You walk into your branch. You’ve been a personal banking client for eight years. You have revenue coming in, a registered business, and a clear plan. You sit down with the advisor and ask about a business line of credit. They look at your file, ask a few questions, and tell you they’ll need more history before they can help.

You leave empty-handed. Not because your business isn’t real, but because you hadn’t built the foundation they were looking for.

Here’s what most people get wrong: they believe building business credit in Canada requires years of tradelines, multiple vendor accounts, and a stack of paperwork. In reality, your fastest path runs straight through the bank you already bank with, if you know how to structure the relationship strategically.

Key Takeaway:

- Fast-tracking business credit in Canada depends more on financial readiness than just credit score lenders prioritize consistent revenue, clean banking activity, and clear repayment ability. [1]

- Banks typically require stronger documentation and longer approval times, while alternative lenders can provide funding within 24–72 hours based on cash flow and transaction data. [2]

- Common eligibility benchmarks include 6–12 months in business, steady monthly revenue, a credit score around 600+, and a registered Canadian business with an active bank account. [3]

- Building business credit quickly requires separating personal and business finances, using credit products responsibly, establishing trade lines, and maintaining consistent on-time payments. [4]

- The fastest approvals happen when businesses are “funding-ready” with organized financials, clear use of funds, and strong cash flow visibility that reduces perceived risk for lenders.

Bottom Line: Fast business credit in Canada comes from preparation, not shortcuts. Businesses that show stable revenue, clean financial behavior, and clear repayment ability can access funding quickly through the right mix of banks and alternative lenders.

- Source: Building Business Credit for Equipment Financing (Canada)

- Source: Finder – Fast Business Loans in Canada

- Source: Business Financing Requirements Canada

- Source: Business Credit Building Guide Canada

In this article, you’ll get a concrete roadmap for building business credit fast using your primary Canadian bank. Not someday. Starting this week.

Why Your Primary Bank Relationship Is Your Fastest Path to Business Credit

Most guides treat Canadian banks as passive providers, institutions you apply to and hope for the best. That framing is costing you time and opportunity.

Your bank isn’t just evaluating your application. It’s evaluating your behavior over time.

What Banks Are Actually Looking At

Canada’s Big 6 banks, Royal Bank of Canada (RBC), Toronto-Dominion Bank (TD), Bank of Montreal (BMO), Scotiabank, Canadian Imperial Bank of Commerce (CIBC), and National Bank, all use internal scoring models that go well beyond your credit score. They’re looking at account behavior: how consistent your deposits are, whether your balance is predictable, whether you’ve ever overdrafted, and how long you’ve been in the relationship.

Research from Merchant Growth points out that only 18% of Canadian small businesses requested debt financing in recent years, suggesting most entrepreneurs either don’t understand how to qualify or assume the answer will be no before they even ask.

The businesses that get approved fastest aren’t always the most profitable. They’re the ones that have shown their bank a clear, consistent financial picture over time.

How Existing Personal Clients Get an Edge

This is the part nobody talks about enough. If you’ve been a personal banking client with RBC, TD, or BMO for several years, you already have goodwill in the relationship. TD and RBC are consistently rated highest for small business support and relationship management among Canada’s major banks, and part of that reputation comes from how they treat clients who demonstrate financial discipline over time.

Relationship managers advocate internally for clients they trust. Building business credit isn’t just a financial exercise. It’s a trust-building process, and your primary bank is the smartest place to start that trust.

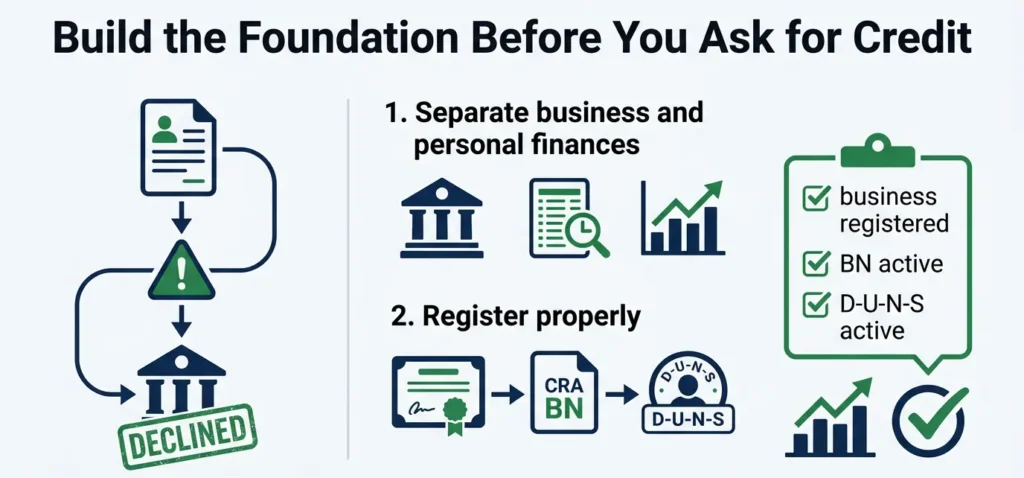

Build the Foundation Before You Ask for Credit

The mistake most entrepreneurs make is jumping straight to the application. Before you ever request a credit product, you need a clean foundation in place. Skipping this is exactly why capable business owners get turned down.

Separate Your Business and Personal Finances From Day One

This step is non-negotiable. Open a business chequing account under your registered business name and route all business revenue and expenses through it. Mixing personal and business funds doesn’t just create accounting headaches. It signals to your bank that the business isn’t treated as its own entity. That’s a credibility problem.

From day one, use the business account consistently. Not occasionally. Every transaction through that account is a data point in your bank records. Frequency and consistency matter more than balance size in the early stages.

Register Properly and Get Your Business Number and DUNS Number

Make sure your business is properly registered with your province and has a Business Number (BN) from the CRA. Then apply for a free D-U-N-S Number through Dun and Bradstreet Canada. This number establishes your business credit file and allows lenders and vendors to report your payment history to the commercial bureaus. It takes minutes to apply and is one of the most overlooked steps in the process.

Try This: Block 30 minutes this week to confirm your business is registered, your BN is in order, and your D-U-N-S Number is active. These are the three pillars your bank and bureaus need to even start tracking your progress.

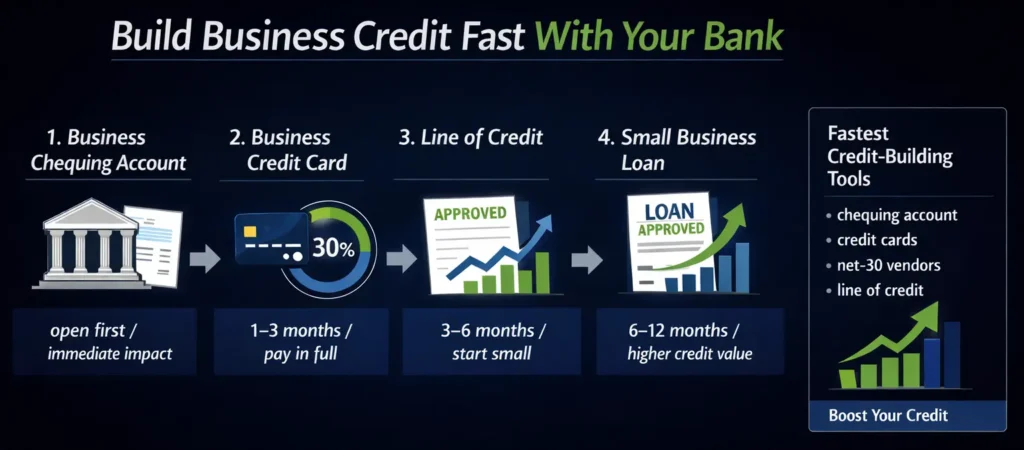

What Steps Build Business Credit Fast With Your Bank?

Here’s where strategy turns into action. These four steps, done in sequence and done consistently, are how you compress the timeline and accelerate your business credit profile with your primary Canadian bank.

Credit-Building Products at a Glance

| Product | Time to Impact | Difficulty | Credit-Building Value | Best First Move |

| Business Chequing Account | Immediate | Easy | High | Yes, open this first |

| Business Credit Card | 1 to 3 months | Easy | High | Yes, apply within 30 days |

| Business Line of Credit | 3 to 6 months | Moderate | Very High | After 6 months of account history |

| Vendor / Net-30 Accounts | 1 to 3 months | Easy | Moderate | Alongside your credit card |

| Small Business Loan | 6 to 12 months | Hard | Very High | After line of credit is established |

Step 1: Open a Business Chequing Account and Use It Actively

If you haven’t already, open a business bank account specifically designed for your business type. Then use it daily. Avoid overdrafts at all costs, because even a single overdraft on a business account sends a warning signal that your cash flow isn’t managed well. Maintain a consistent minimum balance, not because the bank requires it (though some accounts do), but because it demonstrates financial stability. Deposit revenue regularly and predictably rather than in large, irregular lump sums. Banks trust consistent patterns.

Step 2: Apply for a Business Credit Card and Pay It in Full Every Month

A business credit card is one of the fastest ways to start building a business credit profile. Choose one from your primary bank that reports to commercial bureaus like Equifax Business. Use it for regular, predictable expenses such as software subscriptions, office supplies, and fuel. Keep your credit utilization below 30% of your limit. Every month, pay the full balance. No exceptions. After six months of clean behavior, call your bank and ask for a credit limit increase. This is how you gradually grow your available credit without adding risk to your profile.

Step 3: Request a Small Business Line of Credit Early

This is where framing matters enormously.

When you talk to your bank about a line of credit, the words you use signal your level of financial sophistication. There’s a real difference between these two approaches:

- “I need money to grow my business.”

- “I’d like to establish a small credit facility to manage cash flow predictably.”

The second version positions you as a disciplined operator, not a business in distress. Start small. A $5,000 to $15,000 line of credit is not a large ask, but it creates a credit product that gets reported and adds to your profile. Use it occasionally and pay it back quickly. The goal at this stage isn’t to borrow. It’s to demonstrate that you can.

You can also explore government-backed programs like the Canada Small Business Financing Program through your bank, which reduces the lender’s risk and can make early approvals easier for new businesses.

Step 4: Build Transaction History Through Consistent Revenue Deposits

Your bank account activity is your financial story. Deposit revenue consistently, not in unpredictable bursts. Avoid large unexplained cash movements. Keep your account in good standing across every product you hold with that bank. The relationship between your chequing account behavior and your credit applications is invisible to most business owners, but it’s one of the first things a relationship manager checks when your application comes across their desk.

Try This: Schedule a 15-minute conversation with your bank’s small business advisor this week. Use this framing: “I want to start structuring my banking relationship to support my business credit over the next 12 months. What would you recommend?” That single conversation often opens doors most entrepreneurs don’t even know exist.

How Long Does It Take to Build Business Credit in Canada?

Let’s be direct about the timeline, because too many resources either oversell speed or leave you with unrealistic expectations.

The Realistic Timeline

During the first six months, your job is infrastructure: business account open and active, business credit card in use, D-U-N-S Number secured, and consistent deposit behavior established. You’re not going to qualify for large financing yet, and that’s fine. You’re building the foundation.

From six to twelve months, your credit profile starts taking shape. Vendors who report to credit bureaus are adding payment history. Your bank is seeing predictable account behavior. A new company typically needs at least two years to establish business credit strong enough for a traditional bank loan, but the two-year mark arrives a lot faster when you’re doing the right things from day one.

After year two, you start to unlock the real benefits: better loan terms, higher credit limits, and reduced reliance on personal guarantees.

How to Compress the Timeline

You can accelerate the process in a few concrete ways. First, leverage your existing personal banking relationship, since clients with long-standing personal accounts get faster trust. Second, increase your monthly transaction volume by routing all business spending through your bank’s products. Third, hold multiple products with the same institution: a chequing account, a credit card, and a line of credit. Banks score relationship depth, not just individual products.

Businesses with strong credit profiles are 41% more likely to be approved for bank loans. The gap between you and that number closes every month you operate cleanly.

How Does a Canadian Business Credit Score Work?

Understanding this helps you stop guessing and start managing your score deliberately.

Equifax and TransUnion Business Scores

Canada’s two major credit bureaus, Equifax and TransUnion, both produce business credit scores for Canadian business owners. Scores typically run on a scale from 0 to 100. A score of 80 or higher is considered favourable to most lenders. The calculation takes into account payment history, outstanding debt, credit mix, and time in business. Both bureaus use slightly different methods, so it’s worth monitoring your profile across both. Many Canadian banks now provide credit score information directly through their business banking portals, so check yours regularly.

The DUNS Number and PAYDEX Score

Dun and Bradstreet issues the PAYDEX score, which measures your business payment performance on a 0 to 100 scale. Here’s a detail most entrepreneurs miss: early payments actually score higher than on-time payments. So if you’re managing vendor accounts and trade credit, paying a few days early is a simple, zero-cost way to build a stronger score than your peers who pay on the due date.

Common Mistakes That Slow Down Your Business Credit

Darren came to James feeling completely stuck. He had a legitimate business, was earning a decent income, and still couldn’t break through to the financial opportunities he wanted. As James worked with him through NLP goal-coaching, a pattern emerged: Darren’s financial avoidance and inconsistent behavior were invisible to him but completely visible to lenders. Once he addressed the underlying beliefs driving that behavior, his financial actions became deliberate and consistent. His business relationships, bank relationships included, shifted as a result.

The mindset piece matters more than most financial guides will admit. Here are the behaviors that sabotage business credit, and most of them are fixable with a decision, not years of work.

Mixing Personal and Business Funds

This is the single most common mistake. It makes your business look unreliable and creates a CRA audit risk. Separate accounts, separate cards, separate financial identity.

Working With Vendors Who Don’t Report to Bureaus

Not all vendors report payment history to commercial credit bureaus. If your goal is to avoid the patterns that cause small businesses to stall, prioritize vendor relationships with suppliers who actually report. On-time payments only build your profile if someone is tracking them.

Ignoring Your Business Credit Report

Errors are more common than you’d think. Pull your business credit report regularly from Equifax Business and check for inaccuracies. A disputed error can take weeks to resolve, and finding it early keeps it from blocking a future application at the worst possible moment.

Data and Findings

The numbers behind business credit in Canada tell a story most entrepreneurs haven’t read, and that gap is costing them.

According to Innovation, Science and Economic Development Canada, only 18% of Canadian small businesses requested debt financing in a recent reporting period. That means the vast majority of business owners either don’t know how to qualify, assume the answer will be no, or haven’t built the foundation to ask confidently. The opportunity in that gap is significant for anyone willing to do the groundwork.

The approval odds shift dramatically once a business establishes its credit profile. Businesses with strong credit are 41% more likely to be approved for bank loans compared to those with thin or unestablished credit files. That’s not a marginal edge. It’s the difference between accessing capital when growth demands it and being turned away when timing matters most.

On the scoring side, Canadian business credit operates on a 0 to 100 scale across both Equifax Business and TransUnion. A score of 80 or higher is the benchmark most lenders consider favorable. Yet many business owners have never pulled their own business credit report, let alone taken deliberate steps to move their score into that range.

The timeline data is equally instructive. Most new businesses need at least 12 to 24 months of consistent financial behavior before a traditional Canadian bank will approve them for a standard business loan. However, businesses that open a dedicated account, secure a business credit card, and maintain a clean transaction history from month one consistently reach that threshold faster than those who start late or build inconsistently.

From James’s work with business coaching clients, a recurring pattern emerges: the entrepreneurs who stall financially are often not lacking in revenue or ambition. They’re lacking in structured financial behavior, the consistent, bank-visible actions that turn a good business into a creditworthy one. When that behavior shifts, the financial results follow.

Frequently Asked Questions

How long does it take to build business credit with a Canadian bank?

Most new businesses need 12 to 24 months of consistent financial behavior before qualifying for traditional bank financing. You can compress that timeline by opening a business account immediately, using a business credit card responsibly, and maintaining clean, predictable account activity from day one. The relationship you build with your primary bank in the first year pays dividends for years after.

What credit bureau does Canada use for business credit?

Canada’s two primary commercial credit bureaus are Equifax Business and TransUnion. Dun and Bradstreet also tracks business credit and issues the PAYDEX score, which is particularly relevant for trade credit relationships. Scores across all bureaus are influenced by payment history, credit utilization, and time in business.

Does a business bank account help build business credit in Canada?

Yes, directly. A business chequing account at one of the Big 6 banks establishes your business as a separate financial entity, creates transaction history that lenders review when evaluating applications, and is typically a prerequisite for accessing business credit cards and lines of credit through the same institution. Consistent, active use of the account strengthens your profile over time.

What should I say to my bank when applying for business credit?

Frame your request around cash flow management, not financial need. Instead of “I need a loan to grow,” try “I’d like to establish a small credit facility to manage cash flow predictably as my business scales.” This positions you as a disciplined operator and reduces the perceived risk for your lender. Starting small and demonstrating responsible use is always the most effective long-term strategy.

What is a good business credit score in Canada?

Both Equifax and TransUnion use a 0 to 100 scale for business credit scores in Canada. A score of 80 or higher is generally considered favorable by lenders. Consistent on-time payments, low credit utilization, and a diversified mix of credit products are the primary factors that push your score into that range.

Conclusion

Building business credit fast in Canada isn’t about shortcuts. It’s about doing a small number of things consistently, in the right sequence, with the institution that already knows you.

Your primary Canadian bank is your most powerful ally in this process, but only if you approach the relationship proactively. Open your business account and use it actively. Get your business credit card and pay it in full. Request a small line of credit early and frame it as a cash flow tool. Keep your account behavior clean and predictable. And talk to your bank’s small business advisor before you need credit, not after.

The entrepreneurs who access financing when they need it aren’t lucky. They’re prepared. You can be too.

If you’re ready to pair financial strategy with the mindset work that actually makes it stick, James’s business coaching programs are built for exactly this. The goal isn’t just better credit. It’s a business and a version of you that operates with real clarity and confidence at every stage of growth.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.