer match business growth needs. [1]

- Before switching, businesses should compare monthly fees, transaction costs, FX charges, lending support, integrations, and online banking features not just promotional offers or “no-fee” marketing claims. [2]

- The safest transition process includes opening the new account first, updating payroll and recurring payments gradually, monitoring transactions for several weeks, and only then closing the old account. [3]

- Many businesses overlook hidden costs when switching banks, including wire fees, transaction overages, foreign exchange markups, payment processing charges, and fees tied to government remittance services. [4]

- The best banking setup depends on business type: digital-first businesses often benefit from low-fee online banking, while cash-heavy or scaling companies may still benefit from traditional branch-based banking relationships.

Bottom Line: Switching Canadian business banks can improve cash flow, reduce hidden fees, and streamline operations but the best results come from comparing total banking costs carefully and transitioning accounts methodically to avoid disruptions.

- Source: NerdWallet – How and Why to Switch Business Bank Accounts

- Source: No-Fee Business Banking in Canada (2026 Guide)

- Source: Finder Canada – How to Switch Banks

- Source: Common Mistakes When Switching Business Banks

This guide gives you a clear, step-by-step system to switch your Canadian business bank without missing a payment, confusing a vendor, or waking up to a cash flow surprise. Zero downtime isn’t wishful thinking. It’s the result of a structured approach.

How to Know It’s Time to Switch Your Business Bank in Canada

Before we get into the how, it’s worth naming the signs you’ve likely already noticed

Your monthly fees have crept up without a corresponding improvement in service. Your Interac e-Transfer limits are creating friction in transactions that should be instant. Your bank’s platform doesn’t talk to QuickBooks Online or Xero properly, meaning someone on your team is manually reconciling statements every month. When you call for support, you wait.

These are operational drains that show up in your energy and your team’s time before they show up on your income statement. A banking relationship that made sense when you started may be holding you back now that you’re growing. Recognizing that isn’t disloyalty. It’s clarity.

If your current bank is costing you more time than it saves, it’s already costing you money.

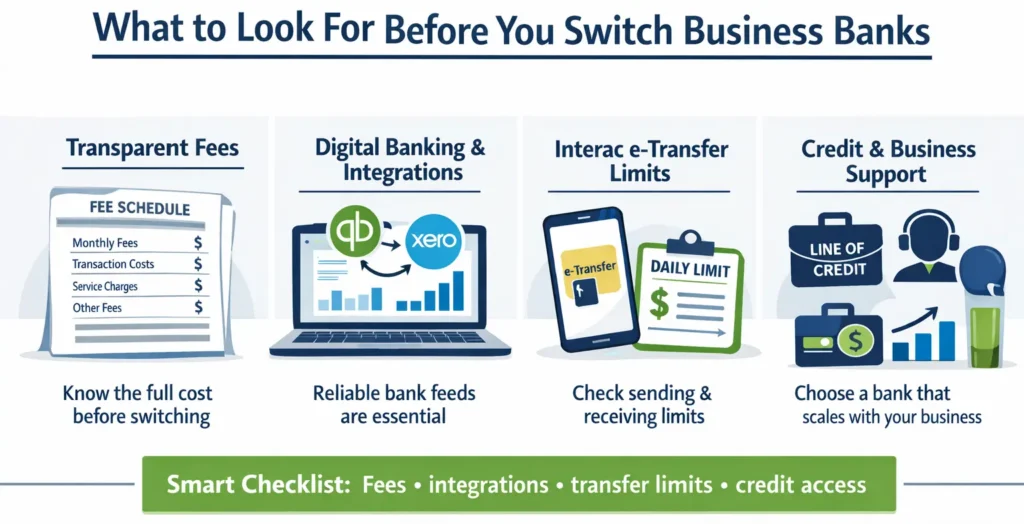

What to Look For Before You Switch Business Banks

Switching to the wrong bank is almost as bad as staying with the one you have. Take time to evaluate the right fit before you move anything.

Transparent Fees and Scalable Pricing

Monthly fees, per-transaction costs, wire transfer charges, and NSF fees should all be clearly listed and easy to understand. Some accounts look affordable on the surface but carry per-transaction fees that stack up fast for active businesses. Know the full cost before you commit, not after.

Strong Digital Banking and Accounting Integrations

This is non-negotiable for most businesses today. Your new bank needs to sync reliably with your accounting software, whether that’s Xero, QuickBooks Online, or another platform. Unreliable bank feeds are one of the most common and most frustrating pain points Canadian business owners face. Confirm the integration before you open the account.

Interac e-Transfer Flexibility

For many Canadian businesses, Interac e-Transfer is a primary payment tool. Check your sending and receiving limits. Some accounts cap daily transfers well below what growing businesses need, which creates bottlenecks at exactly the wrong moments.

Access to Credit and Business Support

Beyond your operating account, think about what you’ll need as you grow. Can this bank provide a business line of credit? Do they have advisors who understand your industry? The right banking partner should be able to grow alongside you, not just hold your deposits.

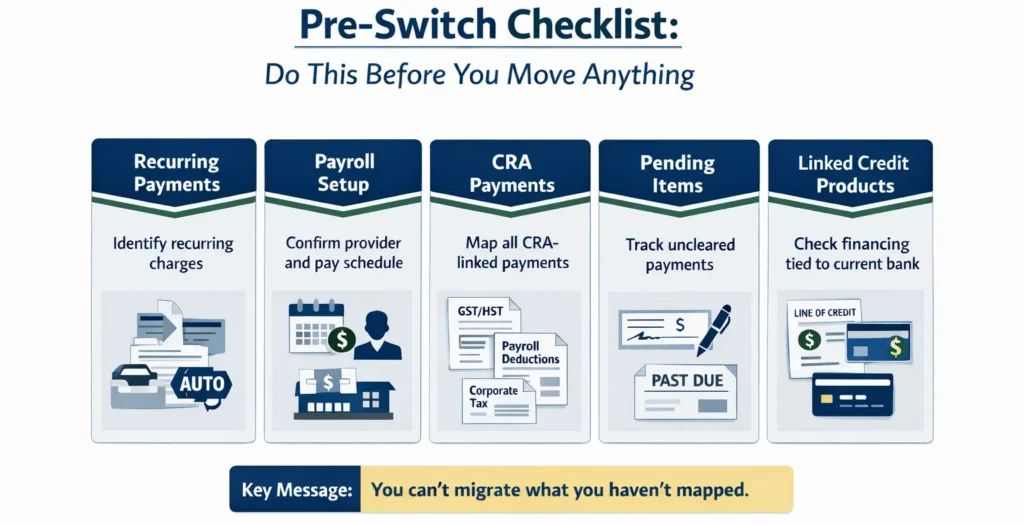

Pre-Switch Checklist: Do This Before You Move Anything

This is where most business owners skip ahead and pay for it later. Spend time here and the rest of the process becomes straightforward.

Before you touch a single payment or transfer, build your complete financial picture. List every recurring payment and subscription tied to your current account. Identify your payroll provider and schedule. Map out your CRA-linked payments, including GST/HST remittances, payroll deductions, and corporate tax installments. Track any outstanding cheques or invoices that haven’t cleared yet. Note whether any financing or credit products are tied to your current account, since those relationships may need to be addressed separately.

This isn’t busywork. This is the foundation that makes zero downtime possible. You can’t migrate what you haven’t mapped.

Data & Findings

Declining Satisfaction Among SMEs

Small business banking satisfaction in Canada continues to decline. According to the Canada Small Business Banking Satisfaction Study 2025 by J.D. Power, overall satisfaction dropped to 652/1000, continuing a downward trend.

Rising inflation, banking fees, and operational pressure are the main contributors, with satisfaction closely tied to cost control and service quality.

Market Dominated by the Big Six Banks

Canada’s banking sector remains highly concentrated. A recent analysis of Canada’s banking competition and structure by Reuters shows that the Big Six banks dominate most SME banking relationships, limiting competition and slowing innovation in pricing and digital services.

This concentration also reduces switching flexibility, prompting regulators to explore reforms to improve competition.

Hidden Fees & Cost Transparency Issues

Unclear and rising banking costs remain a major challenge. Research on SME banking challenges in Canada from Deloitte shows that 32% of small businesses experience financing delays and banking friction.

Many SMEs report unexpected charges and poor fee transparency, which directly impacts cash flow predictability and financial planning.

Digital Banking & Integration Are Now Essential

Digital banking has become a core requirement for SMEs. The Canada Banking Mobile App Satisfaction Study 2024 by J.D. Power highlights that mobile experience, ease of use, and issue resolution are now key satisfaction drivers.

Businesses also struggle with poor integration between banking systems and accounting tools, reinforcing the need for real-time cash flow visibility and automation.

Switching Banks: High Demand, Low Action

Despite dissatisfaction, many SMEs hesitate to switch banks. Insights from SME banking behaviour insights by Deloitte show that businesses fear disruption in payments, payroll, and CRA-related processes.

While better alternatives exist, this hesitation, not lack of options, remains the primary barrier, though improved digital onboarding is gradually reducing friction.

Financial Health Drives Satisfaction

Business performance strongly influences banking satisfaction. According to banking satisfaction and financial health insights from J.D. Power, financially stable businesses report significantly higher satisfaction levels.

In contrast, companies under cash flow pressure experience more issues with fees, credit access, and processing delays, confirming a direct link between financial health and perceived banking quality.

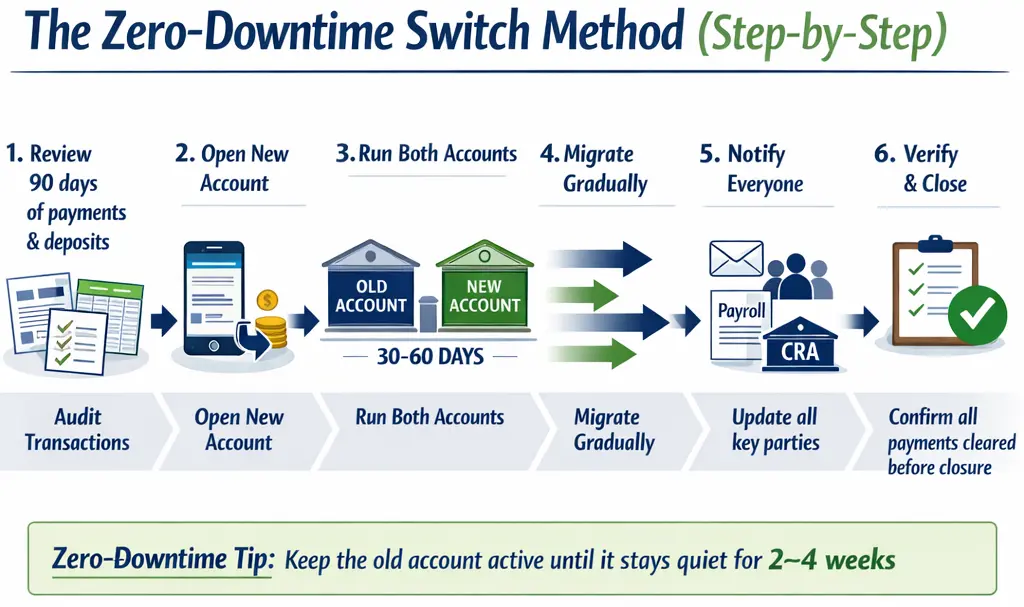

The Zero-Downtime Switch Method (Step-by-Step)

Step 1: Audit Every Payment and Deposit

Export the last 90 days of transactions from your current account and go through them line by line. Categorize everything: vendors, subscriptions, payroll, government remittances, client deposits, and loan payments.

Pay special attention to quarterly and annual payments. Insurance premiums, software licenses, professional dues, and government installments often get missed because they don’t show up in monthly reviews. Finding one of these after you’ve closed your old account is the kind of thing that keeps you up at night.

Try this: Create a simple spreadsheet with three columns: payment name, frequency, and amount. Flag everything that’s automated or pre-authorized. This becomes your migration checklist.

Step 2: Open Your New Account First

Never close your old account before your new one is fully operational. Open your new business account, set up online banking access, test the accounting integration, and make a few small transactions to confirm everything works as expected.

This step often takes longer than people expect, especially if you’re opening at a new institution that requires documentation reviews or in-person verification. Build that time into your plan and don’t rush it.

Step 3: Run Both Accounts in Parallel for 30 to 60 Days

This is the single most important part of the Zero-Downtime Switch Method. Keep both accounts open and active. Maintain enough funds in your old account to cover any payments you haven’t migrated yet.

Running parallel accounts feels redundant. It’s meant to. That redundancy is your safety net. During this window, you’ll catch the quarterly payment you almost forgot, the pre-authorized debit that somehow didn’t make your original list, and any vendor that’s still sending invoices to your old banking details.

Step 4: Migrate Payments Gradually

Don’t flip everything to the new account in one day. Move payments in phases, starting with the lower-stakes ones and working toward payroll and government remittances once you’re confident the new account is functioning exactly as it should.

Moving payroll last is intentional. Your team needs to be paid without delay or confusion. Give yourself time to verify the new payroll setup is working properly before you fully commit.

Step 5: Notify and Update All Key Parties

This is a step people rush and then regret. Be systematic about who needs your new banking information and give them enough lead time to update their systems before you expect a payment.

Contact your vendors and suppliers. Update client invoices and payment instructions. Notify your payroll provider. And critically: update your CRA My Business Account with your new banking details. This includes your GST/HST remittance information, payroll deductions, and any corporate tax payment schedules. Failing to update CRA is one of the most common and most disruptive oversights in this process.

If clients pay you by pre-authorized debit, you’ll need to collect new PAD agreements with your updated banking details. Start that process early.

Step 6: Verify Everything, Then Close Your Old Account

Before you close, run through your migration checklist one final time. Confirm every automated payment has cleared from the new account at least once. Check that your old account has been quiet for at least two to four weeks with no unexpected activity. Leave a small buffer balance in the old account until you’re certain.

When you’re confident, request the account closure in writing and ask for confirmation. Some Canadian banks charge an early closure fee if you close within 90 days of opening, so be aware of that timing. For the Big Five specifically, closure processes vary: TD and CIBC both allow phone closures in some cases, while BMO typically requires a branch visit.

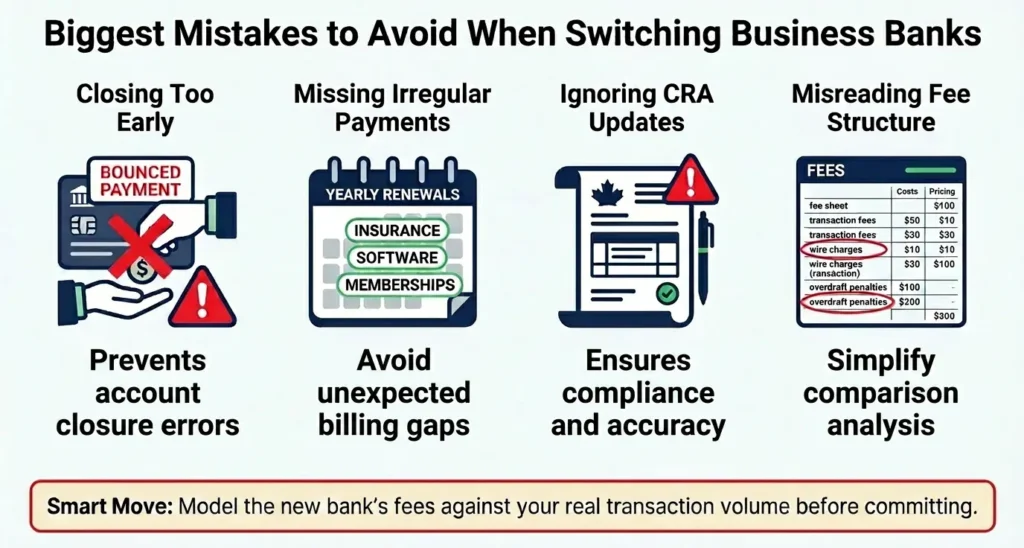

What Are the Biggest Mistakes to Avoid?

Closing your old account too early:

This is the most common and most expensive mistake. A single bounced payment can damage a vendor relationship or trigger NSF fees at exactly the wrong time.

Missing irregular payments:

Annual insurance premiums, software renewals, and professional memberships don’t appear in your monthly transaction history. Export a full year of transactions, not just the past 30 days, to make sure nothing falls through.

Ignoring CRA account updates:

Your Canada Revenue Agency remittances are time-sensitive. A missed or misdirected payment can result in penalties that far exceed any savings from switching banks. Update CRA before you redirect anything else.

Misreading the new bank’s fee structure:

Monthly fees are obvious. Per-transaction fees, wire charges, and overdraft penalties are not always front-of-mind during the sales conversation. Read the full fee schedule and model it against your actual transaction volume before you commit.

A Quick Mindset Check

Here’s something I’ve observed working with business owners across industries: the people who delay this kind of decision don’t lack information. They have plenty of information. What they lack is a clear starting point and permission to take the first step.

Treat this switch like any other business project. Block one to two focused hours to complete Step 1. Once you have your payment audit done, the rest of the process has momentum. Clarity eliminates overwhelm, and action eliminates paralysis.

How Long Does It Take to Switch Business Banks in Canada?

The realistic timeline is 30 to 90 days, depending on how complex your financial setup is. A solo entrepreneur with a simple payment structure can move faster. A business with multiple vendors, payroll integrations, and CRA remittances should plan for the full 90 days

Timing matters too. Avoid starting a bank switch in the weeks leading up to a major tax deadline, during your busiest revenue period, or in the middle of a payroll cycle. The best time to switch is during a slower business period when you have bandwidth to monitor the transition carefully.

Try this: Open a calendar and block out the next 90 days. Mark your payroll dates, tax deadlines, and major payment dates. Then map your migration phases around those anchors. You’ll immediately see the cleanest window for each step.

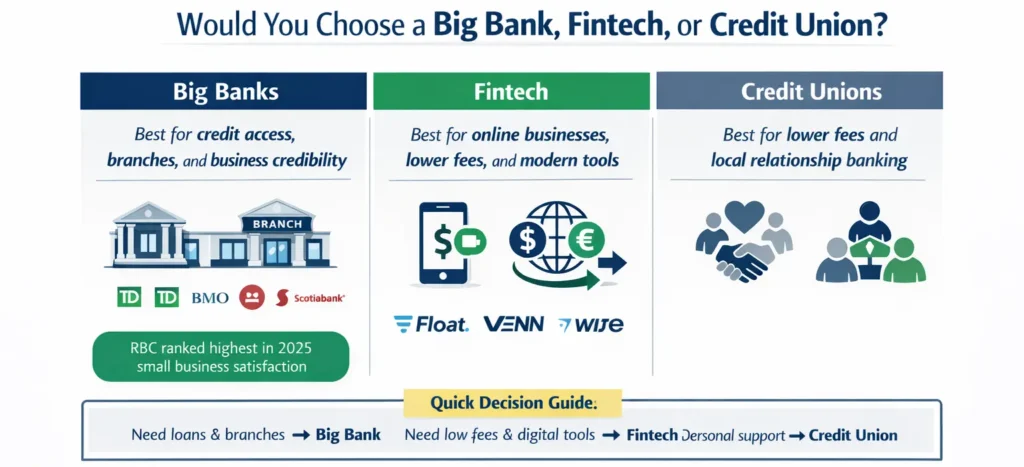

Should You Choose a Big Bank, Fintech or Credit Union?

The right answer depends on what your business actually needs, not on brand familiarity or habit.

Big Five Banks (RBC, TD, BMO, CIBC, Scotiabank)

Best for established businesses that need access to credit, in-person support, and a recognized institution for client-facing credibility. According to the J.D. Power Canada Small Business Banking Satisfaction Study, RBC ranked highest in small business satisfaction in 2025, followed by BMO. If lending relationships and physical branch access matter to you, the Big Five still have real advantages

Fintech Options (Float, Venn, Wise)

Best for businesses that operate primarily online, want lower fees, and need modern integrations. Float, for example, offers up to 4% annualized interest on CAD and USD balances with no monthly fees, which is a meaningful difference for businesses that carry working capital in their operating account. Wise remains the strongest option for businesses with significant international transaction volume. If your business runs lean and digital, these accounts can outperform traditional options significantly.

Credit Unions

Best for businesses that value personalized relationships, regional expertise, and community connection. Credit unions often offer more flexible lending decisions and lower fees than the Big Five, and they’re an underutilized option for many Canadian entrepreneurs. If you’re based outside a major urban centre, a regional credit union can offer meaningful advantages in both service quality and local market knowledge.

For a deeper look at which account structures suit different business stages, the guide on bank accounts for Canadian startups breaks it down by business type and stage.

Frequently Asked Questions

What is the safest way to switch business banks in Canada without downtime?

The safest method is to open a new account first, run both accounts in parallel for 30–60 days, migrate payments gradually, and only close the old account after confirming all transactions are fully switched.

How long does it take to switch business banks in Canada?

Switching typically takes 30 to 90 days, depending on business complexity. Simple businesses may complete it in under a month, while businesses with payroll, CRA payments, and multiple vendors need longer overlap periods.

Will switching business banks interrupt payroll or payments?

No, if done correctly. Interruptions only happen when business owners close the old account too early or fail to migrate automatic payments and payroll systems in advance.

Do I need to update CRA when switching business banks?

Yes. You must update your CRA My Business Account banking details to ensure GST/HST refunds, payroll deductions, and corporate tax payments are deposited correctly into your new account.

What is the biggest mistake when switching business banks?

The biggest mistake is closing the old account before all automatic payments, payroll, and CRA-linked transactions are fully migrated and verified in the new account.

Can I switch business banks without affecting cash flow?

Yes. Cash flow remains uninterrupted if you use a parallel account strategy, keep sufficient funds in both accounts, and migrate transactions in controlled phases rather than all at once.

How to Switch Canadian Business Banks: Final Thoughts

Switching business banks isn’t complicated. It’s a process problem, not a risk problem.

The risk was always in staying put without questioning whether your bank still serves your growth. The business owners who take decisive, planned action on their financial infrastructure consistently put themselves in a stronger position than those who delay out of fear of disruption.

Once your banking is optimized, the next step is making sure the cash flow you’re protecting is working as hard as possible for your business. Explore smart reinvestment strategies that put your capital to work rather than letting it sit.

You’ve built something worth protecting. Your banking should reflect that.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.