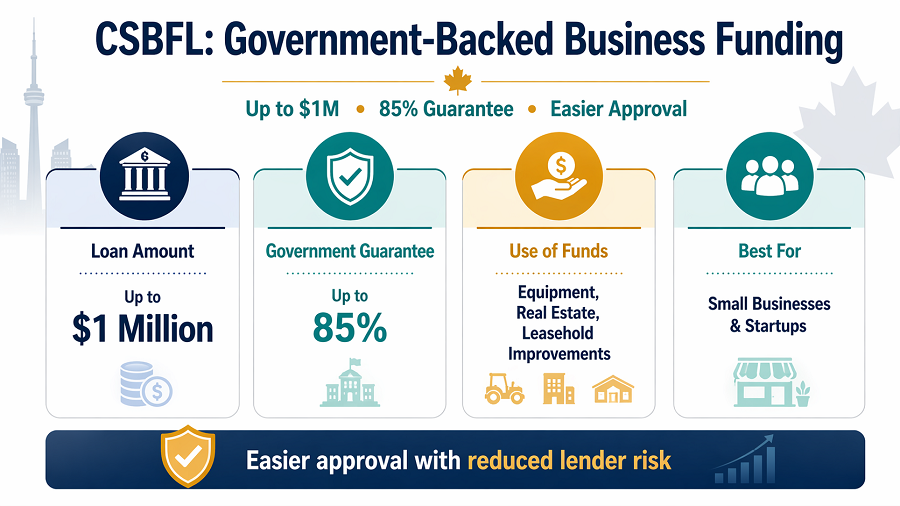

The Canada Small Business Financing Loan (CSBFL) is a government-backed program that helps Canadian businesses access funding with reduced lender risk. It allows businesses to borrow up to $1 million for equipment, real estate, and leasehold improvements, with the government guaranteeing up to 85% of the loan, making approval easier than traditional bank loans.

Most small businesses don’t fail because of bad ideas.

They fail because they run out of cash.

The Canada Small Business Financing Loan (CSBFL) exists to solve exactly that, but most entrepreneurs misunderstand how it works, what it covers, and whether it’s actually worth it.

Here’s everything you need to know.

But how does it work? What are the requirements? And how do you apply? This guide will walk you through everything you need to know from eligibility and loan terms to the application process and repayment options. Whether you’re launching a new venture or expanding an existing one, the CSBFL could be the funding solution your business needs.

Key Takeaway:

- The Canada Small Business Financing Loan (CSBFL) is a government-backed funding program that allows Canadian businesses to borrow up to $1 million, with up to 85% of the loan guaranteed by the government—making approval easier than traditional bank loans. [1]

- What it covers: CSBFL funds can be used for long-term investments such as equipment purchases, commercial real estate, and leasehold improvements—but not for working capital, inventory, or daily operational expenses. [1]

- Best use case: It’s ideal for small businesses and startups that need asset-based financing and may struggle to qualify for traditional loans due to limited collateral or credit history. [2]

- When to be cautious: CSBFL is not suitable for short-term cash flow needs or fast funding, as approval may take longer and funds are restricted to specific use cases. Businesses needing flexible financing should consider alternative options. [2]

Bottom Line: The CSBFL is one of the most accessible funding options in Canada for long-term business investments, thanks to government backing and easier approval—but it’s not designed for quick cash or operational expenses.

- Source: Government of Canada – Canada Small Business Financing Program

- Source: Unleash Your Power – CSBFL Guide

Is the Canada Small Business Financing Loan Worth It?

The CSBFL is worth it for small businesses that need funding for long-term assets like equipment or property but struggle to qualify for traditional loans. However, it is not ideal for businesses needing working capital, inventory funding, or short-term cash flow support.

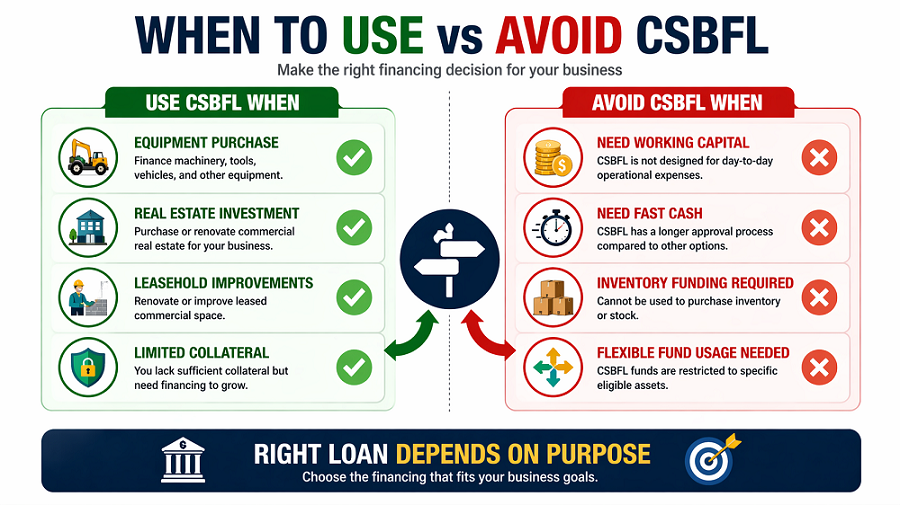

When Should You Use a CSBFL?

- You need equipment, real estate, or renovations

- You lack strong collateral

- You want easier loan approval

When Should You Avoid It?

- You need working capital or inventory funding

- You want fast access to cash

- Your business has unstable cash flow

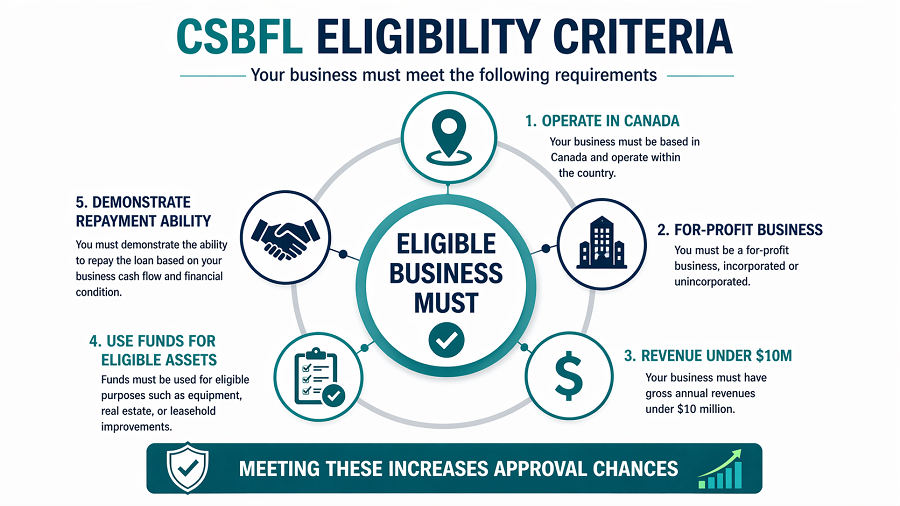

Eligibility Criteria

Business Eligibility

The CSBFL is available to small, for-profit businesses operating in Canada. To qualify, a business must meet the following criteria:

- It must be a for-profit business (corporations, partnerships, and sole proprietorships are eligible).

- It must have gross annual revenue of $10 million or less.

- The business must operate within Canada and be registered under Canadian laws.

Certain industries are not eligible for this loan. Farming businesses are excluded from the program since they have separate government loan programs available through organizations like the Canadian Agricultural Loans Act (CALA) program. Other ineligible businesses may include those engaged in charitable or non-profit activities.

Loan Purpose

The CSBFL is intended to help businesses acquire assets and improve their operations, not to cover everyday operating costs.

Eligible uses of the loan include:

- Purchasing equipment – Businesses can use the loan to buy machinery, tools, vehicles, and technology necessary for operations.

- Acquiring commercial real estate – This includes purchasing office space, warehouses, retail locations, or other business-related properties.

- Making leasehold improvements – This refers to renovations and upgrades made to rental properties, such as installing new flooring, upgrading lighting, or improving interior spaces.

However, certain expenses are not covered under the CSBFL. Businesses cannot use the loan for:

- Working capital (e.g., payroll, rent, utility bills).

- Inventory purchases (e.g., raw materials or stock for resale).

- Goodwill and franchise fees (e.g., fees for buying into a franchise or business acquisition costs).

Borrower Eligibility

To apply for the CSBFL, borrowers must meet certain criteria. Applicants must be Canadian citizens or permanent residents and must demonstrate creditworthiness and financial stability. While the loan is backed by the government, the lender makes the final decision on approval, meaning that businesses must still meet the bank or credit union’s lending requirements.

Lenders will review the applicant’s business plan, financial statements, and credit history to determine whether the loan is a suitable risk. Borrowers with a strong repayment history and clear business goals are more likely to be approved.

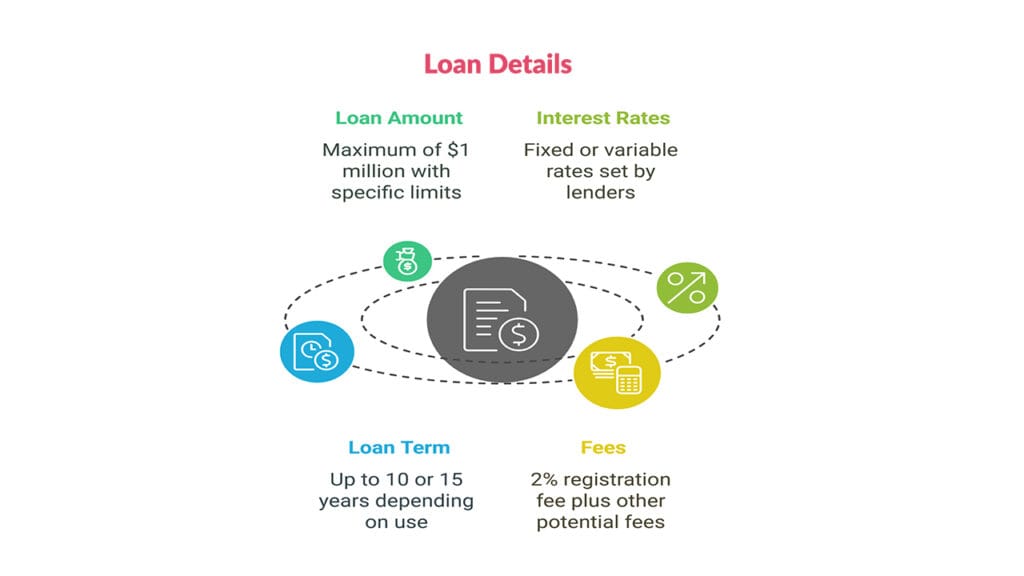

Loan Details

Loan Amount

The maximum loan amount available under the CSBFL is $1 million, but how the funds are used is subject to limits:

- Up to $500,000 can be used for equipment purchases and leasehold improvements.

- Up to $1 million can be used for commercial real estate purchases.

Interest Rates

Interest rates on CSBFL loans are set by the lender and can be either fixed or variable. A fixed interest rate remains the same throughout the loan term, while a variable interest rate is typically set at the lender’s prime rate plus up to 3%. Businesses should compare different lenders to find the most favorable rates.

Loan Term

The maximum repayment period for a CSBFL loan depends on how the funds are used:

- Up to 10 years for loans used to purchase equipment or make leasehold improvements.

- Up to 15 years for loans used to buy commercial real estate.

Fees

A 2% registration fee applies to all CSBFL loans. This fee is calculated based on the total loan amount and can be included in the loan financing. Other fees may also apply, including legal fees, appraisal fees, and administrative costs charged by the lender.

Application Process

Applying for the Canada Small Business Financing Loan (CSBFL) is a straightforward process, but proper preparation is key to increasing your chances of approval. Here’s a simple breakdown of how to apply:

Step 1: Prepare Your Documents

Before applying, gather all the necessary documents to show the lender that your business is financially stable and capable of repaying the loan. You’ll need:

- A Business Plan: Clearly explain your business goals, how the loan will be used, and how it will help your business grow.

- Financial Statements: Include cash flow projections, income statements, and balance sheets to demonstrate financial health.

- Credit History: Both the business and the owner’s credit history will be reviewed. If your business is new, your personal credit score will be important.

- Legal Documents: Some lenders may ask for additional paperwork, such as business registration certificates or lease agreements.

Being well-prepared will help speed up the process and improve your chances of getting approved.

Step 2: Choose a Lender

The CSBFL is offered by various banks, credit unions, and financial institutions, including RBC, TD, BMO, Scotiabank, and CIBC. Since loan terms can vary, it’s a good idea to compare lenders to find the best interest rates, repayment terms, and additional fees.

When meeting with potential lenders, ask about:

- Interest rates (fixed vs. variable).

- Repayment schedules and flexibility.

- Any extra fees (e.g., legal or administrative costs).

Choosing the right lender can make a big difference in how affordable and manageable your loan is over time.

Step 3: Submit Your Application

Once you’ve chosen a lender, you’ll need to submit a formal application along with all required documents. The lender will review your application by:

- Checking your credit score and financial history.

- Evaluating your business plan and repayment ability.

- Confirming that the loan will be used for an eligible purpose (e.g., equipment, real estate, renovations).

Lenders may ask for additional details or clarification, so be ready to provide any extra information they need. The review process can take anywhere from a few days to a few weeks.

Step 4: Loan Approval and Funds Disbursement

If approved, the lender will provide a loan agreement outlining the repayment terms, interest rates, and any fees. Carefully read and understand the agreement before signing.

Once everything is finalized, the loan funds will be disbursed based on the approved purpose, such as paying for equipment, renovations, or commercial property purchases. The lender may require proof that the funds were used correctly, so keep records of all transactions.

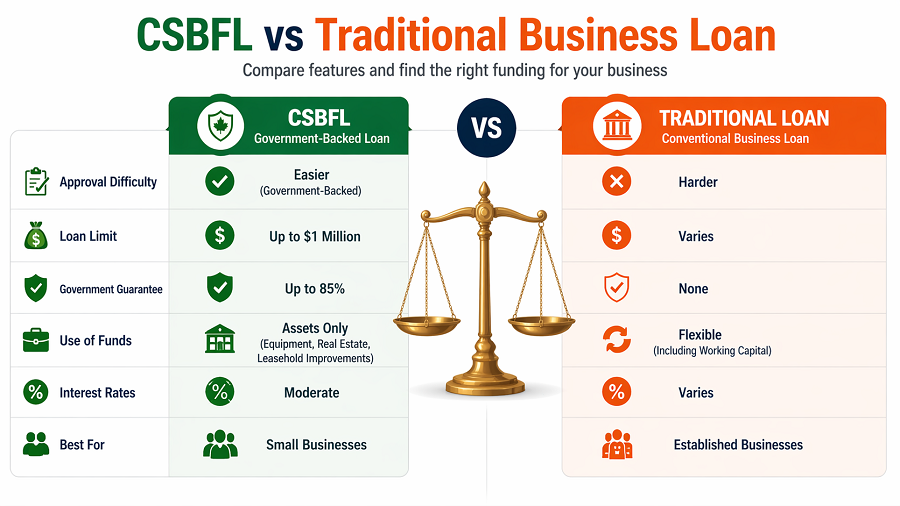

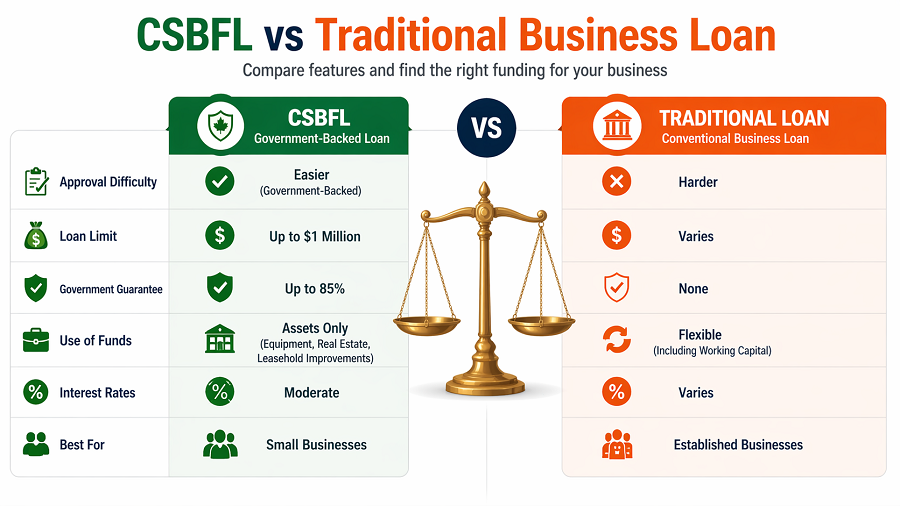

CSBFL vs Traditional Business Loans

| Feature | CSBFL | Traditional Loan |

|---|---|---|

| Approval difficulty | Easier (government-backed) | Harder |

| Maximum loan | Up to $1M | Varies |

| Government guarantee | 85% | None |

| Usage | Assets only | Flexible |

| Interest rates | Moderate | Varies |

| Best for | Small businesses | Established businesses |

Government Guarantee for the Canada Small Business Financing Loan

One of the biggest benefits of the CSBFL is that the Government of Canada guarantees 85% of the loan, reducing the risk for lenders and making it easier for small businesses to secure financing. This guarantee encourages banks and credit unions to approve loans for businesses that may not meet traditional lending criteria.

Risk Sharing: How It Works

With the government covering 85% of the loan balance in case of default, lenders are more willing to provide financing to small businesses. For example, if a business defaults on a $100,000 loan, the government repays $85,000, while the lender covers the remaining 15%. This reduces financial risk for banks, making funding more accessible for entrepreneurs.

Borrower Responsibility

Even though the loan is government-backed, borrowers are fully responsible for repayment. If a business fails to make payments, the lender can take legal action, seize business assets, and report the default to credit agencies, which can hurt the borrower’s credit score.

Repayment Terms for the Canada Small Business Financing Loan

Understanding the repayment terms of the CSBFL is crucial for managing finances effectively. The loan offers a flexible repayment schedule, prepayment options, and consequences for default, helping businesses plan for long-term financial success.

Repayment Schedule

Businesses must make monthly or quarterly payments based on their loan agreement. The repayment period depends on the loan’s purpose:

- Up to 10 years for equipment purchases and leasehold improvements.

- Up to 15 years for commercial real estate purchases.

A structured repayment plan helps businesses manage cash flow while repaying their loan.

Prepayment Options

Some lenders allow businesses to pay off the loan early without penalties, reducing overall interest costs. However, not all lenders offer this flexibility, some charge prepayment fees. Business owners should review their lender’s prepayment policy before signing the loan agreement.

Default and Consequences

Failing to repay the loan can have serious financial consequences, including:

- Damage to credit score, making future borrowing difficult.

- Legal action from the lender to recover funds.

- Seizure of business assets used as collateral.

Although the government guarantees 85% of the loan, this protects the lender, not the borrower. Business owners remain fully responsible for repayment, making financial planning essential to avoid default.

Benefits of the CSBFL

Easier Access to Funding

Many small businesses struggle to get loans due to limited credit history or collateral. The CSBFL reduces risk for lenders by guaranteeing 85% of the loan, making it easier for businesses to get approved and access the funds they need to grow.

Flexible Repayment Terms

With repayment terms of up to 10 years for equipment and 15 years for real estate, the CSBFL offers longer repayment periods than many traditional loans. This helps businesses manage cash flow while investing in long-term growth. Some lenders also allow early repayment without penalties, reducing overall interest costs.

Government Support for Small Businesses

By backing loans, the government encourages banks and credit unions to lend to small businesses, boosting economic growth and job creation. This program is especially helpful for startups and newer businesses that might not qualify for regular bank loans.

How to Qualify for a Canada Small Business Loan

To qualify for a CSBFL loan, your business must operate in Canada, have gross annual revenues under $10 million, and use the funds for eligible purposes such as equipment, leasehold improvements, or commercial real estate.

CSBFL Interest Rates Explained

CSBFL interest rates are typically set by lenders and can be fixed or variable, often slightly higher than standard loans due to government-backed security and reduced lender risk.

Can Startups Get a CSBFL Loan?

Yes, startups can qualify for CSBFL loans if they meet eligibility criteria and demonstrate a viable business plan, although approval depends on lender assessment and financial projections.

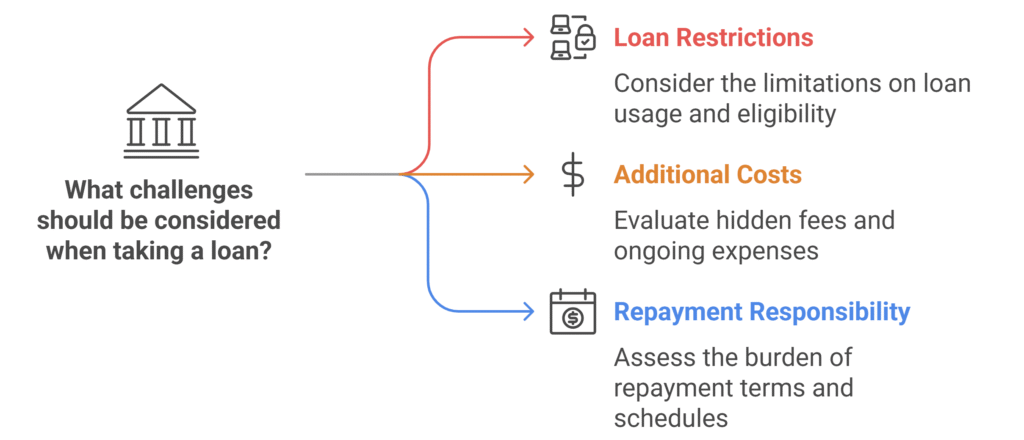

Challenges to Consider

Loan Restrictions

The CSBFL cannot be used for working capital, meaning funds can’t cover payroll, rent, or inventory. Businesses needing cash flow support may need to explore other financing options.

Additional Costs

Borrowers must pay a 2% registration fee on the loan amount, and some lenders charge extra fees for legal or administrative services. These costs should be factored into financial planning.

Repayment Responsibility

Although the government guarantees 85% of the loan, borrowers are still fully responsible for repayment. If payments are missed, lenders can take legal action, seize business assets, and report defaults to credit agencies, which can hurt the business owner’s credit score.

Frequently Asked Questions About Canada Small Business Financing Loans

What are the benefits of getting a Canada small business financing loan?

A Canada Small Business Financing Loan helps entrepreneurs access affordable funding with lower interest rates, government-backed security, and easier approval compared to traditional loans. It can be used for equipment, renovations, or property, making it a strong option for growing businesses.

What can a Canada Small Business Financing Loan be used for?

These loans can cover costs like buying or improving commercial property, purchasing new or used equipment, and financing renovations. However, they cannot be used for working capital, franchise fees, or paying off existing debts. This makes them ideal for long-term investments.

How much does a Canada Small Business Financing Loan cost?

Costs include the interest rate set by the lender, a one-time 2% registration fee, and potential administrative charges. Since the program is partly guaranteed by the government, interest rates are often more competitive than standard small business loans.

Is a Canada Small Business Financing Loan safe for startups?

Yes, it’s generally safe because the program is government-backed, giving lenders more security. However, startups must still demonstrate repayment ability. Borrowers are personally responsible for repayment, so carefully assess cash flow before applying.

Is the CSBFL loan safe?

Yes, the Canada Small Business Financing Loan is considered safe because it is backed by the Government of Canada, which guarantees up to 85% of the loan. However, borrowers remain fully responsible for repayment, and defaulting can negatively impact credit and lead to legal consequences.

Can I use CSBFL for working capital?

No, CSBFL funds cannot be used for working capital, inventory, or day-to-day operational expenses. The program is specifically designed for long-term investments such as equipment, leasehold improvements, and commercial property.

How much can I borrow?

You can borrow up to $1 million under the CSBFL program, with limits depending on the purpose of the loan. A portion of this can be allocated specifically for equipment and leasehold improvements.

Conclusion

The Canada Small Business Financing Loan (CSBFL) is a great option for entrepreneurs looking to invest in equipment, commercial real estate, or business improvements. With government backing, flexible repayment terms, and easier loan approval, it provides much-needed support to small businesses.

Before applying, business owners should carefully review their financial situation, research lenders, and prepare a strong business plan. With the right planning, the CSBFL can be a powerful tool to help businesses grow and thrive in Canada’s competitive marketplace.

The Canada Small Business Financing Loan is one of the most accessible funding options for Canadian entrepreneurs who need capital for long-term investments. With government backing and reduced lender risk, it improves approval chances, but it’s not suitable for short-term funding needs or operational cash flow.