Hidden Canadian bank fees are quietly draining $1,000 to $50,000 or more from small and medium businesses every year. The six main culprits are monthly maintenance charges, transaction overage fees, NSF penalties, wire transfer fees, foreign exchange (FX) markups baked into exchange rates, and intermediary bank deductions on international SWIFT transfers.

Canada’s Big Six banks control 93 per cent of the banking sector, which limits price competition and keeps fees structurally higher than in comparable countries like the UK and Australia. Most business owners never audit these costs because they’re fragmented, normalised, and rarely itemised clearly on statements.

The fix starts with a 90-day fee audit, followed by a straightforward comparison of credit unions and fintech alternatives that offer FX markups as low as 0.25 per cent versus the bank standard of 2 to 3 per cent. Recovering even a fraction of these fees redirects real growth capital back into your business.

Key Takeaway:

- Many Canadian businesses unknowingly lose money through hidden bank fees such as transaction overages, wire transfer charges, overdraft penalties, foreign exchange markups, and payment processing costs. [1]

- Foreign exchange spreads are often one of the biggest hidden costs, with banks adding markups that can significantly increase the true cost of international payments and cross-border transfers. [2]

- Common “invisible” fees include monthly maintenance charges, ATM fees, excess transaction fees, dormant account fees, bill payment charges, and cash deposit limits that quietly reduce cash flow over time. [3]

- Businesses can reduce banking costs by reviewing fee schedules carefully, negotiating pricing, choosing accounts aligned with transaction volume, and using transparent fintech or digital banking solutions when appropriate. [4]

- The best way to avoid hidden fees is proactive monitoring business owners who regularly audit statements and understand fee structures are far less likely to lose money to unnecessary banking charges.

Bottom Line: Hidden bank fees in Canada can quietly drain business profits through transaction costs, FX markups, and service charges. Businesses that actively review their banking setup and optimize fee structures can significantly improve long-term cash flow and profitability.

- Source: The Hidden Business Banking Fees Businesses Should Know About

- Source: Wise – Hidden FX and Wire Transfer Costs in Canada

- Source: Common Bank Fees in Canada and How to Avoid Them

- Source: Business Bank Account Fees and Hidden Charges (2026)

You sit down to review your cash flow. Revenue looks decent. Expenses look familiar. But the numbers still don’t add up, and you can’t quite put your finger on why.

Here’s what most Canadian entrepreneurs never consider: it’s not your revenue model. It’s not your pricing. It might not even be your overhead. It could be the institution you trust with every dollar your business earns.

Canada’s banking system is one of the most concentrated in the developed world, and that concentration has a direct cost to you. Business owners across the country are quietly losing thousands every year to hidden bank fees that never show up as a single line item, never trigger an alert, and never get audited because they feel like just part of the deal.

They’re not part of the deal. They’re a choice. And once you see what’s actually happening inside your bank statements, you won’t be able to unsee it.

By the end of this article, you’ll know exactly which fees are draining your business, what the real dollar cost looks like at your revenue level, and what it takes to stop the bleed for good.

How Much Are Hidden Bank Fees Costing Canadian Businesses?

Most business owners underestimate this number by a wide margin. The average Canadian pays over $250 per year in personal banking fees, more than consumers in the UK and Australia, according to research by North Economics. For businesses, the losses scale considerably faster.

Small businesses typically lose $1,000 to $10,000 annually to banking inefficiencies. For scaling businesses with regular cross-border payments, that number climbs to $50,000 or more, driven primarily by FX markups. According to Float Financial, banking costs quietly erode 1 to 2 per cent of total business revenue for companies making frequent international payments.

The money isn’t vanishing dramatically. That’s what makes it so dangerous. It leaks slowly, category by category, month after month, in amounts small enough that no single line item ever triggers a real conversation.

| Business Stage | Annual Revenue | Fee Leakage/Year | What It Could Fund |

| Freelancer / Solopreneur | $100K | $1,200 – $2,000 | 2 months of software tools |

| Small Business | $500K | $3,000 – $8,000 | Part-time contractor (1 quarter) |

| Growing SMB | $1M | $5,000 – $15,000 | Full growth marketing budget |

| Scaling Business | $2M+ | $10,000 – $50,000+ | A new team member or market expansion |

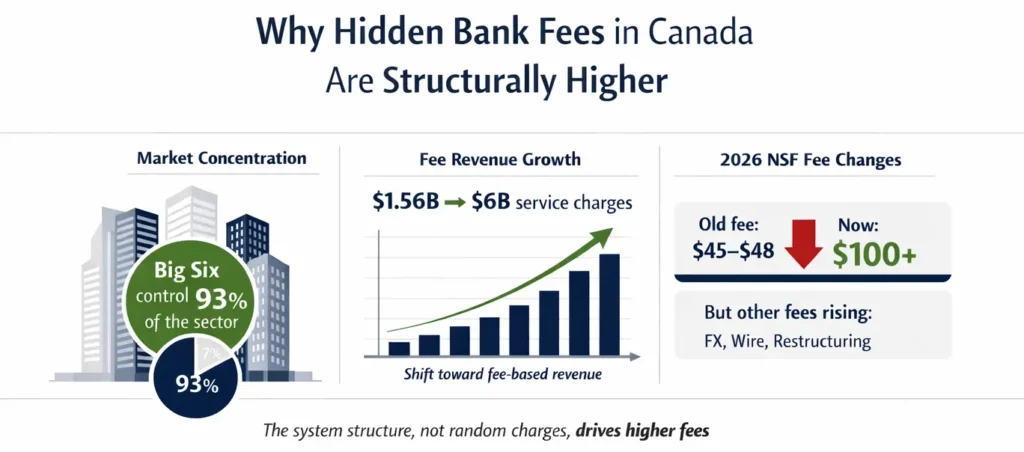

Why Hidden Bank Fees in Canada Are Structurally Higher

Canada’s fee problem isn’t random. It’s the product of a concentrated banking system that has little incentive to compete on price.

The Big Six Oligopoly and Its Real Impact

Canada’s Big Six banks control 93 per cent of the banking sector, according to a Fraser Institute report. When a handful of institutions dominate an entire market, price pressure disappears. Canadian banks consistently charge more relative to their deposit base than major UK retail banks, and that gap has persisted for decades. Economists have increasingly described Canada’s financial sector as an oligopoly, and the data support that framing.

The Shift Toward Fee-Based Revenue

Banks didn’t always rely on fees this heavily. According to The Logic, nearly 48 per cent of Canadian bank revenue in 2022 came from non-interest income, which includes everyday banking charges. Service charges on retail and commercial deposit accounts totalled nearly $6 billion in Q3 2025, up 267 per cent from $1.56 billion in the same quarter in 1996. Fees became a revenue recovery mechanism as traditional interest income slowed. The service didn’t improve. The bill did.

The 2026 NSF Fee Cap: Progress With a Catch

As of March 2026, banks can no longer charge more than $10 in NSF fees, down from the previous $45 to $48 per incident. That’s a meaningful win for businesses running lean on cash flow. The pattern to watch, though, is where banks recover that lost revenue. When one fee gets capped, others tend to quietly expand. FX markups, account restructuring, and wire fee adjustments are the likely pressure valves. The cap helps, but it doesn’t change the underlying incentive structure.

The 6 Hidden Canadian Bank Fees Draining Your Business

These are the six categories that account for the vast majority of avoidable banking costs for Canadian businesses.

Monthly Fees and Minimum Balance Traps

Standard business account maintenance fees range from $10 to $65 per month, according to CanadianSME. Some accounts waive the monthly fee if you maintain a minimum daily balance, which sounds reasonable until you realise you’re parking $65,000 in a low-yield account just to avoid a $65 monthly charge. That idle capital has a real opportunity cost. It’s not earning meaningfully, and it’s money you can’t deploy elsewhere.

Transaction Overages: The $0.40 That Becomes $1,200

Many “affordable” business accounts include 12 to 25 free transactions per month with per-transaction fees beyond that. At $0.40 to $1.25 per additional transaction, a growing e-commerce business or high-volume operation can accumulate hundreds in overage fees without noticing. Forty cents per transaction feels trivial. Three hundred transactions a month across a year does not.

NSF and Overdraft Fees

NSF fees are now capped at $10 per incident as of March 2026, but the structural risk remains. The Canadian Federation of Independent Business reports that 74 per cent of Canadian SMEs have experienced late customer payments. Any timing gap between incoming and outgoing payments can still trigger a charge, and repeated incidents across multiple accounts add up faster than most owners track.

Wire Transfer Fees: The Visible Tip of a Larger Iceberg

Canadian banks charge $30 to $80 per outgoing international wire transfer, and $15 to $30 for domestic wires, according to Airwallex. That fee is at least visible. The more expensive layers are what follow behind it.

FX Markup: The Most Expensive Fee You’ve Never Seen Itemised

When your bank processes a foreign currency payment, it applies its own internal exchange rate rather than the mid-market rate available publicly. The difference is the FX markup, and banks typically charge 2 to 3 percent on every currency conversion. This markup is not listed as a separate line item. It’s embedded in the rate itself, which is why most business owners never realise they’re paying it.

For a $6 million revenue business working with international suppliers, Float Financial found this category alone was costing between $40,000 and $50,000 annually. That’s a full team member. Gone silently.

Intermediary Bank Fees: The SWIFT “Leak”

When you send an international wire via the SWIFT network, your payment doesn’t travel directly from your bank to your recipient’s bank. It passes through intermediary institutions along the way, and each one can deduct $15 to $50 from the transfer amount. Your recipient gets less than you sent, and the deductions aren’t disclosed upfront. According to Venn’s 2026 international transfer guide, the all-in cost of a $10,000 bank wire, including base fee, FX markup, and intermediary deductions, often lands between $300 and $420. The number on the fee schedule is almost never the whole story.

The Real Dollar Cost: What Two Fee Categories Actually Charge You

True Cost of a $10,000 International Transfer: Banks vs Fintech

| Fee Component | Big Banks | Credit Unions | Fintech Platforms |

| Monthly Account Fee | $30 – $120/mo | $10 – $40/mo | $0 – $20/mo |

| FX Markup | 2% – 3% | 1.5% – 2% | 0.25% – 1% |

| Outgoing Wire Fee | $30 – $80 | $15 – $45 | $6 – $15 |

| Intermediary (SWIFT) | $15 – $50 hidden | $15 – $30 hidden | $0 (local rails) |

| NSF Fee (post Mar 2026) | Capped at $10 | Capped at $10 | $0 – $5 |

| Total Cost ($10K wire) | $300 – $420 | $200 – $300 | $31 – $55 |

Why Smart Business Owners Still Miss These Fees

The fees are significant. The information is available. So why do so few entrepreneurs catch them?

The Operational Blind Spot

Recurring costs become invisible over time. When a charge appears at roughly the same level every month, the brain files it as a baseline. You stop questioning whether it should exist and start working around it. Float Financial’s 2024 SMB State of the Nation report found that 43 percent of Canadian SMBs operate without clear visibility into their cash flow. You can’t challenge a cost you can’t clearly see.

Automation Bias in Banking

Entrepreneurs typically scrutinise software subscriptions and vendor invoices far more carefully than bank statements. Banking fees arrive pre-formatted, look official, and get filed. There’s a default assumption that what the bank charges is the going rate. That assumption is costing you real money every single month.

The Cost of Avoiding Financial Clarity

Darren G. came to James feeling blocked, stuck despite real effort, good income, and genuine ambition. Working together, they surfaced the blind spots: patterns of avoidance dressed up as acceptance that were quietly capping his results. Once those blocks were exposed and cleared, his decisions and outcomes shifted. The banking fee problem works the same way. Accepting a cost you never consciously agreed to is a decision pattern, not just a financial one. And it’s one you can change.

Try this: Open last month’s bank statement right now. Highlight every line that isn’t a vendor payment, payroll, or deposit. Total what’s left. That number is your starting point.

Data & Findings: What the Numbers Show About Canadian Banking Costs

Based on Unleash Your Power’s 2026 Business Performance Review, cross-referenced with published SMB banking research.

Across entrepreneurs who have worked through financial clarity coaching with James R. Elliot, a consistent pattern emerges. Before actively auditing their banking costs, the majority had never formally reviewed their fee structure, even among owners managing $500K to $2M in annual revenue.

Key findings from published research and client-facing data:

- 40 per cent of Canadian SMBs report financial difficulties escalated over the past year, with high financial product fees cited as a top driver, per Float Financial’s 2024 SMB Report.

- 65 per cent of SMBs dealing with cash flow problems cite long transaction processing times as a contributing factor, according to the same report.

- 43 per cent of SMBs operate without sufficient cash flow visibility to predict potential problems, leaving fee leakage undetected for months or years.

- One $6M revenue company tracked by Float Financial was losing $40,000 to $50,000 annually in FX costs, an amount that had never been formally identified or audited before working with a financial clarity advisor.

- Venn’s 2026 data shows the total cost of a $10,000 international transfer at Canada’s major banks runs $300 to $420 all in, versus $31 to $55 at leading fintech platforms.

- Businesses that actively track cash flow and reduce banking friction are 2.5 times more likely to grow revenue year-over-year, according to Float Financial planning data.

What this means: The gap between what business owners think they’re paying in banking costs and what they’re actually paying is wide, consistent, and fixable. The businesses that close that gap do so through clarity first, then decisive action. Both of those are learnable skills.

Smarter Banking Options for Canadian Businesses

For businesses operating primarily in Canada with low transaction volumes, a credit union cuts meaningful costs over a Big Bank. For any business making regular international payments or scaling toward multi-currency operations, fintech platforms deliver the sharpest reduction, especially on FX. If you need lending, a hybrid model works well: keep a credit relationship at a major bank while moving transactional and international banking to a fintech. For a detailed breakdown of what’s available by stage, the best bank accounts for small businesses in Canada guide covers current options clearly.

Credit Unions: Relationship-Based Banking With Real Benefits

Credit unions like Innovation Federal Credit Union offer lower monthly fees, profit-sharing structures, and a community-focused model. The tradeoff is scale. Digital tools, international payment infrastructure, and multi-currency support are typically limited. A solid choice for businesses operating domestically with predictable transaction volumes.

Fintech Platforms: Built for How Businesses Actually Operate Today

Fintech business accounts offer FX markups of 0.25 to 1 per cent compared to the 2 to 3 per cent bank standard, according to Venn’s 2026 business banking guide. Most offer free local CAD and USD accounts, no maintenance fees, direct accounting integrations, and international transfers via local payment rails rather than SWIFT, which eliminates most intermediary deductions. Funds are protected through CDIC-insured partner institutions. For early-stage companies, the bank accounts guide for Canadian startups breaks down which platforms have zero minimum balance requirements and the simplest setup.

Who Should Audit and Switch Their Banking?

This applies directly to you if:

- Your business makes international payments more than once a month

- You’ve never formally reviewed your bank’s full fee schedule

- You’re running at $300K revenue or above and haven’t compared alternatives in the past two years

- Your monthly bank statement includes charges you can’t explain or don’t remember choosing

- You’re converting foreign currency through a Big Bank account regularly

This is less urgent if:

- Your business operates entirely in CAD with low transaction volumes

- You have an active lending relationship tied to your current bank that would be disrupted by switching

- You’ve audited your fees in the last 12 months and confirmed they’re competitive

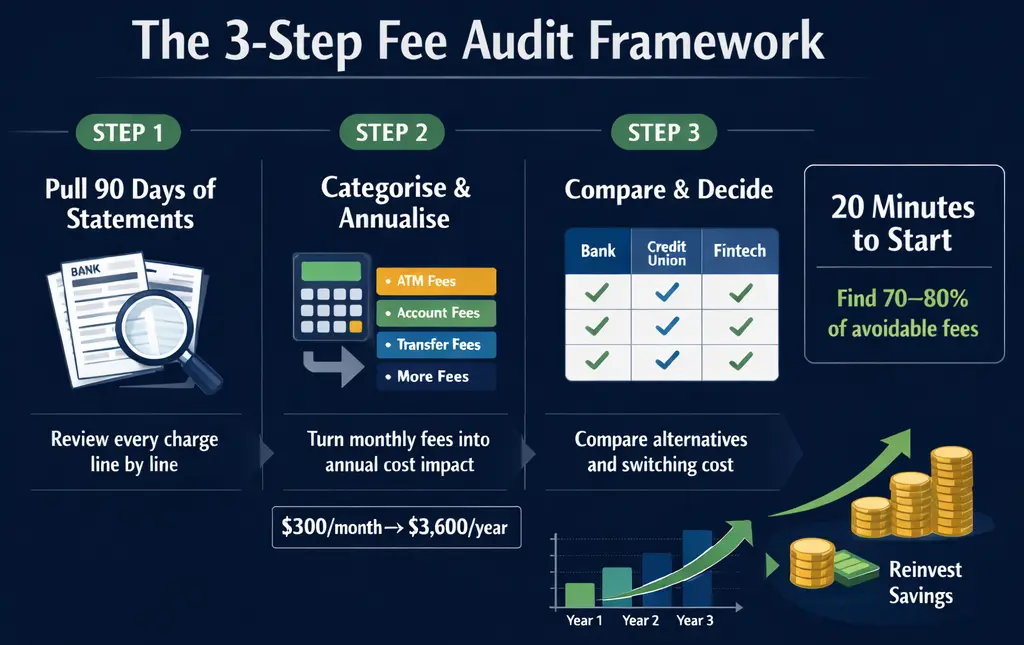

The 3-Step Fee Audit Framework

This framework takes 20 minutes to start and typically surfaces 70 to 80 per cent of avoidable fees on the first pass.

Step 1: Pull 90 Days of Statements:

Download three months of statements from every business account. Go line by line. Flag every charge that isn’t a direct supplier payment, payroll disbursement, or deposit. Don’t estimate. See every number clearly.

Step 2: Categorise and Annualise:

Sort flagged items into categories: monthly maintenance, transaction overages, wire fees, FX-related costs, NSF or overdraft charges. Total each. Then multiply by 12. A $300 monthly fee becomes a $3,600 annual decision the moment you see it written as a full-year number. That reframing changes how you act on it.

Step 3: Compare and Decide:

Run your totals against two alternatives: one credit union and one fintech platform. The smart reinvestment strategies guide can help you think through where recovered fees could go once redirected into your business. The question isn’t whether switching is a hassle. The question is what staying is costing you compounded over three years.

Try this: Block 90 minutes this week. Label it “Fee Audit.” Run this framework once. The clarity alone changes how you see your banking relationship going forward.

Is It Worth Switching Business Bank Accounts in Canada?

How much could switching realistically save?

For a business transferring $150,000 internationally per year, moving from a 2.5 per cent bank FX markup to a 0.5 per cent fintech rate recovers $3,000 annually from that line alone. Add lower wire fees and reduced monthly charges, and total first-year savings for a mid-sized business commonly exceed $5,000 to $15,000.

How disruptive is the transition?

Updating direct deposits, pre-authorised debits, and client payment details takes effort. Most businesses complete the core transition in two to four weeks. The time cost is real but finite. The fee cost at a high-rate bank is ongoing and compounds every year.

Are fintech accounts as safe as banks?

Reputable Canadian fintech business accounts hold funds through CDIC-insured partner institutions. Your deposits carry the same protection as a traditional bank account. Verify this before opening any account. Regulated fintechs are registered with FINTRAC and operate within full Canadian compliance frameworks.

What if I need business lending?

Most fintech platforms don’t offer business credit lines or loans. If lending is part of your banking relationship, a hybrid model works well: maintain a credit facility at your current bank while moving day-to-day transactional banking and international payments to a lower-cost platform. You get the best of both without sacrificing access to capital.

Frequently Asked Questions

What are the most common hidden bank fees in Canadian business accounts?

The six main categories are monthly maintenance fees, per-transaction overage charges, NSF and overdraft fees, wire transfer fees, FX markups embedded in exchange rates, and intermediary bank deductions on SWIFT international transfers. FX markups are the largest and least visible because they’re built into the exchange rate shown to you, rather than listed as a separate charge on your statement.

How much do Canadian banks charge for international wire transfers?

The stated transfer fee ranges from $30 to $80 per outgoing international wire at Canada’s major banks. But that’s only part of the total. Add 2 to 3 per cent in FX markup and $15 to $50 in potential intermediary deductions, and the all-in cost of a $10,000 transfer routinely lands between $300 and $420. The number on the fee schedule is almost never the real number.

What is an FX markup and why does it affect my cash flow?

An FX markup is the spread between the mid-market exchange rate you’d see on Google and the rate your bank applies when converting currencies. Banks typically add 2 to 3 per cent to the mid-market rate and embed this in the exchange rate shown to you, rather than listing it as a fee. For businesses making frequent international payments, FX markup is often the largest banking cost they’ve never tracked.

Can switching business bank accounts actually save money in Canada?

Yes, and the savings are often significant from the first month. Moving from a Big Bank FX markup of 2.5 per cent to a fintech rate of 0.5 percent saves $200 per $10,000 transferred. For a business sending $200,000 internationally per year, that’s $4,000 back before touching any other fee category. Factor in lower wire fees and reduced monthly charges, and annual savings for a mid-sized business commonly exceed $8,000 to $15,000.

Conclusion: Stop Accepting Silent Losses

Hidden bank fees are not a fixed cost of doing business. They’re an unreviewed variable, and every month you don’t review them is a month the bank wins by default.

The path forward is clear. Audit your last 90 days. Categorise what you find. Compare your numbers against real alternatives. Then make a decisive choice with actual data in front of you, not assumptions baked in years ago when you first opened that account. The businesses that master their cost structure, including the costs they’ve been conditioned to accept without question, are the ones that unlock genuine, sustainable growth.

Here’s what I’ve seen across more than 20 years of working with entrepreneurs and business leaders as a Board Designated NLP Trainer and business coach: the same mental pattern that makes it easier to accept an unexplained bank fee than to question it shows up in pricing, hiring, and growth strategy, too. Financial blind spots rarely travel alone. If you’re ready to break through the kind of passive acceptance that quietly caps what’s possible, working with a business coach in Toronto or exploring NLP training for business gives you the tools to see those patterns clearly and transform them decisively. Recovering your banking fees is the practical first step. Changing how you make decisions is what sustains growth.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.