To qualify for a 2026 federal small business loan in Canada, your business must operate in Canada as a for-profit entity, generate under $10 million in annual gross revenue, and offer goods or services to the public. The primary program is the Canada Small Business Financing Program, which guarantees up to 85% of a lender’s risk and offers financing up to $1.15 million. Applications go through banks, credit unions, or caisses populaires, not directly to the government. Startups, including pre-revenue businesses, are eligible. The program covers equipment, leasehold improvements, software, intangible assets, and working capital costs through a separate line of credit

Most Canadian service business owners assume government loan programs are built for manufacturers, retailers, and construction companies. If you run a consulting practice, a coaching business, or a digital agency, you have probably written off federal financing without looking closely at the rules. That assumption is costing you access to some of the most affordable capital available in Canada.

Key Takeaway:

- To qualify for a small business loan in Canada, your business must typically operate in Canada, generate revenue (or show a viable plan), and meet lender criteria such as creditworthiness, cash flow stability, and repayment capacity. [1]

- Government-backed programs like the Canada Small Business Financing Program (CSBFP) require businesses to have under $10 million in annual revenue and operate as a for-profit entity (with some exceptions). [1]

- Lenders evaluate key factors including time in business, credit score, financial statements, business model viability, and how the loan will be used (e.g., equipment, working capital, expansion). [2]

- Startups can qualify, but often need a strong business plan, personal guarantee, and clear revenue projections since most traditional lenders prefer at least 1–2 years of operating history. [2]

- Approval ultimately depends on risk: businesses with consistent cash flow, clear repayment ability, and realistic funding use cases are significantly more likely to get approved.

Bottom Line: Small business loan eligibility in Canada is less about size and more about risk. If your business shows stable cash flow, a clear plan, and the ability to repay, your chances of approval increase significantly even as a startup.

- Source: Canada Small Business Financing Program Guide (2026)

- Source: GrantHub – Business Loan Eligibility in Canada

Accessing funding is consistently ranked as the top barrier to small business growth in Canada. The Canada Small Business Financing Program has backed more than 53,000 businesses with over $11 billion in loans over the past decade. Yet it remains one of the most underused programs in the country, largely because owners do not know they qualify.

In a tighter lending environment where banks scrutinize applications more closely, understanding federal small business loan eligibility in Canada is not optional. It is a competitive advantage. This guide walks through every eligibility gate, every document requirement, and every step of the application so you leave knowing exactly where you stand.

2026 Economic Context: Why Federal Loan Programs Matter More Than Ever

Canada’s lending environment has shifted. With the Bank of Canada’s prime rate sitting at 4.45% as of early 2026, conventional commercial loans carry rates that squeeze cash flow before a business has a chance to grow.

Under the CSBFP, interest rates are capped. Variable-rate term loans max out at prime plus 3%, putting the ceiling at 7.45%. The gap between a capped CSBFP rate and a standard commercial loan can translate to tens of thousands of dollars in unnecessary interest, as financing analysts tracking the program have noted. Compare that to BDC interest rates running at 11 to 13% in 2026, depending on borrower profile.

Beyond rates, lenders are applying tighter credit standards across the board. The 85% government guarantee is what changes the conversation. It reduces a lender’s exposure from 100% to 15% on eligible losses if you default. That shift in risk profile is what gets service businesses approved when conventional lending would say no.

What Is the Canada Small Business Financing Program (CSBFP)?

The CSBFP is a federal loan-guarantee program administered by Innovation, Science and Economic Development Canada (ISED). It does not lend money directly. Instead, the government shares risk with participating banks, credit unions, and caisses populaires to make lenders more willing to approve businesses they might otherwise pass on. According to the official ISED program guidelines, the maximum financing available is $1.15 million per borrower: up to $1 million in term loans and up to $150,000 as a line of credit.

How the Guarantee Works

When a bank considers a standard loan, it bears 100% of the loss if you default. Under the CSBFP, the federal government covers up to 85% of eligible losses. That one change in risk structure is why startups, newer businesses, and service companies with limited physical collateral can access capital they would otherwise be denied.

You still apply through a financial institution. The lender handles the underwriting, makes the approval decision, and manages your loan. ISED registers the loan on the backend once it is approved.

2026 Key Updates

The intangible asset category now allows financing of up to $150,000 for software, licenses, patents, trademarks, website development costs, and other non-physical business assets. This sits within the $500,000 sub-limit for equipment and leaseholds. For service businesses, this update is significant. Tools that run your operation, CRM systems, and custom software now qualify.

Federal Small Business Loan Eligibility in Canada: 2026 Requirements

The Core 3 Eligibility Rules

Your business must meet three conditions to qualify for federal small business loan eligibility in Canada:

- Operate in Canada, with a physical place of business and assets in Canada

- Generate gross annual revenues under $10 million at the time the loan is approved

- Be a for-profit entity offering goods or services to the public

For new businesses, the $10 million revenue threshold applies to estimated gross revenues during the first 52 weeks of operation. Pre-revenue startups are eligible. Startups account for roughly 74% of all CSBFP lending.

Eligible Business Structures

The CSBFP covers a wide range of legal structures: sole proprietors, partnerships, corporations, including Canadian-Controlled Private Corporations, and cooperatives. Since 2021, not-for-profit organizations and registered charities have also been eligible. Legal analysis from Devry Smith Frank LLP confirms that businesses owned by foreign nationals qualify, provided the business itself operates in Canada.

Who Is NOT Eligible

Farming businesses are excluded from the CSBFP. The Canadian Agricultural Loans Act Program handles government-backed financing for that sector. Passive investment companies and businesses that do not offer goods or services to the general public are also ineligible.

Quick Eligibility Checklist

Before approaching a lender, confirm you can check all of these:

- Business is registered and operating in Canada

- Annual gross revenue is under $10 million (or estimated under $10 million for new businesses)

- Business is a for-profit entity

- Businesses offer goods or services to the public

- Personal credit score is approximately 680 or higher

- You have a clear, documented use of funds

If you check all six, you are likely eligible. The next step is choosing the right lender.

Do Service Businesses Qualify for Federal Loan Programs?

Yes. Service businesses qualify for the CSBFP, and the 2026 updates make the program more accessible to them than ever before.

What “Services to the Public” Actually Means

The eligibility language around offering goods or services to the public does not require a storefront or physical inventory. Consulting firms, coaching businesses, marketing agencies, financial advisory practices, and professional service providers all qualify. The standard is whether your business has customers it serves, not whether it manufactures a product.

The 2026 Advantage: Intangible Assets

This is where service businesses gain the most ground. The intangible asset category allows financing for software, whether custom-built, off-the-shelf, or mobile applications, as well as website development costs, patents, trademarks, franchising fees, and digital infrastructure. If your business runs on technology and intellectual property rather than machinery and real estate, there is now a clear financing path for those assets under federal small business loan eligibility in Canada.

What Can You Use a Federal Small Business Loan For?

Eligible Uses

Term loan funds can be applied to: purchasing or improving land and commercial buildings, leasehold improvements such as renovations to a leased space, equipment and machinery, vehicles used in business operations, and intangible assets, including software and digital tools. Lenders typically finance up to 90% of eligible purchase costs, meaning you contribute the remaining 10%.

Working Capital: The Line of Credit

The $150,000 line of credit component is specifically for working capital: day-to-day operating expenses, including payroll, inventory, marketing, and rent. Not all lenders have rolled out this product. If you need working capital coverage, ask specifically whether the institution offers the CSBFP line of credit option before assuming it is unavailable.

The 365-Day Retroactive Rule

One of the most overlooked features of the program: purchases made within the 365 days before your loan approval date are eligible for retroactive financing. According to RBC’s CSBFP program documentation, if you bought equipment, software, or made leasehold improvements in the past year using credit cards or cash, you may be able to recover that capital through a CSBFP loan. Ask your lender about this option before assuming it is off the table.

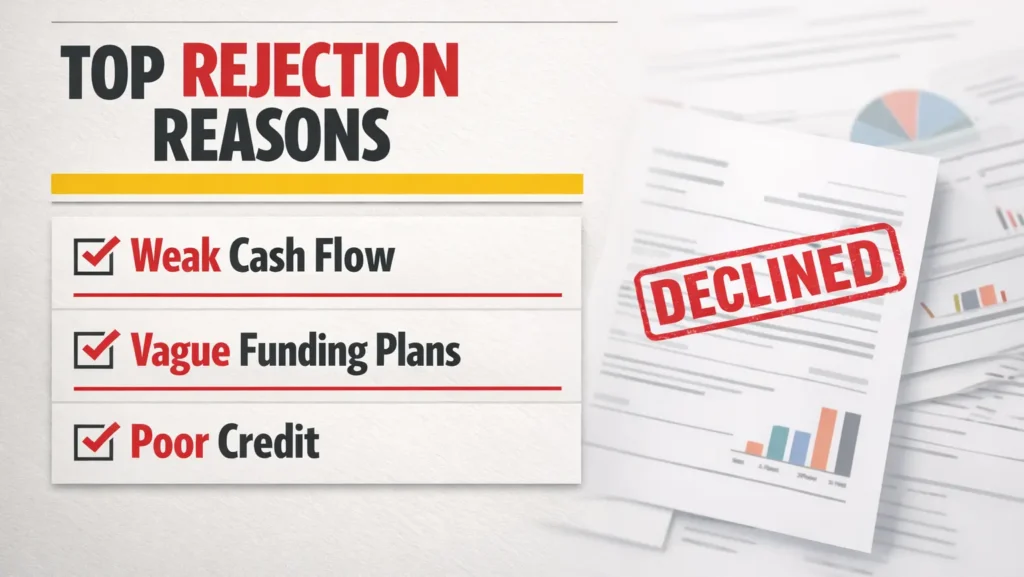

Why Most Canadian Entrepreneurs Get Rejected (Even When They Qualify)

The CSBFP improves your odds significantly, but it does not remove lender underwriting. Lenders still assess whether the deal makes sense. Most rejections come down to four issues.

First, a Debt Service Coverage Ratio below 1.2. This means projected business income does not clearly cover loan repayments by a safe margin. Second, a vague use of funds. “Business growth” is not a use of funds. Specific assets with documented price quotes are. Third, weak financial projections. Cash flow forecasts that lack stated assumptions or show unrealistic growth get flagged immediately. Fourth, poor credit positioning. Outstanding collections, recent missed payments, or unresolved tax issues reduce approval odds before underwriting even starts.

Key insight: Lenders do not reject risk. They reject unclear risk. A well-prepared application that shows exactly how funds will be used, what the repayment sources are, and how the business generates income will always outperform a technically eligible application with vague documentation

What Documents Do You Need Before You Apply?

Personal Documents

Bring a government-issued ID and a recent personal credit report. Lenders will pull credit regardless, but reviewing it first lets you address any errors or outstanding issues before they affect your application.

Business Documents

Established businesses need financial statements for the past two to three years, a current balance sheet, a detailed business plan, cash flow projections for the next 12 to 24 months, and documentation for the specific assets you plan to finance, including quotes, invoices, or purchase agreements.

For Startups Without Revenue History

If your business has no financial history, the application leans heavily on the strength of your business plan, market research, and projected cash flow. Show realistic assumptions, a clear customer acquisition model, and evidence that you understand your costs. Credit unions tend to be more flexible on startup applications than major banks.

How to Apply for a Federal Small Business Loan in Canada: Step by Step

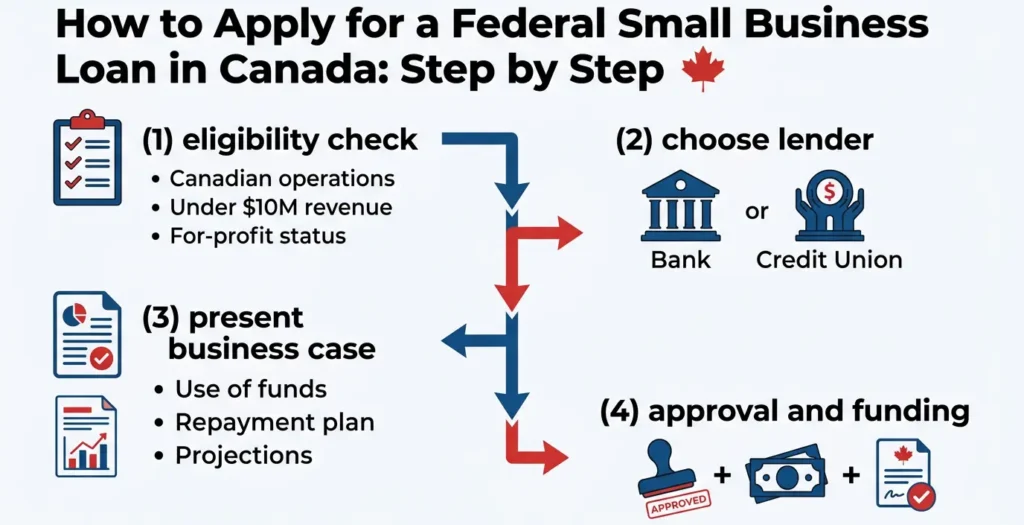

Step 1: Confirm Your Eligibility

Review the core three rules: Canadian operations, revenue under $10 million, and for-profit status. Check the quick eligibility list above. If you pass, pull your credit reports and address any outstanding issues before approaching a lender.

Step 2: Choose Your Lender Strategically

All major Canadian banks, including TD, RBC, CIBC, Scotiabank, and BMO, participate in the CSBFP, as do most credit unions and caisses populaires. Credit unions often apply more flexible internal criteria and are worth approaching if the big banks decline. Reviewing the best bank accounts for small businesses in Canada can help you identify where your banking relationship would be strongest before you apply.

Step 3: Present Your Business Case

Schedule a meeting with a business banking officer and arrive with a prepared proposal. Cover four things: what you need the funds for, the specific assets or costs being financed, your repayment plan, and your financial projections. Clear use of funds is the single most controllable factor in your approval odds.

Step 4: Approval and Funding

The lender reviews your application independently and makes the approval decision. ISED does not influence individual lending decisions. Once approved, the lender disburses the funds and registers the loan with ISED. The CSBFP application guide from Venn.ca notes that lenders now have six months from the date of first disbursement to register term loans with ISED, up from three months previously.

CSBFP vs. BDC: Which Program Is Right for You?

Both programs are federally supported and serve different needs. The Business Development Bank of Canada (BDC) operates as a complementary lender with a mandate to serve businesses that chartered banks may underserve. Here is how they compare:

| Program | Best For | Key Advantage | Rate (2026) | Max Amount |

| CSBFP | Asset-backed funding | 85% government guarantee; lower rates | Up to 7.45% | $1.15M |

| BDC | Cash-flow / no-collateral lending | Works with lenders who declined; no collateral required | 11-13% | $350,000 |

When to Choose CSBFP

Choose the CSBFP when you are financing a specific asset such as equipment, leasehold improvements, software, or real property. The government guarantee lowers your rate significantly and extends your repayment timeline up to 15 years. It is the stronger option if you have an established banking relationship and clear purchase documentation.

When to Choose BDC

BDC does not require collateral on its small business loans of up to $350,000. If your need is working capital, marketing, or expansion costs rather than asset acquisition, and your bank has declined, BDC is the next call to make. Their rates are higher, but their mandate is to take on more risk. According to Grant Compass’s 2026 BDC analysis, 68% of BDC’s portfolio serves businesses with under $2 million in annual sales, which makes it genuinely accessible to smaller service businesses.

Alternative Federal Support: Beyond Loans

SR&ED Tax Credit

If your business involves research, development, or technology innovation, the Scientific Research and Experimental Development (SR&ED) Tax Incentive Program offers a refundable tax credit that does not need to be repaid. The 2026 update raised the eligible expenditure limit to $6 million. SR&ED is not a loan; it is a credit applied against taxes owed, or refunded if your credits exceed your tax liability. It stacks with CSBFP financing and is worth exploring if your service business has a technology development component.

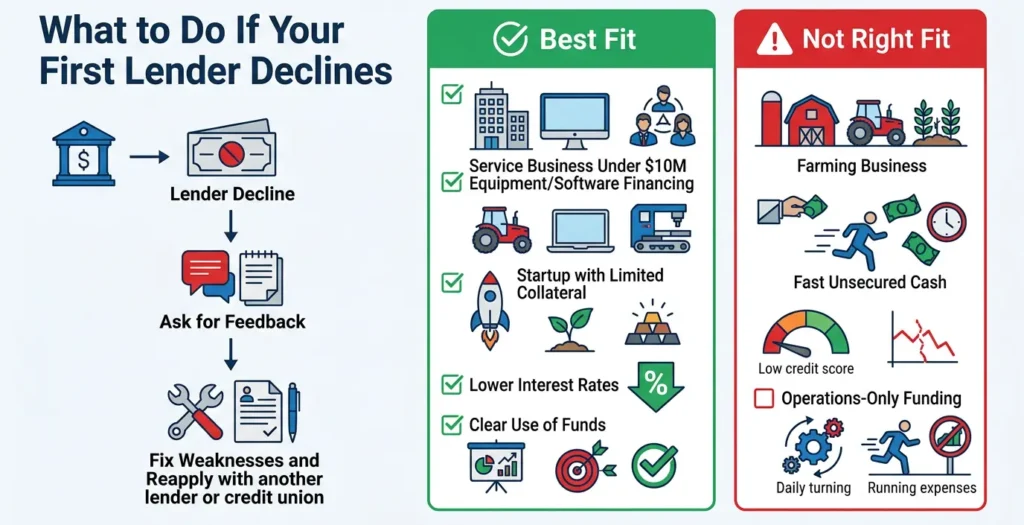

What to Do If Your First Lender Declines

A decline from one institution is not a program rejection. The CSBFP guidelines confirm that borrowers can apply with multiple lenders, and each institution applies its own internal criteria on top of the program requirements.

If your first lender says no, ask why. Get specific feedback on what weakness in the application led to the decision. Then address it before approaching the next lender. Credit unions carry more flexible lending criteria than large national banks and have a track record of approving files that the big five passed on.

Who Should Use This?

The CSBFP is a strong fit for you if:

- You are a Canadian service business owner with revenue under $10 million

- You need to finance equipment, software, leasehold improvements, or intangible assets

- You are a startup or early-stage business with limited collateral

- You want a lower interest rate than standard commercial loans offer

- You have a clear use of funds and can document it

Who Should Avoid This?

The CSBFP is not the right path if:

- You run a farming business (use the Canadian Agricultural Loans Act Program instead)

- You need fast, unsecured cash with minimal documentation (consider alternative lenders)

- Your credit or financial projections need significant work before a lender would approve you

- Your funding need is purely for operations without a specific asset or working capital component

Data & Findings

Program Scale (ISED, 2026)

Over the past decade, the CSBFP has backed more than 53,000 small businesses with over $11 billion in total financing. Startups and businesses under one year old account for approximately 74% of all program lending, which directly contradicts the common belief that federal loans are reserved for established companies with long credit histories.

Interest Rate Differential (April 2026)

CSBFP variable rate cap: 7.45% (prime 4.45% + 3%). Standard commercial loan rates without a government guarantee: typically 9% or higher, with a full personal guarantee required. On a $200,000 loan over ten years, the interest differential between a CSBFP-capped rate and a standard commercial rate produces an estimated $18,000 in savings, based on financing analyst reporting tracked against the program.

BDC Portfolio Composition (FY2025)

BDC deployed $11.5 billion in new financing in fiscal 2025 across 107,345 businesses. 68% of BDC’s portfolio serves businesses with under $2 million in annual sales, confirming that the program is genuinely accessible to smaller operators rather than being concentrated in mid-market companies. BDC interest rates in 2026 run between 11% and 13%, depending on borrower profile, compared to the CSBFP ceiling of 7.45%.

Unleash Your Power Client Observation

Across James R. Elliot’s 20+ years of working with Canadian entrepreneurs, the pattern is consistent: business owners who enter a financing process with a documented strategy, clear use of funds, and a defined growth plan are measurably more likely to secure approval on the first application. Those who approach lenders without that clarity frequently cycle through multiple rejections before either succeeding or abandoning the process. Preparation is the variable most within the owner’s control.

FAQs

What are the basic eligibility requirements for a federal small business loan in Canada (2026)?

To qualify for a federal small business loan in Canada under the Canada Small Business Financing Program (CSBFP) in 2026, your business must meet three core criteria:

Operate in Canada with a physical presence.

Generate under $10 million in annual gross revenue.

Be a for-profit business offering goods or services to the public.

Additionally, most lenders expect a personal credit score of around 680+, a clear use of funds, and proper business registration. Startups, including pre-revenue businesses, are eligible if they can demonstrate a viable business plan and repayment capacity.

Can service-based businesses qualify for CSBFP loans in Canada?

Yes, service-based businesses fully qualify for CSBFP loans in 2026. This includes consulting firms, digital agencies, coaches, and professional services.

The key requirement is that your business provides services to the public; physical products are not necessary. With the 2026 update, service businesses can now finance intangible assets such as software, CRM systems, websites, and digital tools, making the program more accessible than ever.

What is the maximum loan amount and interest rate under the CSBFP?

Under the CSBFP in 2026, businesses can access up to $1.15 million in total financing, including:

Up to $1 million for term loans (equipment, leaseholds, assets)

Up to $150,000 for a line of credit (working capital)

Interest rates are capped, with variable rates typically at prime + 3% (around 7.45% in 2026). This is significantly lower than many traditional or alternative lending options, making CSBFP one of the most cost-effective financing programs in Canada.

Why do businesses get rejected for CSBFP loans even if they qualify?

Even if a business meets eligibility criteria, loan applications can be rejected due to a weak financial presentation rather than a lack of qualification. The most common reasons include:

Poor or unrealistic cash flow projections

Debt Service Coverage Ratio below 1.2

Vague or unclear use of funds

Weak personal credit or unresolved financial issues

Lenders prioritize clarity and risk assessment. A well-documented application with clear funding purposes and realistic projections significantly improves approval chances.

What is the difference between CSBFP and BDC small business loans?

The main difference between CSBFP and BDC loans lies in structure, cost, and flexibility:

CSBFP offers lower interest rates (up to ~7.45%) and is ideal for asset-based financing, backed by an 85% government guarantee

BDC loans have higher rates (11–13%) but offer more flexibility, including unsecured loans with no collateral

CSBFP is best for businesses purchasing assets like equipment or software, while BDC is a strong alternative for businesses needing working capital or those declined by traditional lenders.

Conclusion: Funding Is Only Step One

The eligibility criteria for a federal small business loan in Canada are broader than most service business owners realize. The program exists specifically to lower the barrier for businesses that traditional lending overlooks. You just have to show up prepared.

One of the patterns James R. Elliot sees consistently after more than 20 years of working with Canadian entrepreneurs: what looks like a financing problem is often a strategy and clarity problem underneath. Darren G. came to James feeling stuck despite a good income, unable to move forward on building his own business. Once the goal blocks were cleared and the direction became concrete, the practical next steps, including financing, became obvious.

Funding does not fix an unclear business. It amplifies whatever is already there. If your strategy is solid, financing accelerates growth. If it is not, debt compounds the problem.

If you are ready to build the business infrastructure that makes lenders say yes, working with a business coach in Toronto gives you the strategic clarity that capital alone cannot provide. Pair that with a smart reinvestment strategy for the funds you secure, and you are not just borrowing money; you are building something that compounds.

Understanding why small businesses fail to grow usually comes before the breakthrough. The businesses that get funded and then use that funding well are the ones that started with the right entrepreneurial mindset. That is the work worth doing first.

Take the first step. Your transformation starts today.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.