With USD cross-border bank accounts, you invoice a US client for $10,000 USD. The payment lands. You feel good. Then you check your actual balance and find $9,600. No one sent you an explanation. No line item called “we took your money.” It just disappeared quietly, automatically, the way bad systems always bleed you dry when you’re not paying attention.

That’s what happens when Canadian startups assume their USD account is doing the job it was built to do. Most of the time, it isn’t. The account exists. The money arrives. But the infrastructure underneath is outdated, expensive, and designed for a world that doesn’t match how modern businesses actually operate.

Key Takeaway:

- USD cross-border bank accounts help Canadians manage U.S. payments, hold American dollars, reduce currency conversion costs, and simplify business or personal transactions between Canada and the United States. [1]

- The best cross-border accounts typically offer low FX fees, seamless CAD/USD transfers, U.S.-based banking access, online integrations, and the ability to receive or send U.S. payments efficiently. [2]

- Traditional Canadian banks like RBC, TD, and BMO provide integrated Canada–U.S. banking solutions, while fintech platforms often compete by offering lower fees, faster transfers, and better exchange rates. [3]

- Cross-border banking is especially valuable for freelancers, ecommerce sellers, remote workers, investors, and businesses that earn, spend, or invoice regularly in U.S. dollars. [4]

- The right account depends on transaction volume, FX sensitivity, cash access needs, and whether the user prioritizes branch support, low fees, or digital-first banking convenience.

Bottom Line: The best USD cross-border bank accounts help Canadians minimize currency conversion costs, streamline U.S. transactions, and manage American dollar cash flow efficiently. Choosing the right provider depends on balancing fees, FX rates, digital tools, and cross-border banking convenience.

- Source: Wise – Canada U.S. Cross-Border Banking Guide

- Source: Finder Canada – Best Cross-Border Bank Accounts

- Source: TD Canada Trust – Cross-Border Banking Solutions

- Source: Forbes Advisor Canada – Best U.S. Bank Accounts for Canadians

In 20+ years of coaching Canadian entrepreneurs, I’ve seen brilliant founders make every smart decision imaginable, and then leave thousands of dollars a year on the table because nobody told them their banking setup was a leaky pipe. This article gives you the framework to fix that. By the end, you’ll know exactly which USD cross-border bank account fits your business, what it should cost, and how to stop the silent losses for good.

Why Most Canadian Startup USD Accounts Are Costing You Money

The Bucket vs. Tool Problem

There’s a critical difference between a USD account at a Canadian bank and a true USD cross-border account. One is a bucket that holds US dollars, but it’s not actually connected to the US payment infrastructure. The other is an operational tool, built on ACH rails, that lets your business send and receive payments like a local US company.

Most founders don’t realize they have a bucket until the fees start showing up. And by that point, they’ve already lost months of unnecessary costs they can’t get back.

SWIFT vs. ACH: The Difference That Costs You Thousands

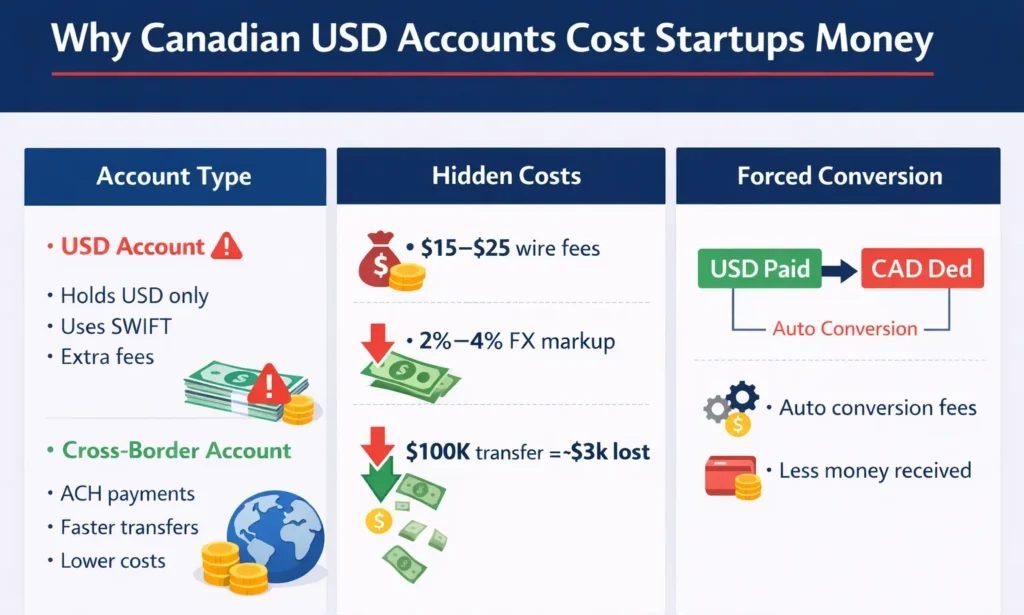

When your USD account sits on Canadian banking infrastructure, every incoming payment from a US client travels through the SWIFT network. SWIFT-only accounts treat every incoming “USD” payment as an international wire, triggering inbound wire fees of $15 to $25 even when both accounts hold US dollars.

ACH is the domestic US payment rail. It’s fast, it’s free, and it works the way your US clients expect. True local US accounts connect directly to the US payment infrastructure, enabling ACH payments, faster processing, and eliminating cross-border wire fees. For a business making 10 US vendor payments monthly, the difference amounts to $300 to $500 in savings. That’s not a rounding error. That’s a real runway.

Hidden FX Markups You’re Probably Not Tracking

This is where most Canadian founders get hit hardest, and it’s the one cost that almost no one audits. In Canada, traditional FX markups can range from 2% to over 4%, depending on the currency pair, your transaction volume, and whether you’re using wire or SWIFT. These fees don’t show up as a line item. They’re baked into the exchange rate your bank quietly offers you instead of the real mid-market rate.

For a $100,000 USD transfer, a 3% markup translates to roughly $3,000 in lost value and these markups are rarely disclosed transparently, making cost forecasting difficult for finance teams managing regular cross-border payments.

Try this: Go to XE.com right now and note the mid-market CAD/USD rate. Then compare it to the rate your bank quoted on your last conversion. Subtract the difference and multiply by your annual USD revenue. That number is what your current banking setup is costing you every year.

The Forced Conversion Trap

If you’re using Stripe, Shopify, or PayPal to collect USD revenue, you’re likely caught in a forced conversion loop. Even if your customers pay in USD, if your connected account is CAD-based, Stripe and Shopify will automatically convert funds before deposit, triggering both FX markup and cross-border fees.

Most founders never notice because the conversion happens before the money even appears in their account. You see a number, you move on. But those compounding losses on every single transaction add up to thousands over a year of money that could have funded your next hire, your next ad campaign, or three more months of runway.

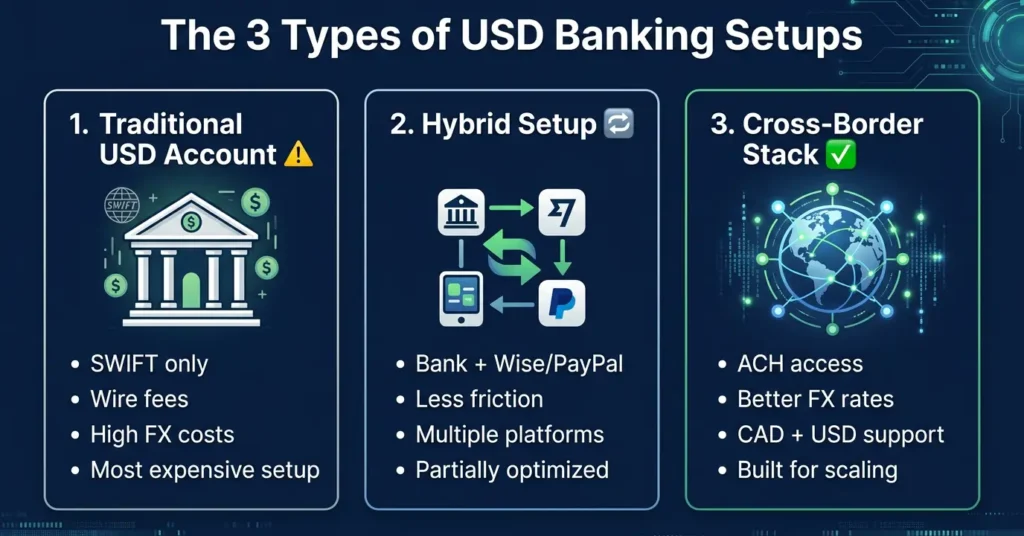

The 3 Types of USD Banking Setups

Before choosing an account, it helps to know which category you’re currently operating in.

Traditional USD Account (Most Common, Least Optimized)

This is a USD account at a Canadian Big 5 bank. It holds US dollars, but it sits on SWIFT infrastructure. Every incoming payment costs you wire fees. Every conversion costs you an FX spread. It’s the default most founders end up with because it’s convenient and it’s quietly the most expensive option on this list.

Hybrid Setup

Some founders pair a Canadian bank account with Wise or PayPal for international transfers. This reduces some friction, but it’s not fully optimized. You’re still managing multiple logins, multiple reconciliations, and not getting the benefit of true ACH rails or integrated CAD and USD in one platform.

True Cross-Border Stack (Where You Want to Be)

This is an account with real US routing and account numbers, ACH access, competitive FX rates, and full support for Canadian payment rails like Interac, CRA payments, and payroll. This is the infrastructure modern Canadian startups are building on and understanding why small businesses fail to grow often comes back to exactly this kind of operational inefficiency hiding in plain sight.

The Stripe Trap: How Founders Lose Revenue Without Realizing

If your payment infrastructure runs through Stripe and you don’t have a true US account with ACH details, you’re paying a 1.5% cross-border fee on every payout. That’s Stripe treating your account as international, not domestic.

| Setup | Stripe Payout Fee | Settlement Speed | Hidden FX Cost |

| Canadian USD Account (SWIFT-only) | 1.5% cross-border fee | 2 to 3 days | Yes (2 to 4%) |

| ACH-Enabled Cross-Border Account | None | Next business day | Minimal (0.25 to 0.5%) |

For an e-commerce brand with $50,000 in weekly USD revenue, Stripe’s cross-border payout fee alone costs $750 weekly, or $3,000 monthly. Depositing into a true US account eliminates this fee entirely. That’s $36,000 a year. Not from a bad product decision. From a banking default, you never questioned.

Try this: Log in to your Stripe dashboard and check your payout destination. If it’s a Canadian bank account, even one labeled “USD,” you’re almost certainly paying the cross-border fee. Switch that to an ACH-enabled US account and the fee disappears immediately.

What to Look for in a USD Cross-Border Bank Account

True US Banking Details

The single most important feature is whether the account comes with a US routing number and a US account number. Without these, you cannot receive ACH payments, you cannot eliminate Stripe’s cross-border fee, and US clients sending you standard domestic transfers will trigger wire fees on your end.

Transparent FX Rates vs. Hidden Spreads

Ask your current provider for the mid-market rate on your last conversion and compare it to what they actually gave you. Providers like Wise publish their rates openly. Traditional banks bury theirs. The gap between those two numbers is your actual FX cost and it should inform every conversation you have with a potential banking partner.

Dual Infrastructure: USD and CAD Under One Roof

This is where a lot of fintech platforms fall short for Canadian founders. You need a provider that handles US payment rails AND Canadian ones, meaning Interac e-Transfer, CRA tax payments, and domestic payroll. Some international platforms are great for USD but require a separate Canadian bank account to handle anything domestic. That creates friction, reconciliation headaches, and split workflows. As part of your broader smart reinvestment strategies, keeping your financial operations lean and centralized matters.

Integrations That Reduce Manual Work

Stripe, Shopify, QuickBooks, Xero. If your banking platform doesn’t talk to the tools you’re already using, you’ll spend hours every month manually reconciling what should reconcile itself. This is not optional infrastructure. It’s the difference between a finance function that scales and one that breaks under growth.

The Best USD Cross-Border Bank Accounts for Canadian Startups in 2026

| Provider | Best For | FX Markup | ACH Access | Monthly Fee |

| Venn | All-in-one Canadian startups | ~0.25% | Yes | Tiered |

| Wise Business | Freelancers and low volume | ~0.45% | Yes | $0 |

| Airwallex | Ecommerce and SaaS scaling | 0.3 to 0.6% | Yes | $0 base |

| RBC Bank (US) | Traditional banking users | 1.5 to 2.5% | Yes | $0 to $15 |

| EQ Bank USD | USD reserve strategy | N/A | No | $0 |

Venn: Best Overall for Canadian Startups

Venn offers local CAD and USD account functionality, interest on balances, corporate cards, low FX rates, and accounting integrations in one platform, making it the top pick for startups, agencies, ecommerce brands, and modern service businesses in 2026.

What sets Venn apart is that it’s built specifically for Canadian businesses operating across borders. You get real Canadian bank rails (Interac, CRA, payroll) alongside a true US account with ACH. The FX markup sits around 0.25%, a fraction of what traditional banks charge. For a startup running $20,000 to $100,000+ in monthly USD revenue, this is the most complete option on the market right now.

Best for: Founders who want everything in one place, Canadian banking plus real USD infrastructure, without stitching together multiple tools.

Wise Business: Best for Simplicity and Transparency

Wise charges no monthly fees and uses the mid-market exchange rate as standard, making it one of the most transparent options for Canadian businesses sending and receiving money internationally. FX fees start from around 0.33 to 0.45%, and the platform gives you local account details in multiple currencies, including USD.

The tradeoff: Wise doesn’t fully replace a Canadian bank account. It doesn’t support CRA payments or domestic payroll through EFT, which means many founders need to run it alongside a traditional account. It’s genuinely excellent for what it does but it’s a payment tool, not a complete banking stack.

Best for: Freelancers, consultants, and early-stage startups with straightforward international payment needs and lower transaction volumes.

Airwallex: Best for High-Volume Ecommerce and Global Scaling

Airwallex has built its own network of local payment rails that bypass SWIFT in over 120 countries, meaning approximately 93% of transfers arrive on the same day and the exact amount sent is the exact amount received, with no intermediary deductions.

The platform supports over 160 payment methods, integrates with Shopify and WooCommerce, and provides advanced expense management tools that scale well with growing teams. FX starts at 0.5% for major currencies. It’s slightly more complex than Wise and more oriented toward businesses with higher transaction volumes.

Best for: E-commerce brands and SaaS companies processing significant international volume, especially those with suppliers or contractors in multiple countries.

RBC Bank (US): Best Traditional Option

RBC Bank is the only US-based bank designed specifically for Canadians, offering free instant transfers up to $25,000 between RBC Royal Bank Canada and RBC Bank US accounts 24/7, with no delay or wire fees. You don’t need a US address or Social Security Number to open an account, and your US funds are FDIC insured.

The downside is cost. Monthly fees run approximately $150 for full business accounts, significantly higher than fintech alternatives, and the banking experience follows traditional patterns; branch visits may be required for certain transactions.

Best for: Startups already deeply integrated with RBC in Canada, or founders who need the security of a recognized institutional bank alongside their US operations.

EQ Bank USD Account: Best for Holding USD Reserves

EQ Bank’s USD account isn’t a transactional account; it’s a high-interest parking spot for USD capital you don’t need to move immediately. EQ Bank’s USD account has no monthly fees, no transaction costs, and an interest rate that leaves competitors behind, making it the strongest choice for holding US cash between uses.

It doesn’t have ACH access or US routing numbers, so it won’t replace your operating account. But as a reserve strategy holding USD runway while earning meaningful interest, it’s genuinely useful as part of a two-account stack.

Best for: Startups holding significant USD reserves between projects, funding rounds, or seasonal cycles.

Which Account Should You Choose? A Quick Decision Framework

| Your Business Model | Best Starting Point |

| SaaS or subscription (Stripe-heavy) | Wise or Airwallex |

| Agency or consulting (wire payments) | Venn |

| Ecommerce scaling fast | Airwallex |

| Prefer traditional banking structure | RBC Bank (US) |

| Holding USD runway or reserves | EQ Bank + operational account |

Most growing Canadian startups end up with a two-account setup: one true cross-border operating account (Venn, Wise, or Airwallex) and one reserve account (EQ Bank) to earn interest on idle capital. Understanding NLP for entrepreneurs teaches you that decisive, clear decision-making, including financial decisions, is a skill you build, not just a one-time choice.

Data & Findings: What the Numbers Actually Say

The cost of poor cross-border banking isn’t theoretical; it’s measurable, and the numbers are significant. Float Financial’s 2026 analysis of FX costs for Canadian businesses found that over 52% of Canadian SMBs struggle with high FX fees and poor exchange rates, and that managing CAD to USD exchange rate volatility is a challenge for 41% of Canadian businesses specifically. That number is rising as US tariff uncertainty continues to pressure the dollar.

On the fee side, Venn’s 2026 FX markup research shows that traditional Canadian bank FX markups range from 2% to over 4%, depending on currency pair and transaction volume and on a $100,000 USD transfer at a 3% spread, that’s $3,000 in lost value per transaction that never appears as a named line item. It gets worse when you factor in wire fees: Airwallex’s breakdown of what Canadian banks actually charge found that CIBC charges up to $80 per outgoing wire payment before the exchange rate markup is even applied.

For e-commerce founders running revenue through Stripe, the losses compound further. Venn’s 2026 startup banking guide modeled an e-commerce brand receiving $50,000 in weekly USD revenue and found it pays $750 per week in Stripe cross-border payout fees with a SWIFT-only account over $30,000 a year that disappears simply because the account lacks a US routing number. Switching to an ACH-enabled account eliminates that fee entirely. Across all business types, Venn’s 2026 US bank account comparison for Canadians puts the annual cost gap between a traditional Big 5 USD account and a true cross-border account at $500 to $5,000+, depending on revenue volume and transaction frequency.

The transparency problem runs deeper than most founders realize. Trolley’s 2026 guide to cross-border payment fees explains that most traditional banks layer a 2 to 3% spread above the mid-market rate and then charge a separate wire fee on top, a double cost that most finance teams never fully audit because neither charge is clearly labeled. Modern fintech platforms have largely solved this, offering rates within 0.33 to 0.5% of the mid-market with no hidden spread. And the market is paying attention: Airwallex’s Canadian market research found that 83% of Canadian SMEs say they would switch to a bank that matched the service and experience of modern fintech platforms. The founders making that move in 2026 are quietly building a structural cost advantage over those still running on the Big 5 default.

Common Mistakes Canadian Founders Make With USD Banking

Getting the account wrong is rarely about ignorance. It’s about assumptions that nobody ever questioned. Here are the four patterns I see most often.

Assuming a USD account is a US account

A USD account at a Canadian bank holds US dollars but operates on SWIFT, not ACH. It’s not functionally the same as a US account, and the difference costs you every time a payment crosses the border.

Ignoring ACH capability

Most founders ask about fees. Almost none ask about ACH. That’s the wrong question order. ACH capability is the infrastructure. Fees are just a number on top of it.

Accepting the default Stripe setup

Stripe will connect to whatever bank account you give it. It won’t tell you you’re losing 1.5% on every payout. You have to go find that out yourself and then fix it.

Treating FX as an unavoidable cost

Over half of Canadian SMBs struggle with high FX fees and poor exchange rates, but most founders treat it as a fixed cost of doing business. It isn’t. It’s a negotiable, changeable variable and modern fintech platforms have already solved it.

Banking as Financial Architecture, Not Admin

Here’s the reframe that matters: your banking setup isn’t paperwork. It’s part of your growth infrastructure. A startup recovering $5,000 a year in unnecessary fees has just found money to fund another month of runway, a new contractor, or a better ad test. That’s not accounting. That’s strategy.

I work with Canadian founders who are brilliant at building their product and leading their team and then quietly lose 3% of every USD dollar they earn to an account they opened in year one and never revisited. Goal setting for business growth has to include your financial infrastructure. The founders who scale fastest aren’t just the ones with the best product. They’re the ones who eliminate friction from every part of their operation, including the parts most people overlook. And if you want a framework for building that kind of business clarity end-to-end, business coaching for Toronto entrepreneurs is a great place to start.

Frequently Asked Questions

Can a Canadian business open a US bank account?

Yes. Several options exist specifically for Canadian businesses and require neither a US address nor a Social Security Number. RBC Bank (US), Wise, Airwallex, and Venn all allow Canadian-incorporated businesses to access true USD accounts with US routing details. Requirements vary by provider but are typically straightforward for incorporated businesses.

What’s the difference between a USD account and a US bank account?

A USD account at a Canadian bank holds US dollars but runs on SWIFT infrastructure. A US bank account has real US routing numbers and connects to ACH the domestic US payment rail. The practical difference is wire fees, settlement speed, and whether Stripe treats your payouts as domestic or international.

Do I need a US address or SSN to open a USD cross-border account?

Not with most modern fintech options. Venn, Wise, and Airwallex all serve Canadian-incorporated businesses without requiring US residency documentation. RBC Bank (US) also waives the SSN requirement for Canadians. Some traditional US banks do require a US address, so it’s worth confirming before applying.

How does Stripe treat Canadian USD accounts?

If your Stripe payout account doesn’t have a US routing number, Stripe classifies the transfer as cross-border and applies a 1.5% fee. This is not labeled clearly in most Stripe dashboards. Switching to an ACH-enabled account with a real US routing number removes this fee immediately.

Which account is best for a Canadian startup just getting started?

Wise is the easiest entry point for early-stage founders with lower volume; it has no monthly fees, transparent FX rates, and a clean interface. As revenue grows and you need full Canadian banking functionality alongside USD, Venn or Airwallex become the stronger long-term choices.

Start Treating Your Banking Like a Growth Decision

The wrong USD account is a slow leak. You won’t feel it today, but over 12 months, it quietly costs you thousands in fees, FX markups, and lost revenue that never had a chance to compound. The right account isn’t just cheaper, it’s faster, cleaner, and built for the kind of business you’re actually trying to build.

Three things to take from this: audit your current FX costs against the mid-market rate, check whether your Stripe payouts are hitting an ACH account, and match your banking setup to your actual business model rather than the default you signed up for in year one.

You’ve built something worth protecting. Your financial infrastructure should reflect that.

If you want to build the bigger picture, the mindset, the systems, and the strategic clarity that makes every decision compound over time, explore what business coaching can do for Canadian entrepreneurs and let’s take the next step together.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.