Profit First is a cash flow allocation system that flips the traditional accounting formula. Instead of treating profit as whatever is left over, you take a fixed percentage of every deposit and move it to a profit account before anything else gets touched. For Canadian solopreneurs, the system needs a Canadian translation.

You set up separate bank accounts for income, profit, owner’s pay, tax and CPP, GST/HST, and operating expenses. You allocate revenue by percentage on a fixed schedule. You quarantine GST/HST as money that was never yours. You pre-fund roughly 25 to 30 percent of net income for CRA taxes and 11.9 percent self-employed CPP. You pay yourself a steady amount from the owner’s pay account, and you force operating expenses to fit what is left.

Key Takeaway:

- Profit First is a cash management system that helps Canadian solopreneurs prioritize profitability by allocating income into separate accounts for profit, taxes, owner compensation, and operating expenses before spending occurs. [1]

- Rather than treating profit as whatever remains at the end of the month, the Profit First method makes profit a planned allocation. This creates better financial discipline, improves cash flow visibility, and reduces the risk of overspending as revenue grows. [1]

- Canadian solopreneurs can adapt the framework by accounting for GST/HST obligations, income taxes, seasonal revenue fluctuations, and industry-specific expenses. Regular allocation percentages help ensure tax liabilities and owner pay are consistently funded. [2]

- The system works best when combined with regular financial reviews, realistic expense management, and strategic reinvestment decisions. By controlling operating expenses and protecting profit first, business owners can build long-term financial stability and sustainable growth. [2]

Bottom Line: Profit First helps Canadian solopreneurs transform cash flow management by making profit intentional instead of accidental. By allocating revenue to profit, taxes, owner pay, and expenses from the start, business owners can improve financial stability, reduce stress, and create a more sustainable path to growth.

- Source: Unleash Your Power – Profit First for Canadian Solopreneurs

- Source: Unleash Your Power – How Much Profit Should a Small Business Reinvest Monthly?

What Is the Profit First Method?

Profit First is a cash flow system created by Mike Michalowicz in his 2014 book of the same name. The core idea is a simple inversion of the formula every business owner is taught.

Traditional accounting says: Sales minus Expenses equals Profit. Profit is whatever is left after the bills are paid. The problem is behavioural. When all your revenue sits in one account, your brain treats the entire balance as available money. Expenses expand to fill it. Profit becomes an afterthought, and most years, an accident.

Profit First says: Sales minus Profit equals Expenses. You decide what percentage of revenue becomes profit, you move it out of reach first, and you force the rest of the business to operate on what remains.

The method rests on a behavioural insight that anyone in business has experienced. We do not spend what we cannot see. Banks know this. Retirement plans know this. Profit First applies the same psychology to business cash flow.

What Profit First Is NOT

This trips up a lot of people, so it is worth being direct.

Profit First is not accounting software. It does not replace QuickBooks, Wave, or your bookkeeper. Profit First is not bookkeeping. You still need to categorize transactions and reconcile accounts. Profit First is not a tax strategy. It helps you save for taxes, but it does not reduce them. Profit First is not a budgeting app, and it is not a productivity hack.

What it is, plainly, is a behavioural cash flow allocation system. It is a way of moving money between accounts on a fixed schedule so that profit, taxes, and owner pay are protected before operating expenses get a chance to eat them.

Why Canadian Solopreneurs Struggle With Cash Flow

There are over 2.6 million self-employed Canadians, and roughly 46.2 percent of them run unincorporated businesses. That is more than a million sole proprietors filing T1 returns with a T2125 attached. Most of them know how to do the work. Far fewer know how to manage the cash flow that comes from doing the work.

The CFIB’s 2026 small business data shows that more than 20 percent of small business owners cite cash flow as a primary concern heading into the year. The failure data is worse. Roughly 22.6 percent of new small businesses close within their first year, and 48 percent of failed businesses cite running out of cash as the cause.

Revenue does not equal available cash. That is the line every Canadian solopreneur learns the hard way, usually in April, when the CRA wants money that has already been spent.

Canadian solopreneurs rarely fail for lack of revenue. They fail because taxes, operating costs, and inconsistent cash flow consume revenue before profit is protected.

Picture a consultant in Toronto earning $120,000 a year. On paper, that is a comfortable income. In practice, after 13 percent HST collected and owed back to the CRA, roughly 25 percent set aside for federal and provincial income tax, 11.9 percent for self-employed CPP, software subscriptions, professional development, accounting fees, a home office portion, and the irregular client-acquisition costs that come with running solo, the number that actually belongs to the consultant is far smaller than $120,000. If all of that money sits in one chequing account, the consultant feels rich on Tuesday and panicked on April 29th. The math has not changed. The visibility has.

How Profit First Works for a Canadian Solopreneur

The original Profit First system was written for US business owners. Canadian solopreneurs need an adapted version because the obligations are different.

In Canada, a sole proprietor is the business. There is no legal separation. You file a T1 personal income tax return with a T2125 Statement of Business or Professional Activities attached. You pay personal income tax on the net income your business generates. You pay both halves of the Canada Pension Plan contributions yourself, since there is no employer to match you.

You may need to collect and remit GST/HST. You may need to make quarterly tax instalments. And you have a split deadline that catches new solopreneurs every year: the filing deadline is June 15, but any balance owing is still due April 30.

This is why the Canadian version of Profit First needs an extra account, tighter tax allocations, and clearer rules around GST/HST. The percentages you copy from a US blog post will not match your reality.

A note on what follows: this is educational guidance, not personalized tax or accounting advice. Your specific allocations should be reviewed with a Canadian CPA who knows your situation.

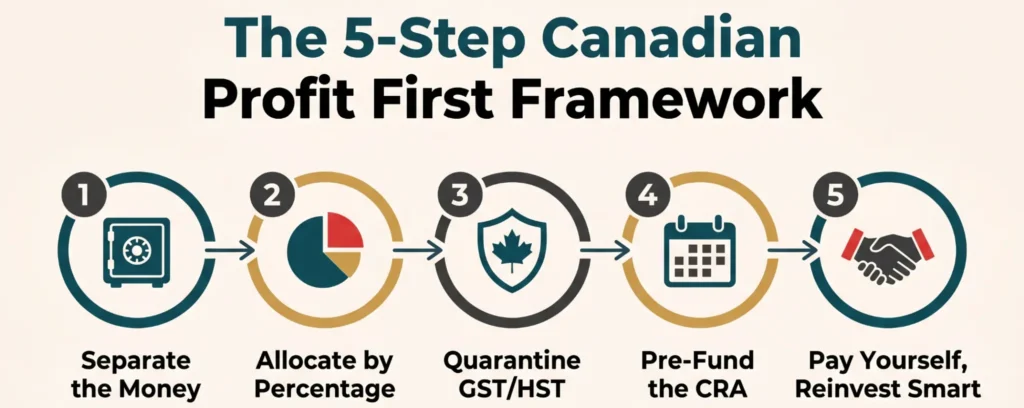

The Canadian Profit First Cash Flow Framework

Separate the Money Before It Tempts You

This is behavioural finance, not accounting. Willpower is not a financial system. If your profit, tax, and operating money all sit in one account, you will spend them as one pool. Every solopreneur who has ever said “I’ll set aside the tax money later” has learned this lesson at their own expense.

The fix is structural. You separate the accounts so that the money you should not touch is physically inaccessible from the money you can spend. You decide once, you automate the rest, and you stop relying on discipline you do not have at the moment of temptation.

One of James’s clients, Darren, came to coaching feeling stuck. He had a job that paid well, but he could not break through to promotions, raises, or the business he kept talking about starting. The work was internal. James calls these “goal blocks,” the invisible patterns that keep capable people running in place. Once Darren saw his own pattern clearly, the shifts in his thinking and behaviour followed quickly. Cash flow works the same way. The pattern of letting profit be whatever is left over is invisible until you build a system that exposes it.

Allocate by Percentage, Not by Mood

Every deposit that lands in your income account gets moved out on a fixed schedule, by percentage, to the other accounts. Twice a month works well for most solopreneurs. Pick two dates and stick to them.

Allocating by percentage matters because it scales. A 5 percent profit allocation works whether you bring in $3,000 or $30,000 that month. Allocating by mood does not scale, because mood does not scale.

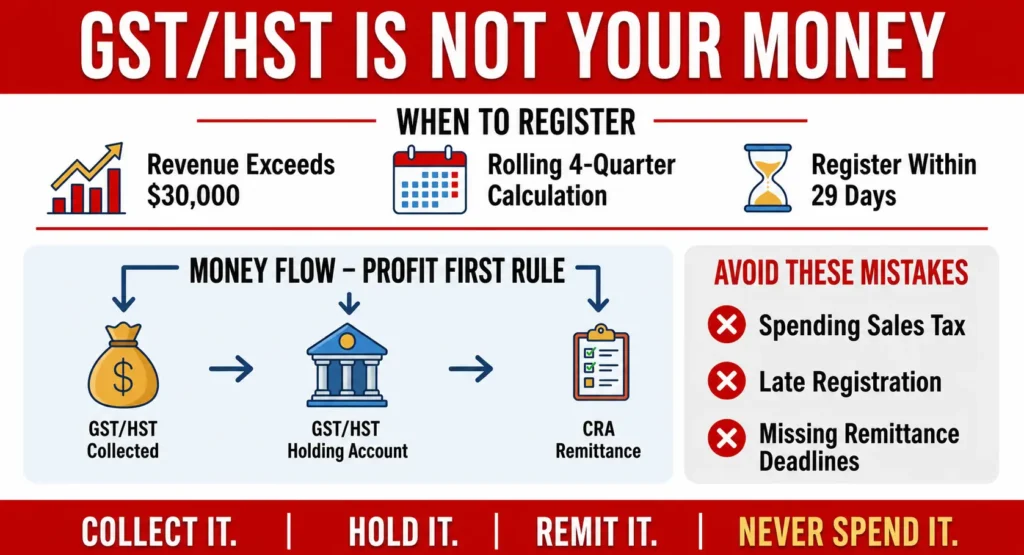

Quarantine GST/HST as Money That Was Never Yours

This is the single most important Canadian adaptation to Profit First, and the one that prevents the most pain.

When you charge 13 percent HST in Ontario or 5 percent GST in Alberta, that money is not your revenue. You are collecting it on behalf of the federal government. It belongs to the CRA from the moment your client pays the invoice. Treating it as cash flow is borrowing from the government at interest.

The fix is a dedicated GST/HST holding account. Every time a deposit lands, the sales tax portion moves immediately into that account and stays there until you remit. You never see it in your operating balance. It does not exist as far as your business decisions are concerned.

Pre-Fund the CRA Before It Comes Knocking

Income tax and CPP are not separate from the cost of doing business. They are the cost of doing business. Treating them as a year-end surprise is what creates the April panic.

Solopreneurs with net tax owing above $3,000 in the current year or either of the two previous years are generally required to make quarterly tax instalments to the CRA. The instalment dates for individuals are March 15, June 15, September 15, and December 15. Miss them and the CRA charges interest. As of 2026, the prescribed interest rate on overdue and instalment amounts is around 7 percent, compounded daily. It adds up faster than most solopreneurs expect.

A Tax and CPP account, pre-funded with every deposit, removes the panic entirely. When the instalment is due, the money is already there.

Pay Yourself Like an Employee, Reinvest Like an Owner

The owner’s pay account is the one most solopreneurs underuse. They pull money in irregular chunks, react to whatever the chequing balance shows that week, and never build the predictable personal cash flow that lets them plan a life.

The fix is to pay yourself a consistent amount on a consistent date, transferred from the owner’s pay account to your personal chequing. If the account does not have enough on payday, that is a signal, not an emergency. It tells you to look at pricing, capacity, or expenses, not to dip into tax money.

The profit account is for reinvestment, owner distributions every quarter, or a financial cushion. It is not for plugging holes in operating expenses. If you start using profit to subsidize expenses, the system stops working. The constraint is the point.

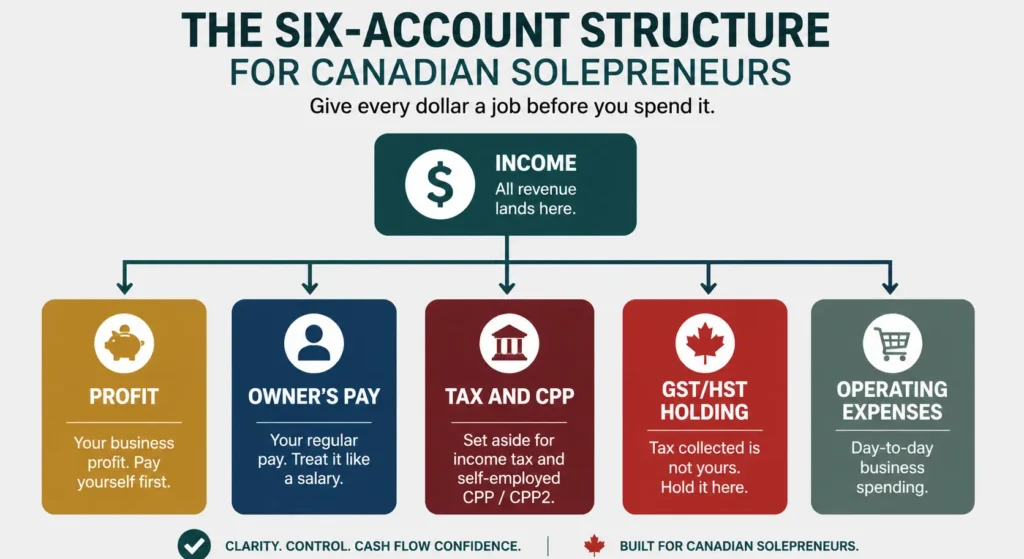

The Bank Account Structure Canadian Solopreneurs Actually Need

You do not need to open all of these on day one. Start with three or four, add as you grow. Most of the major Canadian small business banking options now let you open multiple chequing accounts under one business profile without monthly fees, which makes this far easier than it used to be.

- Income: The landing pad. Every client payment, every Stripe payout, every invoice lands here. Money does not stay here.

- Profit: A percentage of every deposit, moved here on allocation day and left alone.

- Owner’s Pay: The account that funds your personal life. Pays you on a consistent schedule.

- Tax and CPP: Pre-funded reserve for federal and provincial income tax, plus 11.9 percent self-employed CPP.

- GST/HST: Sales tax collected from clients. Never your money. Moves to CRA on your filing schedule.

- Operating Expenses: What is left after the other accounts are funded? Pays for software, contractors, professional services, the lot.

If you are still deciding where to open these, here is a comparison of the best free Canadian business bank accounts for solopreneurs that work well for multi-account setups.

Recommended Profit First Percentages for Canadian Solopreneurs

These are starting points, not rigid rules. Your industry, expenses, debt load, and revenue level all shift the numbers. The point is to pick a starting allocation and adjust quarterly.

| Annual Revenue | Profit | Owner’s Pay | Tax and CPP | Operating Expenses |

| Under $50,000 | 1 to 3% | 50 to 60% | 15 to 20% | 20 to 30% |

| $50,000 to $100,000 | 5 to 8% | 40 to 50% | 20 to 25% | 25 to 30% |

| $100,000 to $200,000 | 8 to 12% | 35 to 45% | 25 to 30% | 20 to 25% |

| $200,000+ | 10 to 15% | 30 to 40% | 28 to 32% | 20 to 25% |

These percentages apply to real revenue, which means total deposits minus pass-through costs like subcontractor fees and direct materials. For most service-based solopreneurs without subcontractors, real revenue and total revenue are the same number, with GST/HST already separated.

A note on CPP. Self-employed Canadians pay both halves of the contribution, which amounts to 11.9 percent on pensionable earnings between $3,500 and $71,300 in 2025. The enhanced CPP2 adds another 8 percent combined rate on earnings between $71,300 and $81,200. By the time you hit the maximum, you are looking at over $9,000 a year in CPP alone, on top of income tax. This is why the Tax and CPP allocation in the table runs higher than the US Profit First guides suggest. Canadian solopreneurs carry an obligation American solopreneurs do not.

For more details on what realistic profit margins look like at different stages, this guide on how much profit a small business should aim for covers the benchmarks across service industries.

Example Allocation for a Canadian Freelancer

Let’s make this concrete. A freelance designer in Ontario earns $8,000 in a typical month, charging 13 percent HST on top.

Total invoiced: $9,040 ($8,000 plus $1,040 HST)

Step one, the HST splits off immediately. $1,040 moves to the GST/HST Holding account on deposit day. The remaining $8,000 is the real revenue available for allocation.

Using the $100,000 to $200,000 row from the table above (this designer is on track for roughly $96,000 a year, so close to that tier):

| Account | Allocation | Amout |

| Profit | 8% | $640 |

| Owner’s Pay | 45% | $3,600 |

| Tax and CPP | 25% | $2,000 |

| Operating Expenses | 22% | $1,760 |

| Total | 100% | $8,000 |

The designer takes home $3,600 in predictable owner’s pay. The CRA gets $2,000 set aside, ready for the next instalment. Operating expenses run on $1,760, which forces real decisions about software stacks, subscriptions, and contractor spend. And $640 quietly builds the profit cushion that means December does not have to be terrifying.

The HST sits in its own account, untouched, waiting for the quarterly remittance.

Handling GST/HST Inside a Profit First System

If your total worldwide taxable revenue exceeds $30,000 across four consecutive calendar quarters, you are no longer considered a small supplier under CRA rules. You must register for GST/HST and begin collecting on all taxable sales.

The threshold is calculated on a rolling basis, not a calendar year. The moment your trailing four quarters cross $30,000, you have 29 days to register. Missing this is expensive. If you crossed the threshold in March but only registered in September, the CRA can assess you for HST on every taxable sale made from March onward, whether you collected it from your client or not. The tax comes out of your pocket.

This is why the GST/HST Holding account matters even if you are below the threshold. The moment you register, you have a sales tax obligation that is not your money. Treating it as cash flow is borrowing from the federal government at 7 percent interest, with penalties layered on top if you cannot remit on time.

Some Canadian solopreneurs also benefit from voluntary GST/HST registration before they hit $30,000, because it allows them to claim input tax credits on business expenses. That decision is worth a conversation with a CPA. Either way, the account structure remains the same. Sales tax in, sales tax out, never touched in between.

Setting Aside Income Tax, CPP, and CRA Instalments

A safe starting point for most Canadian solopreneurs is 25 to 30 percent of net business income set aside for federal and provincial income tax combined with CPP. Higher earners in high-tax provinces should push closer to 35 percent.

Three obligations need to be separated in your head, even if they come out of the same Tax and CPP account.

Income tax

Is calculated on your net business income (revenue minus deductible expenses) and added to your other income on the T1 return. It runs through Canada’s graduated tax brackets, combined federal and provincial.

CPP

Is a flat 11.9 percent on net self-employment earnings between $3,500 and $71,300, with an additional CPP2 contribution at 8 percent combined between $71,300 and $81,200. The employer’s half of CPP (5.95 percent) is deductible against your income, which softens the blow slightly.

GST/HST remittance

Is separate from both of the above. It comes from the GST/HST Holding account, not the Tax and CPP account. Confusing the two is one of the most common mistakes new solopreneurs make.

Quarterly instalments kick in when your net tax owing exceeds $3,000 in the current year or either of the two previous years. The CRA will send you instalment reminders. Ignoring them does not make them go away. It just compounds interest at 7 percent daily until the next reminder shows up, looking less friendly than the last one.

Common Profit First Mistakes Canadian Solopreneurs Make

Watch for these. Most of them are subtle, and most of them quietly undermine the entire system.

Mixing GST/HST with spending money.

This is the most common one. The HST account exists for a reason. If you raid it for operating costs, you are taking a loan from the CRA that you cannot afford.

Copying the US Profit First percentages blindly.

American solopreneurs do not pay 11.9 percent CPP. They have different tax brackets, different sales tax rules, and different filing structures. Canadian percentages need to be Canadian.

Underestimating CPP

This catches almost every first-year solopreneur. They calculate income tax, set aside what feels right, and forget that CPP alone can run over $9,000 a year at higher income levels.

Opening too many accounts at once

Start with three or four. Income, Tax and CPP, GST/HST, and one combined Operating account work fine for the first 90 days. Add the Profit and Owner’s Pay accounts once the rhythm is established. Trying to run six accounts on day one usually leads to giving up after week two.

Inconsistent allocation timing

Twice a month is the sweet spot. Once a month is too infrequent for cash flow visibility. Daily is too obsessive. Pick the 10th and 25th, or whatever pair of dates suits your client’s payment cycle, and stick to them.

Treating profit as leftovers again

The whole system collapses if profit becomes the residual. Profit comes first. If the operating account is short, the answer is to cut expenses or increase revenue, not to dip into profit.

Before vs After Profit First

| Before Profit First | After Profit First |

| One mixed account, no visibility | Purpose-based accounts, clear allocation |

| Tax bill triggers panic every April | Tax reserves already funded |

| Reactive spending based on chequing balance | Planned allocations on a fixed schedule |

| Revenue obsession (“how much did I bring in?”) | Profit awareness (“how much did I keep?”) |

| Unpredictable owner pay | Structured, consistent owner pay |

| GST/HST treated as cash flow | GST/HST quarantined as the CRA’s money |

Who Should Use This Strategy?

Profit First works well for Canadian solopreneurs who:

- Run service-based businesses with manageable overhead, including consultants, coaches, freelancers, designers, creators, and solo agencies

- Experience inconsistent cash flow month to month

- Feel stressed every tax season despite reasonable revenue

- Find themselves overspending in good months and panicking in slow ones

- Struggle to pay themselves consistently

- Want a system they can run without daily attention

The best fit is someone earning between $40,000 and $300,000 in annual revenue, where the math is simple enough to manage personally but the stakes are high enough to matter.

Who Should Avoid This Strategy?

Profit First is not the right fit for everyone. Specifically:

- Ultra-early-stage businesses with revenue under $20,000 a year. The percentages are too small to be meaningful. Focus on revenue first, system later.

- Heavy-inventory businesses where cash flow timing is dominated by purchasing cycles rather than service margins. The system can still work, but it needs significant adaptation.

- Founders are pursuing aggressive reinvestment. If you are deliberately running lean on owner pay to fund growth, the rigid percentages will feel like a straitjacket.

- Businesses with complex payroll beyond the solo owner. Profit First scales, but it scales with adjustments, not by default.

If any of these describe you, the principles still apply (separate accounts, planned allocations, profit awareness), but the specific percentages and accounts need a more customized build.

Pros and Cons of Profit First for Canadian Solopreneurs

| Pros | Cons |

| Cash flow visibility improves immediately | Requires discipline to maintain |

| Tax season stops being a crisis | Multiple bank accounts to manage |

| Owner’s pay becomes predictable | Adjustment period of 60 to 90 days |

| Operating expenses get healthier pressure | Can feel restrictive in early weeks |

| Profit is built in, not hoped for | Does not replace bookkeeping or tax filing |

| Forces honest conversations about pricing | Requires accurate revenue tracking |

Data and Findings

The case for a structured cash flow system is not theoretical. The numbers tell the story clearly.

Canadian Self-Employment Landscape

- More than 2.6 million Canadians are self-employed.

- 46.2% operate as unincorporated sole proprietors, meaning over 1.2 million people manage business cash flow and taxes on their own.

The Cash Flow Crisis

- 22.6% of Canadian small businesses fail within their first year.

- 48% of business failures are caused by running out of cash, making cash flow problems the leading cause of closure.

- More than 20% of small business owners cited cash flow as a top concern in 2026.

The Tax Burden Most Solopreneurs Underestimate

- Self-employed Canadians pay both halves of CPP, with maximum annual contributions exceeding $9,000.

- The CRA charges 7% interest, compounded daily, on overdue taxes.

- Quarterly tax instalments become mandatory once the net tax owing exceeds $3,000.

The GST/HST Trap

- Crossing $30,000 in revenue triggers mandatory GST/HST registration.

- Businesses have only 29 days to register after exceeding the threshold.

- Missing registration can result in $17,000+ in retroactive HST liability on $150,000 of Ontario sales.

Sources: Statistics Canada, TurboTax Canada, CFIB, Fortunly, BizFund, Canada.ca, CalcTax, and Gondaliya CPA.

What Profit First Adoption Tends to Produce

Across coaching engagements with solopreneurs and small business owners, a consistent pattern emerges when clients implement a structured allocation system like Profit First. Within the first 90 days, most report eliminating tax-season panic, achieving consistent owner pay for the first time in their business history, and identifying 10 to 20 percent of operating expenses that quietly disappeared without affecting output. The shift is not magical. It is structural. When money is separated by purpose, decisions about that money get made on purpose.

What This Data Means

Canadian solopreneurs are not failing because they are bad at their work. They are failing because the structural gap between earning and managing is filled by stress, guesswork, and reactive decisions. A cash flow system closes that gap. The Profit First method, adapted for Canadian tax and CPP realities, is one of the cleanest ways to do it.

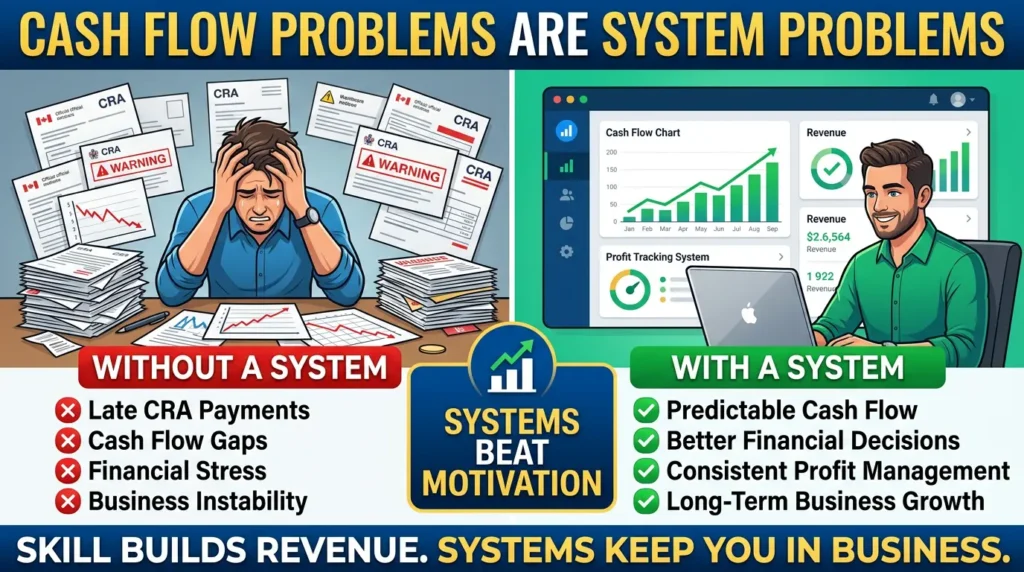

Why Cash Flow Systems Matter for Canadian Solopreneurs

The numbers above are sobering. Roughly one in five Canadian small businesses does not survive its first year. Nearly half of all failures come down to cash flow, not lack of demand, not lack of skill, not lack of effort.

These are not motivation problems. These are system problems. Solopreneurs who fail rarely do so because they have stopped trying. They fail because the gap between revenue and cash kept widening, the CRA bills kept arriving, and there was no structure in place to catch any of it.

A cash flow system fixes what motivation cannot. It builds the structure that makes good financial behaviour the default instead of the exception. It is the same reason James spends so much time with clients on why so many small businesses fail to grow, even when the founder is talented and the work is good. Skill alone does not survive a missing system.

What Happens in the First 90 Days?

- Week 1: Open the accounts you do not have. Decide your starting percentages. Set your two monthly allocation dates.

- Month 1: Run the system. Allocate twice. Notice the friction. Resist the urge to dip into the wrong accounts.

- Month 2: Look at your operating spend. The constraint will expose overspending you did not see before. Adjust where needed.

- Month 3: Tax and Profit reserves are visible and growing. Recalibrate percentages based on what the data shows.

By day 90, the system feels normal. By day 180, you wonder how you ran your business without it. By day 365, you have the cushion that lets you make decisions from a position of choice instead of fear.

For solopreneurs already generating consistent profit, smart reinvestment strategies become the next conversation. The profit account is no longer just a cushion. It becomes a growth lever.

Frequently Asked Questions

Does Profit First work in Canada?

Yes, with adaptation. The core method works anywhere, but Canadian solopreneurs need to add a GST/HST holding account, increase the tax allocation to cover 11.9 percent self-employed CPP, and align the system with CRA instalment cycles. US percentages copied directly will underfund your tax reserves.

How many bank accounts do I need?

Start with three or four: Income, Tax and CPP, GST/HST Holding, and a combined Operating account. Once the rhythm is established, add separate Profit and Owner’s Pay accounts. Most Canadian solopreneurs land on five or six accounts within the first six months.

Should GST/HST stay in a separate account?

Yes, always. The sales tax you collect is not your revenue. It belongs to the CRA from the moment a client pays. A dedicated holding account prevents the most common (and most expensive) mistake Canadian solopreneurs make, which is treating sales tax as cash flow.

How much should self-employed Canadians save for taxes?

A safe starting point is 25 to 30 percent of net business income, which covers federal and provincial income tax plus 11.9 percent self-employed CPP. Higher earners in high-tax provinces should push closer to 35 percent. Adjust based on your prior year’s actual tax bill and your CPA’s guidance.

Can incorporated businesses use Profit First?

Yes, with modifications. Incorporated business owners pay themselves through salary, dividends, or a combination, which changes how the Owner’s Pay and Tax accounts work. The core principles still apply, but the percentages and account flows look different.

Is Profit First good for freelancers?

Especially good, in fact. Freelancers have the most variable cash flow and the least built-in financial structure, which means they benefit most from a system that creates predictability. Service-based freelancers between $40,000 and $200,000 a year are the strongest fit.

What percentages should I start with?

For most Canadian solopreneurs earning $50,000 to $100,000, start with 5 percent profit, 45 percent owner’s pay, 22 percent tax and CPP, and 28 percent operating expenses. Adjust quarterly based on what the numbers actually show. The starting percentages matter less than the discipline of running the system consistently.

Conclusion

If your business generates revenue but you still feel constantly stressed about taxes, cash flow, or paying yourself consistently, the issue is probably not your income. It is your allocation system.

Canadian solopreneurs work hard. They serve clients well, deliver real value, and bring in real money. Where most of them lose ground is not in the doing. It is in the structure around the doing. A Profit First system, adapted for Canadian tax obligations, gives you back the visibility and predictability that let your business actually feel like a business instead of a perpetual emergency.

If you want help building the systems and mindset behind sustainable solopreneur growth, this is the kind of work James does with clients every week. Profit First is one piece. Pricing, positioning, capacity, and the internal patterns that quietly cap your income are the others. Business coaching that improves profitability starts where this article ends.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.