Life coaches in Canada are not legally required to carry insurance. Coaching remains an unregulated profession, with no government license, college, or governing body overseeing who can call themselves a coach. That said, professional liability insurance, also called errors and omissions insurance, is strongly recommended and often expected by corporate clients, event venues, and professional associations.

Coverage for Canadian coaches typically starts around $300 to $400 a year for $500,000 in protection, with most established practices paying between $500 and $1,000 annually once general liability and other add-ons are included. Insurance protects you if a client alleges negligence, financial loss, or breach of professional duty.

It does not replace a signed coaching agreement, proper business registration, or staying inside your scope of practice. Most coaches buy coverage once they take on a first paying client, since that’s when real liability exposure begins.

Key Takeaway:

- Life coach insurance helps protect Canadian coaches from financial losses related to client claims, accidents, property damage, and legal disputes. While not legally required in every province, having appropriate coverage demonstrates professionalism and reduces business risk. [1]

- Most coaching businesses benefit from a combination of professional liability (errors and omissions), general liability, cyber liability, and business property insurance. The right coverage depends on whether you coach online, in person, or operate a physical office. [1]

- When comparing insurance providers, review coverage limits, policy exclusions, deductibles, legal defense costs, and whether your coaching niche or certifications require specialized protection. Choosing a policy based solely on price can leave important risks uncovered. [2]

- As your coaching practice grows, review your insurance annually to ensure it reflects new services, additional staff, digital tools, or increased revenue. Keeping your coverage up to date helps safeguard both your business and your professional reputation. [2]

Bottom Line: Life coach insurance is an essential investment for Canadian coaches who want to protect their business, clients, and reputation. Selecting comprehensive coverage that matches your coaching practice provides peace of mind and allows you to focus on delivering exceptional client results.

You’re Building a Business. Insurance Is Part of the Foundation.

You’ve decided to become a life coach. You’re setting things up properly: a niche, a website, maybe a few discovery calls already booked. Then someone mentions insurance, and suddenly you’re not sure if it’s a legal requirement, a nice-to-have, or something you can put off until you’re “more established.”

Here’s the honest answer. Life coaching is unregulated in Canada, so no law forces you to carry insurance. But that doesn’t mean it’s optional in any practical sense. In my 20-plus years of training coaches across Canada, the ones who treat their practice like a real business from day one, contracts, structure, and protection included, are the ones who last. This article walks through exactly where you stand legally, what coverage actually does, what it costs, and how to put the right protection in place before you sign your first client. If you’re building toward a credentialed practice, our Life Coach Training Certification in Canada program covers the business foundations alongside the coaching skills.

Quick Legal Checklist

Before diving into the details, here’s where insurance fits into the broader legal picture for new coaches.

| Item | Required by Law? | Recommended? |

| Professional Liability Insurance | No | Yes |

| General Liability Insurance | No | Often |

| Coaching Agreement | No | Yes |

| Business Registration | Depends on the business name | Usually |

| GST/HST Registration | Mandatory after $30,000 CAD revenue | Yes |

| Cyber Liability Coverage | No | Increasingly |

Insurance is one line on this checklist, not the whole list. A complete legal foundation pairs coverage with a signed agreement, proper registration, and clean record-keeping.

Are Life Coaches Regulated in Canada?

Understanding Coaching’s Legal Status

Coaching is generally unregulated across every Canadian province and territory. There’s no federal coaching license, no mandatory certification, and no government body that approves or disqualifies who can call themselves a life coach. Business registration requirements do vary by province, but those rules govern your business name and tax obligations, not your right to practice coaching itself.

Coaching vs. Therapy: Where Legal Risk Appears

The legal risk for coaches doesn’t usually come from coaching itself. It comes from drifting into territory reserved for regulated health professionals.

In Ontario, for example, the Regulated Health Professions Act defines psychotherapy as a “controlled act,” restricted to members of six regulated colleges, including the College of Registered Psychotherapists of Ontario. The controlled act specifically covers treating a serious disorder of thought, mood, emotional regulation, perception, or memory through a therapeutic relationship. General counselling, advice-giving, and goal-focused coaching fall outside that definition, but the line can blur fast if a coach starts diagnosing or treating mental health conditions.

The practical rule is simple. Don’t diagnose. Don’t advertise psychotherapy services unless you’re licensed to provide them. Staying inside your coaching scope reduces both your legal exposure and your insurance risk, since most policies exclude claims tied to unlicensed clinical work. For the full picture of what’s required province by province, see our complete legal requirements for coaching in Canada guide.

Can You Get Life Coach Insurance Without Certification?

Yes, in most cases. Insurers evaluate the services you actually offer, not whether you hold a specific credential. Certification isn’t a prerequisite for buying a policy.

That said, training still matters for reasons beyond insurance eligibility. It builds the credibility that helps you land corporate contracts, and many professional associations set their own education standards for membership. If you’re still weighing your training options, our Life Coach Training Certification in Canada program is built to give you both the coaching skills and the business grounding clients expect from a professional practice.

What Types of Insurance Do Life Coaches Actually Need?

Professional Liability Insurance (Errors & Omissions)

This is the core policy for any coach with paying clients. It covers claims that your advice caused harm or financial loss, allegations of professional negligence, and the legal defence costs that come with fighting even a baseless claim. Zensurance notes that professional liability coverage for life coaches typically starts around $315 a year for $500,000 in protection, which makes it one of the more affordable lines of business insurance available.

Who needs it: Every coach working with paying clients, regardless of niche or delivery format.

General Liability Insurance

Also called commercial general liability (CGL), this covers third-party bodily injury, property damage, and claims like false advertising or libel. Think of a client tripping in your office, or a chair breaking during a session. Hiscox recommends pairing professional liability with general liability for coaches who regularly meet clients face to face.

Who needs it: Coaches who see clients in person, rent office space, or run in-person workshops.

Cyber Liability Insurance

If you store client intake forms, session notes, or payment details digitally, a data breach or ransomware incident can expose you to real liability. Rates.ca lists cyber liability as one of the more common add-ons Canadian coaches are purchasing as coaching moves further online.

Who needs it: Online coaches and anyone storing client data in a CRM, scheduling tool, or cloud storage.

| Coverage Type | Protects Against | Best For | Typical Annual Cost |

| Professional Liability (E&O) | Negligence claims, bad-advice allegations, and financial-loss disputes | All coaches with paying clients | From about $315 |

| General Liability (CGL) | Slip-and-fall injuries, property damage, and false advertising | In-person coaches, workshop hosts | From about $250 |

| Cyber Liability | Data breaches, stolen client records, ransomware | Online coaches storing client data | Often $100 to $300 as an add-on |

How Much Does Life Coach Insurance Cost in Canada?

Typical Premium Ranges

Entry-level professional liability coverage starts in the low hundreds of dollars annually. Mid-range packages that bundle professional and general liability typically land between $500 and $1,000 a year, according to Rates.ca. Expanded packages with cyber liability, business interruption, and higher coverage limits push toward the upper end of that range or beyond, depending on your revenue and risk profile.

What Affects Your Premium

Several factors shape your quote: your annual revenue, the coverage limit you choose, your claims history, your province, how many clients you work with, and whether you serve clients outside Canada. Coaches offering health-adjacent or financial-adjacent services typically see higher premiums than general life or career coaches.

Typical Deductibles

Acera’s EasyCover program notes that deductibles for life coach policies usually fall between $250 and $1,500 per claim, often scaled to your annual revenue. Two claims in the same policy year means paying that deductible twice, so it’s worth factoring into your budget alongside the premium itself.

Data and Findings

Here’s a consolidated snapshot of the numbers that matter most when you’re budgeting for coverage, pulled directly from the sources cited throughout this guide.

| Metric | Figure | Source |

| Entry-level professional liability premium | From $315/year for $500,000 coverage | Zensurance |

| Entry-level general liability premium | From $250/year for $1,000,000 coverage | Zensurance |

| Typical bundled coverage most coaches carry | $500 to $1,000/year | Rates.ca |

| Typical per-claim deductible | $250 to $1,500 | Acera EasyCover |

| GST/HST registration threshold | Mandatory above $30,000 CAD annual revenue | Legal Requirements for Coaching in Canada |

| ICF membership cost and eligibility | $270 USD/year, requires 60 hours of coach-specific training | International Coaching Federation |

| Small business litigation exposure, general benchmark | 36% to 53% of small businesses face litigation in a given year | SimplyBusiness |

A note on that last figure: it’s a general small-business litigation benchmark, not a coaching-specific statistic. No Canadian regulator or association currently publishes coaching-specific claim frequency data, since the profession isn’t regulated or centrally tracked. Treat it as a directional reference for how common business disputes are overall, not a coaching-industry forecast.

Does ICF Membership Include Insurance?

Usually not automatically. Membership and insurance are separate products, even when an association makes both easy to access in one place.

What ICF membership typically provides is preferred access to a group policy. Westminster Global administers a Master Policy for ICF members in the US and Canada, meaning members can qualify for professional liability coverage through that negotiated program rather than shopping the open market from scratch. It’s a discount and a convenience, not coverage that activates the moment you join.

Why Professional Membership Still Matters

Even setting insurance aside, professional membership carries weight. It signals credibility to corporate clients, ties you to a recognized code of ethics, and often unlocks continuing education that keeps your skills current. If you’re weighing whether certification is worth pursuing, our guide to life coaching certification in Canada breaks down the options.

What Happens If You Skip Insurance and Receive a Claim?

Common Claim Scenarios

Claims against coaches tend to follow a few patterns: a client alleges your advice led to business or financial losses, a coaching relationship ends in a contract dispute, a refund disagreement escalates, or a client claims you overstepped a professional boundary. None of these requires intent on your part to become expensive.

What Insurance Can and Cannot Do

Insurance can cover your legal defence, negotiate settlements, and pay out on covered claims, so your business and personal finances aren’t carrying that cost alone. What it cannot do is replace the groundwork that prevents disputes in the first place: a clear coaching agreement, ethical and well-documented sessions, and boundaries that keep you inside your scope of practice. Coverage and good practice management work together. Neither one substitutes for the other.

Do Online Coaches Need Different Coverage Than In-Person Coaches?

Online Coaching Risks

Coaching from behind a screen trades slip-and-fall risk for data risk. Client intake forms, session recordings, payment information, and notes stored in a client portal all create exposure if a platform is breached or a device is lost. This is where cyber liability coverage earns its keep.

Coaching Across Provincial Borders

Most Canadian professional liability policies extend coverage across provinces, so a coach based in Alberta working with clients in Ontario is typically still protected. Still, it’s worth confirming territorial coverage directly with your broker rather than assuming, since policy wording varies between insurers.

Coaching International Clients

If you take on clients in the US or elsewhere, tell your broker before you do. Cross-border coaching can affect your eligibility for certain policies, change your premium, and in some cases require different coverage limits or wording entirely. This is a quick conversation that can save you from a denied claim later.

When Should You Buy Insurance?

| Stage | Recommendation |

| Researching coaching as a career | Learn your coverage options |

| In training or certification | Compare policies and providers |

| Coaching for free or practicing | Assess your risk exposure |

| First paying client | Obtain coverage |

| Corporate contracts | Obtain coverage immediately |

| Workshops or live events | Obtain coverage immediately |

Do You Need Insurance Before Your First Client?

Not usually by law. But most coaches purchase coverage right around that point anyway, because that’s the moment real liability exposure begins. Waiting until after a claim happens isn’t a strategy; it’s a gamble.

Insurance Is Only One Piece of the Legal Puzzle

Coverage works best as part of a complete foundation, not a standalone fix. Pair your insurance with proper business registration, a signed coaching agreement for every client, organized record-keeping, GST/HST compliance once you cross the $30,000 threshold, and clear professional boundaries. For the full breakdown of what’s required to coach legally across Canada, read our guide to legal requirements for coaching in Canada. If you’re still in the early build phase, starting a coaching business in Canada walks you through the registration and setup step by step.

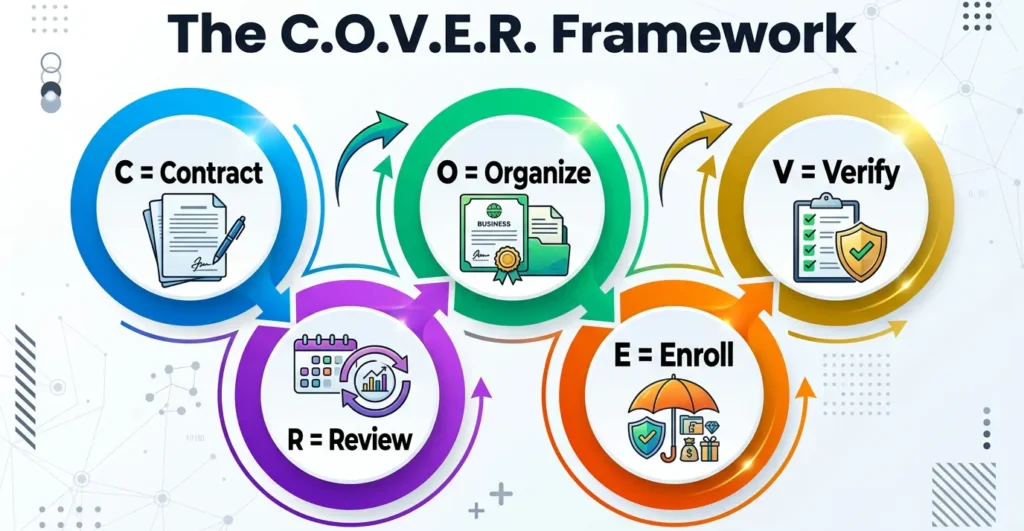

The 5-Step C.O.V.E.R. Framework for New Life Coaches

A simple way to remember what protects your practice, in order.

- Contract: Put a written coaching agreement in front of every client before your first session. It sets expectations and gives you a reference point if anything is ever disputed.

- Organize: Register your business name and choose a structure, whether that’s a sole proprietorship to start or something more formal as you grow.

- Verify: Confirm your legal, tax, and registration obligations for your province, including when GST/HST registration kicks in.

- Enroll: Purchase the coverage that matches how you actually work: professional liability at a minimum, with general liability or cyber liability added based on your delivery format.

- Review: Revisit your coverage once a year, and any time you add group programs, corporate clients, or international work that changes your risk profile.

Who Should Get Insured Right Away?

Prioritize insurance immediately if you:

- Already have paying clients

- Run workshops or live events

- Rent office space for sessions

- Coach corporate teams or organizations

- Store sensitive client information digitally

- Work with clients outside Canada

Who Can Reasonably Wait?

Coaches still in training, working only with free practice clients, or testing a niche with friends and family before launching publicly, carry lower exposure for now. That said, “later” should mean before your first paid engagement, not an indefinite postponement.

Frequently Asked Questions

Is life coach insurance legally required in Canada?

No. Coaching is unregulated in every Canadian province, so there’s no law requiring you to carry insurance. Professional associations, corporate clients, or venues may still require proof of coverage before they’ll work with you.

What does professional liability insurance actually cover for a life coach?

It covers claims that your coaching caused financial loss or harm, allegations of negligence or breach of professional duty, and the legal defence costs that come with fighting a claim, even an unfounded one. It does not cover bodily injury or property damage, which falls under general liability instead.

Can I buy life coach insurance before I’m certified?

Yes. Insurers base your eligibility and premium on the services you offer, not on whether you hold a specific credential. Certification can still strengthen your credibility with clients and some professional associations.

Does ICF membership automatically include insurance?

No. Membership gives you preferred access to a group policy, often through a Master Policy program, but you still need to enroll and pay for that coverage separately.

How much should I budget for life coach insurance in my first year?

Plan for somewhere between $315 and $1,000 CAD annually, depending on whether you carry professional liability alone or bundle in general liability and cyber coverage. Your exact premium will depend on your revenue, coverage limits, and the services you offer.

Conclusion

Insurance isn’t usually a legal requirement for life coaches in Canada, but it’s one of the simplest, most affordable ways to protect the business you’re working hard to build. Combine the right training, a clear coaching agreement, and appropriate coverage, and you’re free to focus on what actually matters: helping your clients take decisive action toward the life they want.

Ready to launch your coaching career on solid ground? Explore our Life Coach Training Certification in Canada program and build the coaching, ethical, and business foundations for a lasting practice.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.