The best business banking in Canada depends on your needs: Big Banks offer stability, in-person support, and full-service solutions, while digital challengers provide lower fees, faster setup, and modern tools. For most small businesses and startups in 2026, digital banks are often more cost-effective, while established businesses may benefit more from traditional Big Bank services.

Canada’s best business bank accounts in 2026 split into two clear camps. The Big Five banks (RBC, TD, BMO, Scotiabank, and CIBC) charge between $30 and $125 or more per month but give you branch access, established lending relationships, and the credibility that loan officers recognize. Digital challengers like EQ Bank, Float, and Venn charge zero monthly fees and pay 2 to 4% interest on your operating balance.

Key Takeaway:

- The best business banking option in Canada depends on your transaction volume, monthly fee tolerance, cash deposit needs, and whether your business operates primarily online or in person.

- Digital-first accounts are often best for freelancers, consultants, SaaS founders, and service businesses because they offer lower fees, strong online banking, and easy e-transfer management.

- Traditional banks remain a strong choice for established businesses that need branch access, cash handling, business credit, lending products, and relationship-based banking support.

- The most important factors to compare are monthly fees, transaction limits, international payment support, mobile banking quality, and access to business credit tools.

- Choosing the right account can directly improve cash flow efficiency, reduce hidden fees, and support long-term business growth in Canada.

Bottom Line: The best business bank account in Canada is the one that aligns with how your business moves money low-cost digital banking for lean operations or full-service traditional banking for scale, lending, and cash-heavy workflows.

For most Canadian entrepreneurs in 2026, the strongest setup is not one or the other. It is a deliberate combination: a digital account for daily operations and yield, paired with a Big Five relationship for future credit access. Canada’s open banking framework rollout, beginning in 2026, makes this hybrid approach more secure and more practical than ever before.

What Is the Best Business Bank in Canada for Entrepreneurs in 2026?

The honest answer is that there is no single best business bank account for every Canadian entrepreneur. The right choice depends on how your business moves money, whether you need physical branches, and whether you are planning to apply for financing within the next one to three years.

What has changed significantly in 2026 is that digital-first platforms have matured. They are no longer just payment apps or savings workarounds. EQ Bank, Float, and Venn now offer genuine business banking functionality, including CDIC insurance protection, corporate cards, and accounting software integrations. Canadian entrepreneurs finally have real alternatives to the Big Five.

The most important thing to understand before comparing your options: your banking choice affects your loan eligibility, your tax organization, and how efficiently your cash works for you on a daily basis. It is a growth decision, not just an admin task. For a deeper look at options early in your business journey, see our guide to bank accounts for Canadian startups.

The Big Five: What You Get and What It Costs

Canada’s Big Six banks (RBC, TD, BMO, Scotiabank, CIBC, and National Bank) collectively hold more than 90% of commercial banking assets in the country. Their business accounts come with real advantages: branch access for cash deposits, dedicated relationship managers, and established lending pipelines that digital platforms cannot replicate yet.

But the cost structure is steep. Entry-level Big Five business plans typically start around $30 per month. Unlimited transaction accounts range from $65 to $125 per month. Most banks will waive those fees if you hold a minimum balance, but the thresholds are significant. TD’s Unlimited Business Plan requires a $65,000 balance to waive its $125 monthly fee. Keeping that much in a non-interest-bearing checking account represents a real cost, not a savings.

Here is what that actually means: $65,000 sitting idle in a Big Five account earns close to nothing. At a digital platform paying 4% annually, that same balance generates roughly $2,600 per year. That is money leaving your business quietly, every year, without a single transaction fee attached to it. This is what we call the Zombie Balance problem. The capital is technically yours. It just is not working.

Onboarding with a Big Five bank typically takes three to five business days, with branch visits and paperwork required for most business account applications.

Digital Challengers: EQ Bank, Float, Venn and the No-Fee Revolution

The biggest shift in Canadian business banking in 2026 is the maturation of digital platforms into full-featured alternatives. These are the standout options:

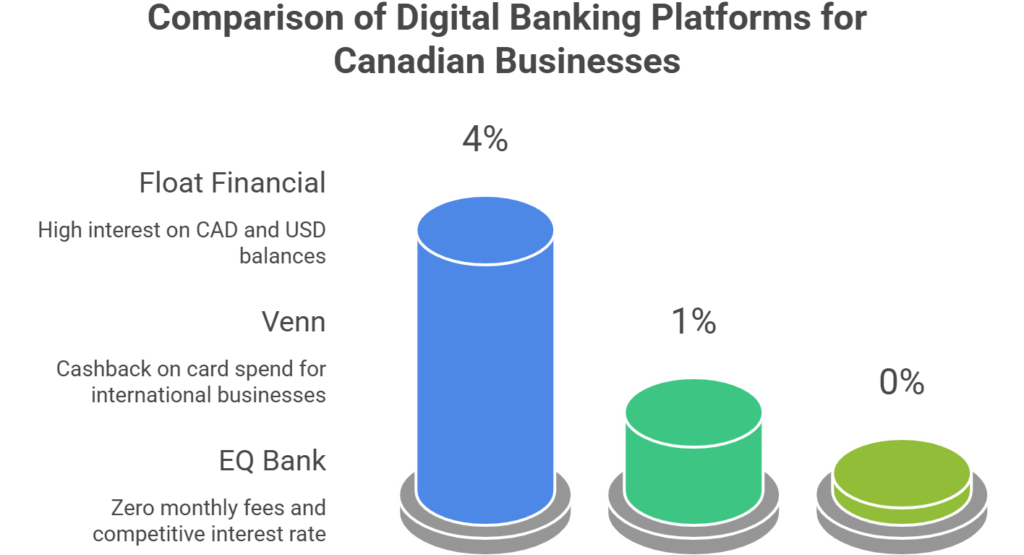

EQ Bank

EQ Bank won Ratehub’s best chequing account award for 2026. The business account charges zero monthly fees, pays a competitive interest rate on everyday balances, and includes unlimited electronic transfers and mobile cheque deposits. EQ Bank is a Schedule I bank, meaning deposits are CDIC-insured directly. The only real limitation: there are no branches. For consultants, coaches, SaaS operators, and professional services firms, that is rarely a problem.

Float Financial

Float targets Canadian businesses with higher operating balances. Float pays up to 4% annualized interest on both CAD and USD balances, charges zero monthly fees, and includes corporate cards with spend controls. A Toronto marketing agency holding $80,000 in working capital between projects earns a meaningful yield with Float rather than watching that balance sit idle at a Big Five account earning nothing.

Venn

Venn stands out for businesses with international operations. It offers local CAD and USD accounts, support for over 30 currencies, 1% cashback on card spend, and accounting integrations with QuickBooks and Xero. Foreign exchange markups at traditional banks typically run between 2.5% and 4% per transaction. Venn’s rates are significantly lower, which adds up fast for businesses paying international suppliers or receiving payments in USD.

Account opening with any of these platforms takes under 15 minutes online. No branch visits required.

For a broader comparison of small business account options, our guide to the best bank accounts for small businesses covers the full landscape.

The Hidden Costs Canadian Entrepreneurs Miss

Banking fees you can see are only part of the picture. The costs that quietly drain Canadian business owners tend to be invisible until someone points them out.

Idle Cash Loss:

As described above, holding large balances in non-interest-bearing Big Five accounts is an opportunity cost with a real dollar value. If your operating balance averages $50,000 and your bank pays 0% while digital platforms pay 3 to 4%, you are giving up $1,500 to $2,000 per year for the convenience of keeping money somewhere familiar.

FX Markups:

Big Five banks typically add a 2.5% to 4% markup on every foreign exchange transaction, often without displaying it transparently. For a business paying $200,000 in USD vendor invoices annually, that markup costs between $5,000 and $8,000 per year on top of the stated rate.

NSF Fees:

New federal regulations that took effect in March 2026 cap non-sufficient funds fees at $10, down from the previous $45 to $48 charged by most major banks. This is a meaningful change for small businesses managing tight cash flow timing.

Understanding where money is leaking is part of Building Smart reinvestment strategies that actually compound your growth over time.

The Biggest Business Banking Mistakes in Canada

Most of these are decisions made by default rather than design, and they cost more than most entrepreneurs realize.

- Using one account for everything: Mixing operating cash, savings, and personal funds in a single account creates tax headaches and makes it nearly impossible to see how your business is actually performing month to month.

- Chasing fee waivers instead of yield: Locking up $65,000 to avoid a $125 monthly fee sounds smart until you calculate what that capital could earn elsewhere. The math rarely works out in the bank’s favor.

- Ignoring FX fees: International payment costs are invisible in most bank statements because the markup is embedded in the exchange rate. Most business owners never compare the stated rate to the mid-market rate, and that gap adds up to thousands annually.

- Not building a lending relationship early: Digital banks are excellent for operations and yield. They are not yet strong enough for business credit. If you wait until you need a loan to open a Big Five account, you are starting from zero with no transaction history. Build that relationship before you need it.

- Skipping a dedicated business account entirely: Using a personal checking account for business transactions is surprisingly common among freelancers and early-stage founders. It creates immediate problems when applying for any form of business financing, where lenders expect to see a distinct business banking history.

These gaps are not just financial friction. After 20+ years working with entrepreneurs, what I have seen consistently is this: the decisions that hold businesses back are rarely the obvious ones. They are the quiet patterns running in the background, costing money and credibility every single month.

Best Business Bank in Canada for Entrepreneurs Seeking Loans

If you plan to apply for a Canada Small Business Financing Program (CSBFP) loan or a conventional business line of credit, your banking relationship matters more than most founders expect.

Lenders assess your creditworthiness in part through your banking history: transaction consistency, average balances, and the depth of your existing relationship with a financial institution. A business that has banked with RBC or TD for two years before applying carries a meaningfully different profile than one opening a new account at loan application time.

The practical recommendation: maintain a Big Five account even if you do most of your day-to-day banking digitally. You do not need to keep large balances there. You need a consistent, organized transaction history that gives a lender something to evaluate when the time comes.

For a deeper look at how business structure and financial decisions affect growth, our post on why small businesses fail to grow addresses the patterns worth catching early.

What Canada’s 2026 Open Banking Framework Changes for Small Businesses

Canada’s consumer-driven banking framework, launched in 2026 under Financial Consumer Agency of Canada oversight, represents the first structural reform to Canadian banking in decades. In practical terms for small business owners, it means three things.

First, you can now direct your bank to share your financial data with accredited third-party platforms through secure API connections, without sharing your login credentials. Password sharing has been the standard workaround for years. The new framework replaces it with direct, regulated data connections.

Second, real-time dashboards that pull information across multiple institutions become genuinely viable. If you run the 3-account stack described below, you can view your operating account, yield account, and lending account in a single interface without logging into three separate banking portals.

Third, switching costs fall. When your data is portable, moving providers become faster and less painful. That increases competitive pressure on the Big Five to improve their products and pricing.

This is the first time in Canada that a modular, multi-institution banking setup can be both practical and secure. The open banking framework is what makes the hybrid model genuinely frictionless in 2026.

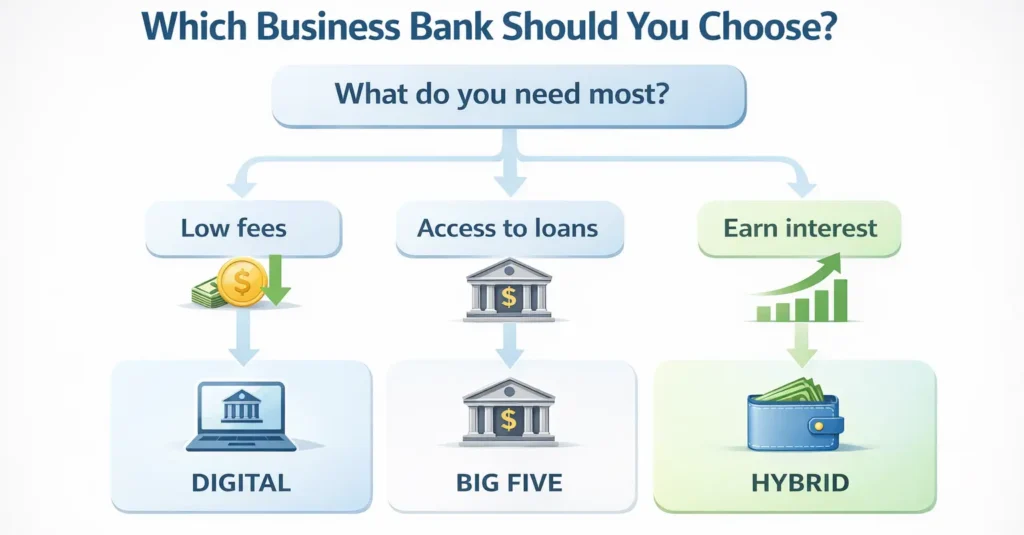

Who Should Stick with a Big Five Bank?

A Big Five bank is the right primary account for your business if:

- You handle significant volumes of physical cash that require regular branch deposits.

- You are planning to apply for a business loan, line of credit, or commercial mortgage within one to three years.

- Your business requires complex banking services like letters of credit, trade finance, or payroll processing for a larger team.

- You have existing personal banking, mortgages, or credit facilities with a Big Five institution and want consolidated relationship management.

Who Should Go Digital-First?

A digital-first account is a strong fit if:

- Your business operates primarily online with electronic payments and invoicing.

- You want to earn yield on operating cash without maintaining a separate savings account. You transact frequently in foreign currencies and want to avoid hidden FX markups.

- You are in the early stages of your business and want to keep monthly overhead low.

- You are a consultant, coach, freelancer, or professional services operator with no need for cash deposit services.

For most Canadian entrepreneurs, both apply to some degree. The clearest path in 2026 is a deliberate hybrid.

Big Five vs. Digital Challengers: Side-by-Side Comparison

| Feature | Big Five Banks | EQ Bank | Float | Venn |

|---|---|---|---|---|

| Monthly fee | $30 to $125+ | $0 | $0 | $0 |

| Interest on deposits | 0% (operating) | 2.75% | Up to 4% | 2%+ |

| CDIC insurance | Yes | Yes (direct) | Yes (partner) | Yes (partner) |

| Branch access | Yes | No | No | No |

| Onboarding time | 3 to 5 days | <15 min | <15 min | <15 min |

| Lending access | Strong | Limited | Limited | Limited |

| FX markups | 2.5 to 4% | N/A | Low | Low |

| Accounting integrations | Basic | Basic | Strong | Strong |

| Best for | Lending, cash | Simplicity | Yield/spend | Cross-border |

Data & Findings

Canada’s business banking landscape is rapidly evolving, driven by rising fees, regulatory changes, and the growth of digital challengers.

Canadian banks have increasingly relied on fee-based income, with nearly 48% of revenue coming from non-interest sources. This highlights how traditional banks depend heavily on service charges rather than core banking services. Source:

Regulators are now stepping in to reduce costs. The Financial Consumer Agency of Canada (FCAC) announced new rules capping NSF (non-sufficient funds) fees at $10 starting in 2026, alongside commitments for low-cost accounts. This aims to improve affordability and transparency:

Digital challengers are gaining traction by solving these issues. For example, Float offers up to 4% yield on business balances, compared to near 0% interest from traditional Big Five banks, making them more attractive for cash-heavy businesses:

Market rankings are also shifting. EQ Bank has been ranked among the top chequing account providers, while traditional banks like TD have been absent from the top 2026 rankings, signaling a change in value perception:

Structurally, the Canadian banking system remains highly concentrated, with the Big Six controlling over 90% of commercial banking assets. This dominance has historically limited competition and contributed to higher fees:

Looking ahead, the introduction of open banking frameworks in 2026 is expected to accelerate competition. This will allow businesses to securely share financial data with fintech providers, enabling more personalized and lower-cost solutions

The 3-Step Business Banking Stack

This framework gives every account a single job. When accounts are mixed or undefined, you lose clarity and you lose money.

Step 1: Operating Account (Digital)

This is where your daily cash flow lives. Payments come in, bills go out, and payroll processes. A digital platform like EQ Bank or Float works well here because there are no transaction fees eating into routine activity and the interface is faster than most Big Five portals.

Step 2: Yield Account (Digital)

Any cash that sits for more than a week goes here. Float pays up to 4% annually on balances you can still access immediately. This is not a locked GIC or a complex investment. It is your working capital, earning a return while it waits. A Toronto agency holding $80,000 in operating reserves earns approximately $3,200 per year with this setup rather than nothing.

Step 3: Lending Account (Big Five)

This account is for relationship-building, not daily use. Keep it active with consistent, organized transactions. Run payroll or a supplier payment through it monthly. When you are ready to apply for a business loan or line of credit, you have two to three years of clean banking history to present.

Each account has one job. When you mix them, you lose money.

Darren G. came to James feeling financially stuck despite a well-paying career, blocked from the income growth and business he had always wanted. The shift that started to unblock him was not dramatic. It was a series of clear, deliberate decisions about structure: where to direct his resources, and what each piece of his financial life was supposed to do. Applying that same clarity to your banking setup produces the same result. Structure does not limit growth. It enables it.

If your current banking setup is not built this way, it is not just inefficient. It is quietly limiting what you can build.

For a broader look at the mindset that supports deliberate financial decision-making, explore the entrepreneurial mindset through NLP.

Frequently Asked Questions

What is the best business bank account in Canada in 2026?

The best option depends on your business model. EQ Bank is the top choice for simplicity and no fees. Float Financial is strongest for earning yield on operating balances. Venn is best for businesses with international payment needs. For lending access and branch support, the Big Five remain the most practical option. Most Canadian entrepreneurs benefit from combining a digital account for daily operations with a Big Five account for building a lending relationship.

Are digital business bank accounts in Canada CDIC-insured?

Yes, most are. EQ Bank is a Schedule I bank with direct CDIC coverage. Float and Venn hold business funds in trust accounts at CDIC-member institutions, which typically qualify those deposits for coverage up to $100,000 per depositor. Always confirm the specific coverage structure directly with each provider before opening an account.

Do I need a Big Five bank account to get a business loan in Canada?

Not strictly required, but practically important. Lenders assess your transaction history and banking relationship as part of any business credit evaluation. Having an active, organized Big Five account for one to two years before applying gives your application a significantly stronger footing. If you plan to seek financing within three years, open a Big Five account now and keep it active with regular, organized transactions.

What is Canada’s 2026 open banking framework?

Canada’s consumer-driven banking framework, launched in 2026 under Financial Consumer Agency of Canada oversight, allows business owners to direct their bank to share financial data with accredited third-party platforms through secure API connections. This replaces the practice of sharing banking passwords with apps and enables real-time data access across multiple accounts and institutions, making hybrid banking setups more secure and more practical than ever before.

How much can a Canadian business save by switching to a digital bank account?

It depends on your current setup. A business paying $125 per month in Big Five fees saves $1,500 per year in direct fees by switching to a zero-fee digital account. If you also move idle operating cash to a platform paying 4% annually, a $50,000 average balance adds another $2,000 per year in recovered yield. For businesses with international payments, reducing FX markups from 3.5% to under 1% on $200,000 in annual transactions saves an additional $5,000 or more per year.

Your Banking Setup Is a Growth Decision

Your banking structure is one of those foundational decisions most entrepreneurs make once and never revisit. In 2026, the gap between what the Big Five offer and what digital challengers deliver has become too large to ignore. The smart move is not to pick a side. It is to build a deliberate stack where every account has a clear role, and your money is working as hard as you are.

Clarity of vision extends to your finances. If you want to build a business that gives you genuine freedom, every part of your operating structure needs to reflect that intention, including where you bank.

Ready to take decisive action on the decisions that drive real growth? Explore James R. Elliot’s business coaching programs atunleashyourpower.com/business-coach-toronto and start building the financial and mindset foundation your business deserves.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.