The decision between sole proprietorship vs. incorporation in Canada comes down to one number: your net profit. Incorporation wins on tax once that figure consistently clears $60,000 to $100,000. A sole proprietor pays personal marginal rates past 50%. An Ontario CCPC pays as little as 11.7% on the same income in 2026. At $120,000 in profit, that gap means $20,000 or more in immediate tax deferral. But this is a deferred advantage, not a permanent saving. It only works when you retain earnings inside the corporation. Factor in $1,500 to $3,000 in annual compliance costs, and the math tells you everything.

Key Takeaway:

- A sole proprietorship is the simplest business structure in Canada easy to start, low-cost, and fully controlled by the owner but it comes with unlimited personal liability and income taxed at personal rates. [1]

- Incorporation creates a separate legal entity that protects personal assets, offers lower corporate tax rates on retained earnings, and makes it easier to scale, hire, and access financing. [2]

- The key trade-off is simplicity vs scalability: sole proprietorships have minimal paperwork and costs, while corporations require ongoing compliance, accounting, and legal structure. [1]

- Incorporation often becomes worthwhile when profits grow and you can leave money inside the business, benefiting from lower corporate tax rates and reinvestment advantages. [2]

- For many Canadian entrepreneurs, the typical path is starting as a sole proprietor for simplicity, then incorporating later as revenue, risk, and growth opportunities increase.

Bottom Line: Choose a sole proprietorship for simplicity and low cost in early stages, but consider incorporation as your business grows, profits increase, and the need for liability protection and tax efficiency becomes more important.

- Source: Sole Proprietorship in Canada Guide (2026)

- Source: BDC – Sole Proprietorship vs Incorporation

For many Canadian entrepreneurs, choosing the wrong business structure quietly costs $10,000 to $25,000 per year in unnecessary taxes. That money does not go to better equipment, more staff, or a smarter exit plan. It goes to the CRA.

In Canada, every self-employed person operates under a business structure from day one. A sole proprietorship is the simplest option: you and the business are one legal entity, and all income lands on your personal T1 return. A corporation creates a separate legal entity with its own tax return, its own liability protection, and access to significantly lower rates through the federal Small Business Deduction.

The structure you choose at $50,000 in profit rarely stays optimal at $150,000. Here is exactly how to know when to move, and how much it is actually worth.

How Sole Proprietors Are Taxed in Canada

As a sole proprietor, you and your business are legally the same entity. Every dollar your business earns flows directly onto your personal T1 tax return and is taxed at your marginal income tax rate. The CRA treats all sole proprietorship income as personal income, with no mechanism to defer or retain it inside a separate legal entity.

That marginal rate escalates as your income grows. In Ontario, combined federal and provincial marginal rates range from roughly 20% at lower income levels to over 53% at the top bracket. There is no separation between what the business earns and what you personally owe.

Sole proprietors cannot defer tax by retaining earnings. Whatever the business makes, you pay personal tax on it in the same year. There is no mechanism to split income with a spouse through the business structure or hold profits inside a separate legal entity. Those limitations become expensive as your income climbs.

On the upside, business losses as a sole proprietor can be written off directly against your other personal income sources, including employment income. That loss-utilization advantage is real and worth understanding before deciding to incorporate.

How Incorporated Businesses Are Taxed in Canada

A corporation is a separate legal entity that files its own tax return, the T2 Corporate Income Tax Return. The business and the owner are legally distinct, which changes everything about how income is taxed.

Canadian-Controlled Private Corporations (CCPCs) qualify for the Small Business Deduction (SBD), which reduces the federal corporate tax rate from 15% to 9% on the first $500,000 of active business income. The CRA Small Business Deduction rules confirm this rate applies to qualifying CCPCs with active business income under the business limit. Each province adds its own small business rate on top.

In Ontario for 2026, the combined federal and provincial small business rate is approximately 11.7% (blended across the year, with the provincial rate dropping from 3.2% to 2.2% on July 1, 2026, as confirmed by the 2026 Ontario Budget). From 2027 onward, the full combined rate moves to 11.2%.

As an incorporated business owner, you also have flexibility in how you pay yourself. You can take a salary, pay yourself dividends from after-tax corporate profits, or combine both approaches. That flexibility is one of the structural advantages that a sole proprietorship cannot replicate.

Real Numbers: The Tax Gap Between Structures

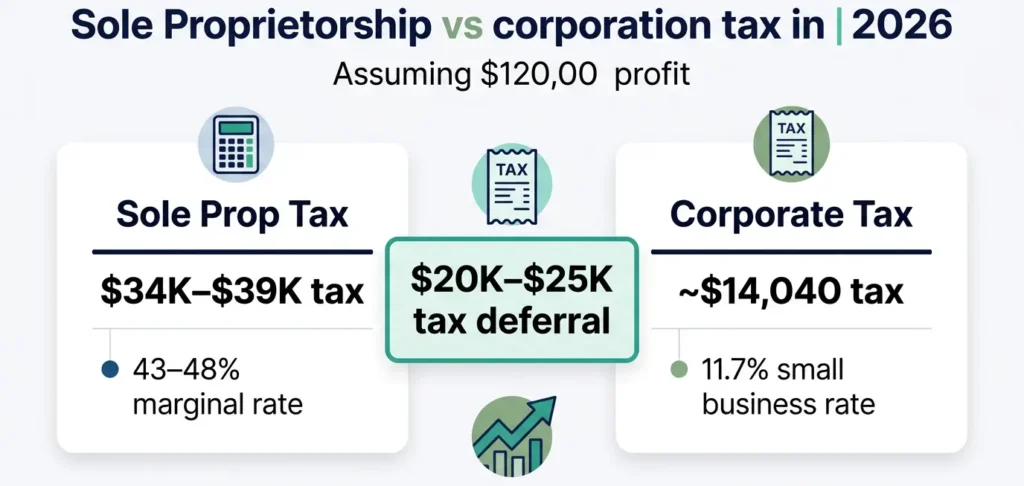

The difference between structures is clearest when you run actual numbers. Here is a straightforward Ontario comparison at $120,000 in net business profit for 2026.

Sole Proprietorship at $120,000 Net Profit (Ontario, 2026)

All income: flows to your personal return at marginal rates

Estimated personal tax: $34,000 to $39,000 (after federal/Ontario brackets, CPP, basic personal amount)

Marginal rate on top income: 43% to 48%

Corporation at $120,000 Net Profit (Ontario, 2026)

Corporate tax rate: ~11.7% (blended small business rate)

Corporate tax on $120,000: ~$14,040

Retained after-tax earnings: ~$105,960 (available for reinvestment)

Estimated Tax Deferral

Potential immediate tax gap: $20,000 to $25,000 at this income level

Important: This is primarily a tax deferral advantage, not always a permanent tax saving. When you eventually withdraw those retained earnings as dividends, you will pay personal tax on them. The real power of incorporation is in the time value of that deferral and the opportunity to reinvest at the lower corporate rate in the meantime.

Tax Savings by Province (2026)

The federal small business rate is 9% across Canada. Provincial rates vary, which means the combined rate and the benefit of incorporation differ depending on where you operate.

| Province | Combined Small Business Rate (2026) | Approx. Top Personal Marginal Rate |

|---|---|---|

| Ontario | 11.7% (blended 2026); 11.2% from 2027 | ~53.5% |

| British Columbia | ~11% | ~53.5% |

| Alberta | ~11% | ~48% |

| Quebec | ~12.2% | ~53.3% |

| Saskatchewan | ~10% | ~47.5% |

| Nova Scotia | ~12.5% | ~54% |

Note: Combined rates based on BDO Canada corporate income tax table and provincial 2026 budgets. Provincial rates are subject to annual budget changes. Always confirm with a CPA before making structural decisions.

The gap between personal marginal rates and corporate small business rates is significant in every province. Alberta and British Columbia entrepreneurs often reach the breakeven point slightly earlier than Ontario entrepreneurs because the personal tax differential is more pronounced.

The $60,000 to $100,000 Threshold: When Incorporation Starts to Win

Most Canadian CPAs and tax professionals align on a consistent range: incorporation typically starts to make financial sense when annual net business profit consistently exceeds $60,000 to $100,000.

Below that threshold, the compliance overhead often erodes the tax savings. Incorporation costs include government registration fees (around $360 in Ontario), plus annual accounting and legal costs that typically run between $1,500 and $3,000 per year. At lower profit levels, those costs can outpace the tax benefit.

The breakeven point also shifts by province. Ontario entrepreneurs may reach around $55,000 in annual profit; Alberta entrepreneurs often see the math work closer to $50,000. The wider the gap between your personal marginal rate and the corporate rate, the earlier incorporation becomes worthwhile.

One important caveat: incorporation saves the most when you are not withdrawing every dollar out of the corporation each year. If you need to draw all of your profit as personal income, the tax benefit shrinks substantially because the deferral advantage disappears.

Thinking through how much profit your business should actually keep is a useful exercise before making this decision.

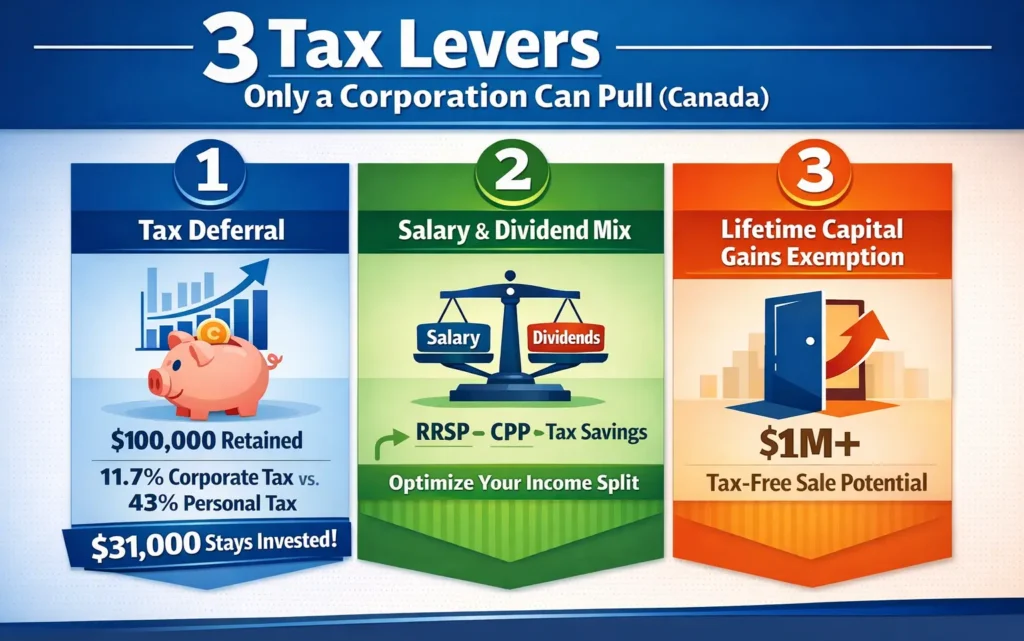

Three Tax Levers Only a Corporation Can Pull

Tax Deferral Through Retained Earnings

The most powerful advantage of incorporation is the ability to leave profits inside the corporation at the low corporate rate. If your marginal personal tax rate is 43% and the corporate rate is 11.7%, retaining $100,000 inside the corporation instead of drawing it personally keeps roughly $31,000 working for you rather than going to the CRA.

Developing smart reinvestment strategies for those retained earnings is where the real long-term compounding begins.

Salary and Dividend Mix Optimization

Incorporated owners can pay themselves through a combination of salary and dividends. A salary creates RRSP contribution room and CPP contributions. Dividends are taxed at a lower rate but do not create RRSP room. Working with an accountant to find the optimal split for your personal situation can save thousands annually.

Lifetime Capital Gains Exemption

When you sell the shares of a qualifying small business corporation (QSBC), you may be eligible for over $1 million in tax-free capital gains under the Lifetime Capital Gains Exemption (2025 figures). This is one of the most significant exit planning advantages available to Canadian entrepreneurs and is only accessible through a corporation.

The Hidden Costs and Tax Traps of Incorporation

Incorporation is not without its pitfalls, and the ones that catch entrepreneurs off guard tend to be the least discussed.

The Passive Income Trap

If your corporation earns more than $50,000 in passive investment income (interest, rent, portfolio dividends, net capital gains), the federal Small Business Deduction begins to phase out. At $150,000 in passive investment income, the federal SBD is eliminated entirely, and your active business income is taxed at the general corporate rate of 15% federally.

Ontario and New Brunswick are important exceptions to this rule at the provincial level. Even if your federal SBD is reduced or eliminated due to passive income, Ontario’s provincial SBD remains intact, preserving the provincial portion of the tax advantage. Most other provinces do follow the federal passive income grinddown, so this distinction matters significantly for Ontario entrepreneurs.

Annual Compliance Costs

Running a corporation requires a separate T2 corporate tax return, corporate minute books, potential payroll remittances if you take a salary, and annual legal or accounting maintenance. Budgeting $1,500 to $3,000 per year for these costs is realistic.

Loss Utilization

If your corporation operates at a loss, those losses stay inside the corporation. They can be carried back three years or forward twenty years, but they cannot be used to offset your personal income the way a sole proprietor’s losses can. For entrepreneurs in early-stage businesses expecting losses, staying as a sole proprietor preserves that personal tax flexibility.

Sole Proprietorship vs. Incorporation: Full Comparison

| Factor | Sole Proprietorship | Corporation |

|---|---|---|

| Tax filing | Personal T1 return | Separate T2 corporate return |

| Tax rate on income | Personal marginal rate (up to 53%+) | As low as 11.2% in Ontario (2027) on the first $500,000 |

| Personal liability | Unlimited | Limited to investment in shares |

| Compliance cost | Low (no separate return needed) | $1,500 to $3,000 per year |

| Income flexibility | None: all income taxed personally | Salary, dividends, or a combination |

| Loss utilization | Can offset other personal income | Losses remain inside the corporation |

| Exit planning | Difficult to sell or transfer | Shares sold with potential LCGE |

| Ideal income range | Net profit under $60,000 | Net profit consistently above $60,000 to $100,000 |

Who Should Stay a Sole Proprietor

Sole proprietorship is the right call in specific situations. It is not simply a stepping stone to incorporation. For many entrepreneurs, it is the correct long-term structure.

Consider staying as a sole proprietor if your net annual profit is consistently below $60,000, if you are in an early stage and testing your business model, or if you expect business losses you want to apply against other personal income sources such as employment earnings.

Sole proprietorship also makes sense if you are withdrawing virtually all of your income each year and have no plans to retain and reinvest earnings inside the business. Without the ability to defer income inside a corporation, the tax advantage of incorporation diminishes significantly.

A short-term side hustle or project-based contract work often does not justify the compliance overhead of incorporation.

Understanding why small businesses fail to grow often comes down to structural decisions made too early, or too late, for the wrong reasons.

Who Should Incorporate

Many entrepreneurs delay incorporation not because of the numbers, but because they still see themselves as freelancers rather than business owners. As Darren discovered when he worked with James, the identity shift often has to come before the financial decision can.

Incorporate if your annual net profit is consistently $60,000 to $100,000 or more, especially if you plan to retain and reinvest a portion of those earnings inside the business. High-liability service work, including consulting, coaching, and technology development, makes the liability protection of incorporation valuable beyond just the tax benefit.

If you are planning a long-term business exit or sale, the Lifetime Capital Gains Exemption is only available on corporate shares. Building that exit structure early can mean over $1 million in tax-free proceeds when you eventually sell.

Setting up the right bank accounts for your Canadian startup is one of the practical early steps once the decision to incorporate is made.

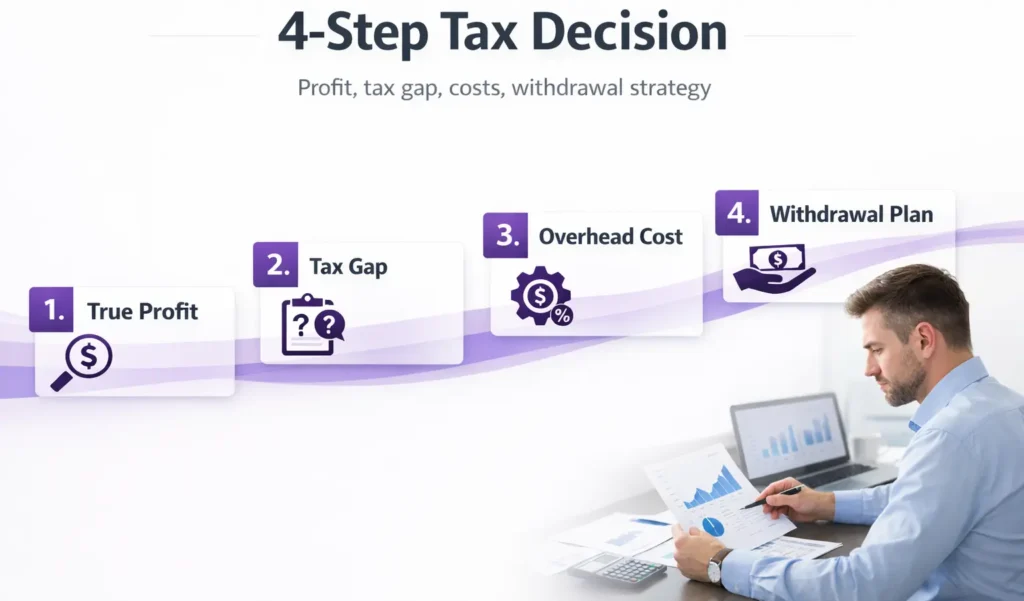

The 4-Step Structure Clarity Framework

Choosing between sole proprietorship and incorporation does not need to be a guessing game. After 20+ years of working with Canadian entrepreneurs as a Board Designated NLP Trainer and business coach, I’ve seen the same four decision points come up consistently.

Step 1: Calculate True Profit

Start with revenue, subtract all legitimate business expenses, and arrive at your actual net profit. Not revenue. Not what is in your bank account. Net profit after costs. Many entrepreneurs base their incorporation decision on gross revenue, which leads to poor choices in both directions.

Step 2: Model the Tax Gap

Compare your estimated personal marginal tax rate against the combined small business corporate rate for your province. The wider the gap, the stronger the case for incorporation. Use a rough estimate first, then refine it with an accountant.

Step 3: Estimate the Overhead

Add up the realistic annual cost of maintaining a corporation in your province, including accounting fees, legal compliance, and your own time. Then compare that number to your estimated annual tax savings. If the savings comfortably exceed the overhead, incorporation likely makes sense.

Step 4: Define Your Withdrawal Strategy

Ask yourself honestly: how much of your corporate profit do you intend to leave inside the business each year? The deferral advantage of incorporation is greatest when retained earnings compound at the corporate rate over time. If you need every dollar personally each year, the advantage shrinks.

Working through this framework with a business coach in Toronto or your province can accelerate the clarity significantly.

FAQ: Sole Proprietorship vs. Incorporation in Canada

At what income should I incorporate in Canada?

Most Canadian tax professionals recommend considering incorporation once annual net profit consistently exceeds $60,000 to $100,000. The exact breakeven point varies by province. Ontario entrepreneurs often reach around $55,000; Alberta entrepreneurs are closer to $50,000. Below that range, annual compliance costs of $1,500 to $3,000 can outweigh the tax savings.

Does incorporation permanently save tax in Canada?

Not permanently. Much of the benefit is tax deferral rather than tax elimination. Profits retained inside a corporation are taxed at the low corporate rate (as little as 11.2% in Ontario from 2027). When those profits are eventually withdrawn as salary or dividends, personal tax applies. The real advantage is compounding those retained earnings at the corporate rate over time.

Is incorporation worth it for a side hustle in Canada?

Usually not below $50,000 in net profit. If you are withdrawing all income and not retaining earnings, the deferral advantage disappears and you are left with $1,500 to $3,000 in compliance costs and no material tax benefit. Start as a sole proprietor, track your profit, and incorporate once the math clearly works in your favour.

Can I write off business losses as a corporation in Canada?

No, not against your personal income. Corporate losses stay inside the corporation. They can be carried back three years or forward twenty years to offset future corporate income, but they cannot be applied against your personal T4 employment or investment income. Sole proprietors can write off business losses against other personal income in the same tax year, which makes sole proprietorship more advantageous in early-stage loss periods.

What is the Small Business Deduction in Canada?

The Small Business Deduction (SBD) is a federal tax reduction available to qualifying Canadian-Controlled Private Corporations (CCPCs). It reduces the federal corporate tax rate from 15% to 9% on the first $500,000 of active business income. Combined with provincial small business rates, the total corporate tax rate drops to roughly 11% to 13%, depending on the province. The CRA outlines full SBD eligibility criteria, including rules around associated corporations and passive income limits.

Conclusion

The answer to “sole proprietorship or corporation?” is not universal. It depends on your profit level, your province, how much you plan to retain inside the business, and what your long-term exit looks like.

What is universal is that this decision deserves more than a quick search. The numbers involved, especially as your income grows, are significant enough to warrant a proper analysis of your specific situation.

Book a tax-structure strategy call and we will calculate your exact breakeven point based on your province, profit level, and withdrawal needs. You will walk away knowing precisely whether incorporation saves you money and when to make the move.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.