The five strongest Canadian business bank accounts in 2026, ranked by real operating cost rather than marketing, are: RBC Digital Choice for incorporated startups that need a Big 5 lending relationship, BMO eBusiness Plan for zero monthly fees from a major bank, Venn for cross-border and USD-heavy operations, Wise Business for international payments at mid-market exchange rates, and EQ Bank Business for parking tax reserves and idle cash at interest.

The biggest hidden fees almost nobody flags are FX markups of 2.5 to 3.5 percent on USD conversions, wire fees of $30 to $80 plus intermediary deductions, Interac e-Transfer charges on legacy accounts, and per-transaction overages. For most incorporated startups, a hybrid setup using a Big 5 anchor plus a fintech layer beats any single account on total annual cost.

Key Takeaway:

- Choosing the right Canadian business bank account can significantly impact cash flow, fees, and day-to-day operations. The best account depends on your transaction volume, business size, cash handling needs, and plans for future growth.[1]

- Key factors to compare include monthly fees, transaction limits, e-transfer costs, branch access, online banking features, integration with accounting software, and availability of business credit products. A lower monthly fee is not always the most cost-effective option if transaction charges are high.[1]

- Digital business banking platforms can offer lower fees and streamlined operations, while traditional banks may provide stronger lending relationships, cash management services, and access to in-person support. The right choice depends on your business model and financial needs.[2]

- Business owners should review account terms regularly as transaction volume and banking requirements change. An account that works well during startup may become expensive or restrictive as the business grows.[2]

Bottom Line: The best Canadian business bank account is the one that aligns with your transaction volume, banking preferences, and growth plans. By comparing fees, features, integrations, and support options, business owners can reduce costs, improve cash management, and build a stronger financial foundation for long-term success.

- Source: Unleash Your Power – Comparing Canadian Business Bank Accounts

- Source: Unleash Your Power – Are Fintech Business Accounts Safe?

Here is a number that should bother every Canadian founder: the $6 a month business account that looks like a bargain on the rate card can quietly cost a growing startup four to six thousand dollars a year once the hidden fees stack up.

The monthly fee is the smallest line on your real bill. The damage happens in the places most rankings skip past. A 2.8 percent foreign exchange spread on USD client payments. A $45 outbound wire fee followed by another $20 deduction from an intermediary bank you never agreed to use. Fifteen e-Transfers above your monthly cap at $1.50 each. Cash deposits are charged at $2.50 per thousand.

This guide is a hidden-cost exposure report for incorporated Canadian startups, agencies, ecommerce founders, and SMBs trying to figure out where their banking dollars are actually going. You get five real recommendations, six fee categories that drain working capital invisibly, a worked annual-cost comparison, and a five-step audit framework you can run on your last 90 days of statements before you close this tab.

If you have ever wondered why your runway shrinks faster than your spreadsheet predicts, your bank account is a reasonable place to start looking.

Why Most “Best Business Bank Account” Rankings Are Misleading

Search “best Canadian business bank account,” and roughly eight of the top ten results are written by companies that also sell business bank accounts. The winner of the ranking is almost always the company that wrote the page.

The honest comparison starts with how your business actually moves money, matches the account structure to that pattern, then calculates the true annual cost. Monthly fees are the most visible number and the least important one. What matters is your transaction profile: how often you move money, what currencies you move it in, how much cash you handle, and whether you plan to apply for credit in the next 12 months. The cost categories that get glossed over consistently (FX markup, e-Transfer overages, wire deductions, cash deposit fees, USD spreads) are the ones that hurt the most.

The Real Cost of “Free” Business Banking in Canada

According to Venn’s 2026 analysis of Canadian business accounts, most accounts advertised as zero monthly fee actually carry meaningful costs hidden in transaction limits, e-Transfer charges, wire fees, and FX markups that can drain thousands annually. Wise Canada’s free-account guide points out that the foreign exchange markup alone can cost 3 to 5 percent of a transaction value at traditional banks, meaning a $5,000 payment to a US supplier carries roughly $150 in hidden cost before any wire fee gets added.

Run the math on a realistic profile. An incorporated consulting business processes 60 e-Transfers a month, sends two outbound USD wires a quarter, and converts roughly $8,000 USD a month in client receipts to CAD. At Big 5 pricing, that pattern carries an FX cost in the range of $2,400 to $3,300 a year, wire fees of $400 to $600, plus e-Transfer overages on top. None of those costs appear on the monthly summary as a single line item.

The Top 5 Canadian Business Bank Accounts for Startups & SMBs (2026)

RBC Digital Choice Business Account

RBC Digital Choice runs at $6 a month and includes unlimited electronic transactions, ten free Interac e-Transfers, unlimited mobile cheque deposits, and unlimited Moneris merchant deposits. For an incorporated startup planning to apply for a business credit card, line of credit, or term loan within 24 months, the lending relationship that comes with a Big 5 account history is genuinely valuable. The catch sits in FX and wire categories; pairing this account with Wise or Venn for cross-border flows is the smart hybrid play.

- Best for: incorporated startups planning to apply for credit, retail SMBs, Moneris-heavy businesses

- Avoid if: USD-heavy operations, frequent international wires

- Hidden cost risk: FX markup, wire fees, transaction profile mismatch as you scale

BMO eBusiness Plan

The BMO eBusiness Plan is a $0 monthly fee account from a major bank that actually delivers unlimited electronic transactions. According to Hardbacon’s 2026 business-banking review, this account fits incorporated consultants, freelancers scaling up to a corporate structure, and lean digital-first startups. Branch deposits cost extra, and opening requires a branch appointment in most regions, but for the right business, this is the cleanest domestic anchor available from a major Canadian bank.

- Best for: incorporated consultants, agency founders, lean digital startups

- Avoid if: cash-heavy businesses, retail with frequent branch deposits

- Hidden cost risk: branch transaction fees, cash deposit charges, and limited included e-Transfers

Venn

Venn is not technically a bank. According to Venn’s own disclosure, account balances are held at Bank of Montreal, a CDIC member. What you get is a financial operating platform purpose-built for incorporated Canadian businesses with cross-border activity: real CAD and USD account details, FX rates well below Big 5 pricing, 1 percent unlimited cashback on the corporate card, and accounting integrations with Xero and QuickBooks. Incorporation is required.

- Best for: incorporated agencies, SaaS startups, and ecommerce brands receiving USD through Stripe or Shopify

- Avoid if: unincorporated sole proprietors, cash-heavy businesses

- Hidden cost risk: limited physical banking functionality, no Canadian payroll on the platform itself

Wise Business

Wise uses the mid-market exchange rate and charges a transparent conversion fee of 0.4 to 0.6 percent, which is roughly 80 to 90 percent cheaper than Big 5 FX markups. No monthly fees, with a one-time registration fee of approximately $42 CAD. Wise does not support Interac e-Transfer, cannot pay CRA taxes directly, and lacks Canadian payroll integration. Treat it as a specialist tool that earns its keep on the FX line of your P&L while a primary domestic account handles everything else.

- Best for: ecommerce brands, agencies with international contractors, import and export businesses

- Avoid if: domestic-only operations, businesses wanting a single all-in-one account

- Hidden cost risk: limited Canadian payment infrastructure requires pairing with a domestic account

EQ Bank Business

EQ Bank Business is best understood not as a primary operating account but as a tax reserve and idle-cash bucket. The account pays meaningful interest on balances, charges zero monthly fees, and is directly CDIC-covered through EQ Bank’s own membership. According to Remitbee’s 2026 comparison, Canadian businesses moving operating reserves into EQ Bank have reported earning thousands in interest annually on funds that previously sat at zero yield. Position it as where your GST, HST, corporate tax, and emergency reserves sit until you need them.

- Best for: holding tax reserves, parking emergency operating funds

- Avoid if: this is your primary operating account, you need USD support

- Hidden cost risk: limited full-service business banking, not designed for daily operations

Top 5 Accounts at a Glance

| Account | Monthly fee | Transactions | FX cost | USD support | CDIC | Best for |

| RBC Digital Choice | $6 | Unlimited + 10 e-Transfers | 2.5 to 3% | Separate USD account | Direct member | Lending credibility to retail SMBs |

| BMO eBusiness Plan | $0 | Unlimited + 2 e-Transfers | 2.5 to 3% | Separate USD account | Direct member | Lean digital startups |

| Venn | $0 | Unlimited | 0.25 to 0.6% | Native CAD and USD | Held at BMO | USD-heavy agencies |

| Wise Business | $0 + $42 one-time | Unlimited | 0.4 to 0.6% | Native multi-currency | Held in trust | International payments |

| EQ Bank Business | $0 | Limited (reserve use) | N/A | None | Direct member | Tax reserves, idle cash |

The 6 Hidden Fees Most Canadian Business Owners Miss

FX markup on USD conversions

The single largest hidden cost. WealthNorth’s 2026 wire transfer guide explains it plainly: Canadian banks do not advertise their FX markup; they quote you a rate that runs 1.5 to 3 percent worse than the mid-market rate. On a $50,000 USD conversion, that markup quietly removes $750 to $1,500 before any wire fee gets added. Fintech alternatives like Wise and Venn charge 0.25 to 0.6 percent.

Interac e-Transfer overage fees

Big 5 business accounts typically include around ten e-Transfers per month, then charge for every additional one. According to Biller’s 2026 e-Transfer fee comparison, per-transfer charges run $1.00 to $1.50 on accounts without a premium package. A business sending 50 to 100 e-Transfers a month can rack up $500 to $1,200 a year in overages.

Wire transfer fees and intermediary deductions

Venn’s analysis of Canadian wire pricing shows banks typically charge $30 to $80 for outbound international wires, plus 2.5 to 3 percent FX markup, plus another $15 to $30 in intermediary fees deducted from the transfer amount itself. The intermediary deduction is the one most founders never see clearly because it happens on the recipient’s side.

Transaction overage charges

Most Big 5 plans include a fixed number of transactions per month, after which every additional item costs $0.65 to $1.25. A growing business that scales past its included count without upgrading can rack up $50 to $200 monthly before anyone notices.

Cash and coin deposit fees

Standard Big 5 pricing runs around $2.50 per $1,000 of cash deposited. A retail SMB depositing $20,000 monthly pays roughly $600 annually just to put money into its own account.

USD conversion spreads disguised as “convenience”

When you pay a USD invoice from a CAD account without first converting, your bank performs the conversion at its retail rate and pockets the spread silently. The fee never appears as a line item because it is baked into the exchange rate itself. The most invisible category on the list, and often the most expensive.

Data and Findings

Here is a modeled annual cost for a representative incorporated Canadian startup: a small agency with 60 monthly e-Transfers, $8,000 USD per month in client receipts converted to CAD, eight outbound USD wires per year, and roughly 180 electronic transactions per month overall.

| Cost category | Big 5 only setup | Hybrid setup (Big 5 + Venn or Wise) |

| Monthly account fee | $72 per year | $72 per year |

| FX markup on $96,000 USD annual conversion | $2,400 to $3,360 | $240 to $576 |

| e-Transfer overages (50 over included) | $600 to $900 | $600 to $900 |

| Wire fees (8 outbound) | $360 to $640 plus $120 to $240 intermediary | $0 to $100 |

| Transaction overages | $150 to $400 | minimal |

| Estimated annual total | $3,702 to $5,612 | $912 to $1,648 |

This is a modeled scenario based on the public fee schedules referenced throughout, not a guaranteed result. The pattern is consistent across every realistic profile: the hybrid setup beats the Big 5-only setup by roughly $2,000 to $4,000 a year for a small incorporated business, and the gap widens as USD activity grows.

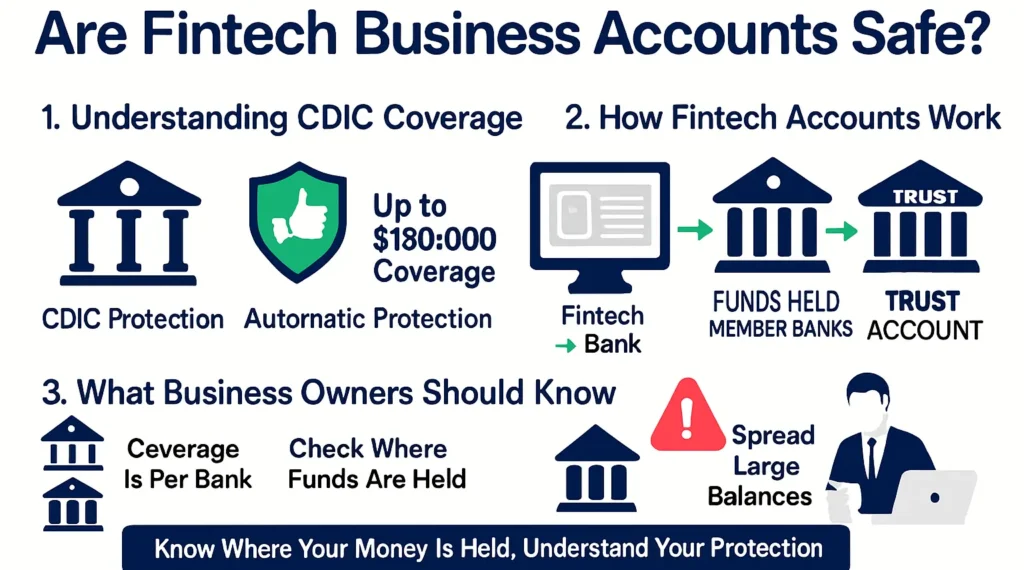

Are Fintech Business Accounts Safe? CDIC Coverage Explained

The Canada Deposit Insurance Corporation insures eligible deposits at member institutions up to $100,000 per insured category, per member institution. According to CDIC’s official coverage page, protection is automatic and applies to chequing and savings accounts in both Canadian and foreign currencies. For startups holding seed funding above six figures, you may need to spread funds across multiple CDIC member institutions for full coverage.

Fintech platforms need to be read carefully. Venn, Float, and similar platforms are not themselves banks. They are technology companies whose customer balances are held in trust at a CDIC member institution. According to Float’s explanation of CDIC for business accounts, this trust structure preserves CDIC coverage on the underlying deposits, but the coverage flows through the underlying bank.

Two practical implications. The $100,000 limit applies per member institution, not per platform; if your Venn balance is held at BMO and you also have a BMO business chequing account, both share the same ceiling at BMO. And platforms that hold funds in different structures may carry different protection. Always confirm the current disclosure before holding large balances.

Best Business Account by Business Type

| Business type | Best account |

| Incorporated consultant or solo founder | BMO eBusiness Plan |

| Ecommerce startup with US customers | Wise Business plus a domestic anchor |

| Retail SMB with cash deposits | RBC Digital Choice |

| USD-heavy agency or SaaS startup | Venn |

| Holding corporate tax reserves | EQ Bank Business |

| Planning a business loan in 12 months | RBC Digital Choice as primary |

Who Should Use a Big 5 Bank vs. a Fintech Stack?

When a Big 5 still wins

Lending relationships are the strongest case. Canadian lenders typically want to see six or more months of business statements from a recognized institution before approving a line of credit or term loan. A Big 5 also wins on branch access for cash-heavy operations and Moneris integration for in-person businesses.

When fintech wins

Cross-border activity. If your business receives USD from Stripe, Shopify, or international clients, or pays contractors in multiple currencies, FX savings alone justify the switch. Fintech also wins on onboarding speed, transparent pricing, and accounting integrations.

Why hybrid setups are the new default

The most cost-efficient setup in 2026 is rarely a single account. It is a stack: a Big 5 anchor for credibility and future lending, a fintech platform for USD operations, and a high-interest reserve account for idle cash. The total cost typically beats any single all-in-one solution.

The 5-Step Fee Audit Framework

A practical framework you can run on your last 90 days of statements.

Pull 90 days of statements

Download the full PDF, not the summary view. Line items matter more than totals.

Categorize every fee

Build six columns: monthly account fee, transaction overages, FX markup, wire and e-Transfer fees, cash deposit charges, and everything else.

Calculate your true cost per transaction

Divide the total quarterly banking cost by the total quarterly transaction count. The monthly fee divided by transaction count and true cost per transaction tends to be wildly different figures.

Match your banking structure to your actual behavior

The right structure is whichever carries the lowest annualized cost on your specific profile.

Switch or stack accounts strategically

Run new accounts in parallel for a month before fully migrating, so you do not get caught with pre-authorized debits hitting an account you have already closed.

Try this: Open your last 90 days of statements and highlight every charge under $5. Add them up. That number, multiplied by four, is what your “free” or “low fee” account actually costs you per year.

This kind of operational clarity is the financial equivalent of what NLP brings to leadership: you cannot lead a business effectively if you cannot see clearly where the resources are flowing. The gap between scaling and stalling often shows up first in how clearly the owner understands their own numbers.

Frequently Asked Questions

What is the cheapest business bank account in Canada?

The BMO eBusiness Plan at $0 a month is the cheapest account from a major Canadian bank, with unlimited electronic transactions. The cheapest account on paper is not necessarily the cheapest in practice once you factor in FX markup, wire fees, and overages.

Is Venn a real bank? Venn is a technology platform, not a chartered bank. Balances are held at Bank of Montreal, a CDIC member, and remain eligible for CDIC deposit insurance up to applicable limits.

Can I use Wise Business as my only Canadian business account?

Not really. Wise does not support Interac e-Transfer, cannot process CRA tax payments directly, and lacks Canadian payroll integration. Most Canadian businesses use Wise as a specialist tool alongside a primary domestic account.

Do I still need a Big 5 account for business loans?

In most cases, yes. Canadian lenders typically want to see six or more months of business statements from a recognized institution before approving a line of credit or term loan.

How much can FX markup cost a startup annually?

On $100,000 of annual USD conversion volume, a Big 5 markup of 2.8 percent costs roughly $2,800. A fintech platform charging 0.5 percent on the same volume costs $500.

Are fintech business accounts CDIC-insured?

Most reputable Canadian fintech business platforms partner with CDIC member institutions, and balances held at those institutions remain eligible for CDIC coverage up to $100,000 per insured category per member institution. Always confirm the current disclosure on the platform’s own terms page.

Conclusion

Most businesses do not lose money through one catastrophic decision. They lose it gradually, through invisible operational inefficiencies that compound quietly while the founder is busy doing the work that actually grows the business. Banking fees are one of the cleanest examples of this pattern, because the leakage happens in tiny amounts spread across hundreds of transactions, and almost nobody reconciles them line by line until somebody points out that the total runs into the thousands per year.

The fix is not complicated, but it does require clarity. Run the 90-day audit. Match your account structure to your actual transaction behavior. Stack accounts strategically if your profile is split. Stop paying Big 5 FX markups on USD activity that a fintech platform handles for a fraction of the cost. The money you free up is working capital you can put back into hiring, marketing, product or simply runway.

If you want help building that kind of operational clarity into the rest of your business, James’s business coaching in Toronto works with incorporated founders on exactly this kind of work: finding the invisible inefficiencies and turning them into capacity for growth. Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.