Business cash flow is the net movement of money into and out of your business and for scaling Canadian companies, how you manage and reinvest that flow determines whether growth compounds or stalls.

Scaling-stage Canadian businesses typically reinvest 30-50% of net profit into talent, systems, and market growth while maintaining 3-6 months of operating reserves. This range supports sustainable expansion without overextending cash, and Canada has become significantly more tax-efficient for R&D-intensive businesses in 2026, with SR&ED expenditure limits doubled to $6M and capital expenses restored as eligible claims following Bill C-15 (Royal Assent March 26, 2026).

The real bottleneck for most founders past the startup stage is not cash. It is the clarity and decision framework needed to deploy it without second-guessing every move.

Key Takeaway:

- Canadian businesses in growth mode typically reinvest 30–50% of net profit into talent, systems, automation, and market expansion while preserving liquidity for day-to-day operations.

- Maintain a cash reserve of 3–6 months of operating expenses before making major reinvestment decisions to protect against delayed receivables, seasonal slowdowns, or market shifts.

- The highest-return reinvestment areas usually include customer acquisition, process automation, team development, and technology upgrades, as these directly improve revenue velocity and efficiency.

- Reinvestment should be tied to measurable ROI benchmarks such as CAC payback, margin improvement, retention lift, or time saved per workflow rather than emotional spending.

- Sustainable growth comes from balancing aggressive reinvestment with strong cash flow discipline, ensuring the business scales without creating liquidity stress.

Bottom Line: The most resilient Canadian businesses reinvest strategically into growth drivers while protecting cash reserves. Strong cash flow management turns profit into scalable momentum without sacrificing stability.

What Is Business Cash Flow?

Business cash flow is the movement of money into and out of your business over a given period. Cash coming in includes revenue from sales, client payments, and any financing received. Cash going out covers operating expenses, payroll, loan repayments, taxes, and supplier costs. A business with positive cash flow brings in more than it spends, creating the surplus that funds reinvestment, reserves, and growth. Negative cash flow means the reverse: more is leaving than arriving, which forces reliance on credit or depletes reserves even when revenue looks healthy on paper. For scaling businesses, managing the timing and volume of both sides of this equation is what separates sustainable growth from a constant scramble for working capital.

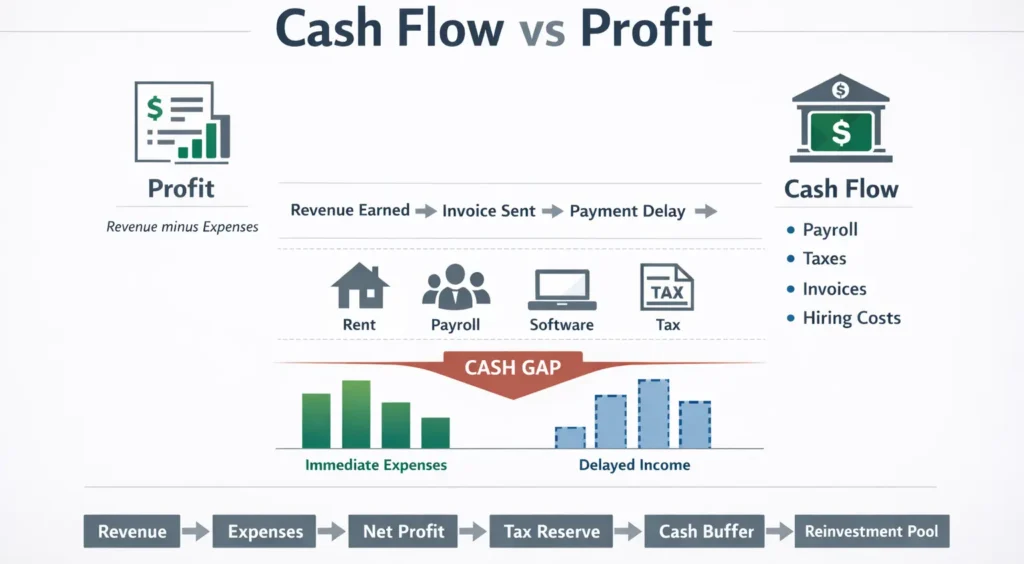

Cash Flow vs. Profit: Why the Distinction Determines Your Reinvestment Capacity

You can be profitable and still run out of money. That sounds contradictory until you understand the timing gap that trips up most scaling businesses.

Profit is what your financial statements report. Cash flow is what is actually in your account when a vendor invoice hits, a tax installment falls due, or a hiring opportunity appears. These two numbers rarely align and at the scaling stage, the gap between them can be wide enough to stall growth entirely.

The Timing Problem That Trips Up Scaling Businesses

When revenue grows faster than your collections infrastructure, receivables pile up. You have earned the money, but it has not arrived yet. Meanwhile, fixed costs like payroll, rent, and software subscriptions do not wait. That mismatch is one of the most consistent reasons a scaling business under margin pressure feels like it is shrinking even while revenue climbs.

According to a 2024 Canadian Western Bank study of more than 500 SME owners and decision-makers, 60% of Canadian small and medium-sized businesses reported ongoing cash flow challenges, with timing mismatches between inflows and outflows cited as a primary driver.

Calculating Your True Available Profit

Before you reinvest a single dollar, calculate available profit, not gross profit, not revenue. Net profit is total revenue minus all operating expenses, including your salary. From that figure, subtract long-term debt obligations, tax reserves (typically 25-30% of net profit for incorporated Canadian businesses), and the minimum cash buffer you are maintaining. Most advisors recommend three to six months of operating expenses as a floor. What remains is your deployable reinvestment pool.

Getting this number right is the foundation of every reinvestment decision that follows.

How Much Should a Scaling Canadian Business Reinvest?

There is no universal percentage but there are well-established benchmarks for each growth stage.

For scaling-stage businesses past the early startup phase, typically $500K to $5M in annual revenue, research consistently points to 30-50% of net profit as the balanced growth range. This supports sustainable expansion without overextending operating reserves. Businesses in the $3M to $5M revenue band often operate with 8-20% net margins, translating to $250K-$1M in annual profit and how that pool is allocated is one of the highest-leverage decisions a founder makes each year.

The Three Reinvestment Tiers

At a Glance: Reinvestment Tiers

20-30% of net profit = Conservative (stable, income-focused businesses)

30-50% of net profit = Balanced sweet spot (scaling businesses with recurring revenue)

50-70% of net profit = Aggressive (rapid expansion or exit preparation)

| Tier | Reinvestment Rate | Best Fit | Risk Level | Outcome Horizon |

| Conservative | 20-30% | Stable, mature businesses prioritising income | Low | 2-4 years |

| Balanced (Sweet Spot) | 30-50% | Scaling businesses with recurring revenue | Moderate | 1-3 years |

| Aggressive | 50-70% | Businesses pursuing rapid expansion or exit prep | Higher | 6-18 months |

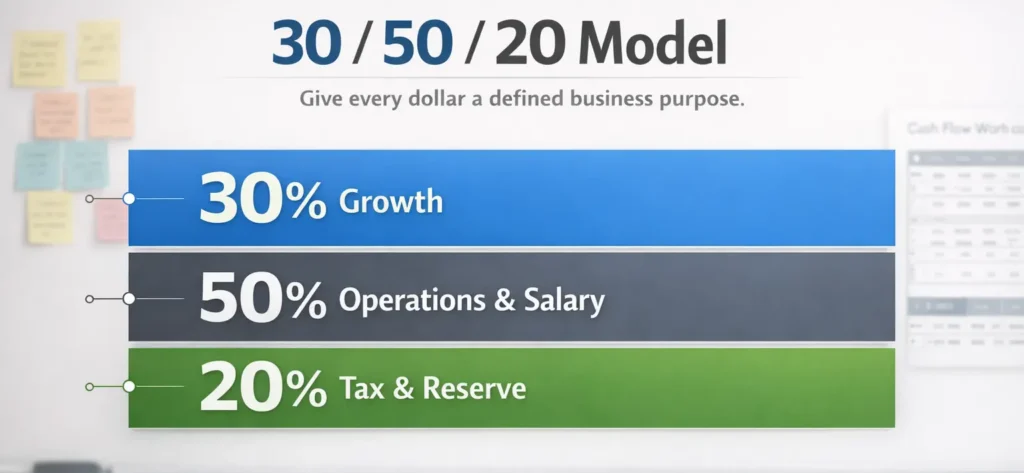

The 30/50/20 Allocation Model

A practical model many scaling businesses apply is the 30/50/20 split: 30% of net profit for growth reinvestment, 50% for operating expenses and owner salary, and 20% for tax reserves and contingency. This model ensures every dollar has a defined purpose. For more details on calibrating this to your specific situation, see this guide on how much profit to reinvest based on your stage and industry context.

The Cash Flow Traps That Stall Scaling Businesses

Scaling creates new cash flow vulnerabilities that did not exist in the startup phase. Most of them are predictable and avoidable.

Lifestyle Creep and the Fixed-Expense Trap

When revenue grows, personal and business expenses tend to grow with it. The risk is that personal fixed costs, such as mortgages, vehicles, and private school fees, do not adjust when the business has a slow quarter. A scaling business under margin pressure that has also expanded the owner’s personal lifestyle on the assumption that every strong year will repeat is operating with very little resilience.

Revenue-First Thinking

Sales numbers feel like cash. They are not. A business that closed $200K in new contracts last month but collects on net-60 terms has not yet generated usable capital. The Canadian Federation of Independent Business has noted that approximately 50% of small businesses identify cash flow constraints as a direct barrier to investment, and much of that constraint comes from treating booked revenue as available cash.

The Mindset Layer: Why Smart Owners Still Freeze at the Reinvestment Decision

Cash flow management is as much behavioral as it is mathematical. Harvard Business Review research has documented that business owners with proactive financial habits who schedule cash flow reviews and automate invoice tracking consistently outperform reactive counterparts even at identical revenue levels. The difference is not resources. It is a mindset and habit structure.

Owner patterns shaped in the survival stage do not automatically upgrade when revenue does. The instinct to protect cash that served you in year one can become the ceiling that limits you in year four. Behavioral finance research shows that loss aversion, the tendency for losses to feel roughly twice as painful as equivalent gains, causes founders to under-reinvest even when the numbers clearly support deployment.

Darren G. experienced this firsthand. He came to James carrying what felt like an invisible ceiling: a good salary, a stable career, yet completely blocked from the income growth and business ownership he genuinely wanted. Through James’s coaching process, he identified the subconscious goal blocks that were shaping every financial decision without his awareness. Once those patterns were exposed and cleared, his thinking, behaviors, and results shifted in ways that extended well beyond his finances. That pattern is more common among scaling founders than most would readily admit.

The decision to reinvest is not purely financial. It is an identity decision. Leaders who see themselves as builders reinvest. Leaders who still see themselves as survivors protect.

Where to Reinvest for Maximum Return at the Scaling Stage

Not all reinvestment delivers equal return. At the scaling stage, three categories consistently produce the highest ROI.

People First

Hiring before you feel completely ready is one of the most consistently high-return investments a scaling business can make. The right hire in a revenue-generating role, or in an operational capacity that frees the founder to focus on growth, often pays back within six to twelve months. The key is filling gaps that are actively constraining output, not simply adding headcount. For a structured approach to aligning hiring decisions with measurable outcomes, these smart reinvestment strategies offer practical frameworks for Canadian businesses.

Systems and Automation

Manual processes do not scale. At the startup phase, a founder managing everything manually is resourceful. At the scaling phase, the same behaviour creates bottlenecks that compound with volume. Investing in financial automation, CRM tools, and operational systems reduces overhead and creates the data visibility needed for confident reinvestment decisions. According to the CWB study, 42% of Canadian SMEs in key industries still rely on manual processes for cash flow management, a significant efficiency gap that targeted reinvestment can close.

Market and Growth Channels

Reinvesting in channels that are already producing through deeper marketing spend, expanded sales capacity, or geographic reach carries lower risk than building new channels from scratch. For goal-setting frameworks that tie reinvestment directly to revenue targets, this guide on goal-setting for business growth provides a structured starting point.

Canadian Tax Levers That Multiply Your Reinvestment Power

Canada has become significantly more tax-efficient for R&D-intensive and capital-investing scaling businesses in 2026. Two federal programs in particular create leverage that most generic finance articles overlook and that most scaling founders underutilize.

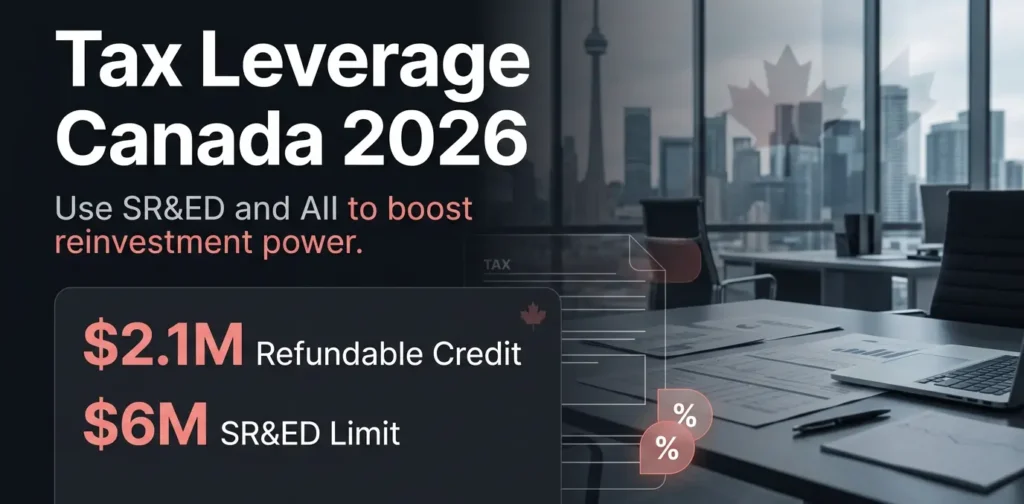

SR&ED Program: Now Worth Up to $2.1M Annually

The Scientific Research and Experimental Development (SR&ED) tax incentive is one of the most powerful reinvestment tools available to scaling Canadian businesses. Following the 2024 Fall Economic Statement and confirmed in Budget 2025 (Bill C-15, Royal Assent March 26, 2026), the annual SR&ED expenditure limit eligible for the enhanced 35% refundable investment tax credit increased from $3M to $6M for qualifying Canadian-controlled private corporations. According to KPMG Canada, eligible businesses can now claim up to $2.1M in refundable credits annually, double the previous ceiling, representing one of the largest expansions of the refundable SR&ED benefit since the program was created.

Capital expenditures have also been restored as eligible SR&ED claims for property acquired after December 15, 2024, reversing a policy shift from 2012 (PwC Canada, 2025). Additionally, as of April 1, 2026, the CRA launched a new pre-claim approval process for eligible businesses with annual gross income under $25M. The CRA provides a determination within eight weeks, allowing founders to confirm SR&ED eligibility before incurring any development costs.

Accelerated Investment Incentive (Reinstated to 2030)

The Accelerated Investment Incentive allows businesses to deduct capital expenses faster than standard CCA rates, improving cash flow in the year of purchase. According to PwC Canada, the AII has been fully reinstated with a gradual phase-out beginning after 2030. For scaling businesses investing in equipment, technology infrastructure, or leasehold improvements, this accelerated deduction can meaningfully reduce tax drag on capital reinvestment in the year it matters most.

Tax Remittance Timing and Cash Reserve Planning in Canada

Canadian incorporated businesses carry several remittance obligations that directly affect cash flow planning. GST/HST remittances for annual filers are due three months after the fiscal year-end; monthly filers remit within one month of each reporting period. Payroll source deductions are typically due on the 15th of the month following payroll processing for regular remitters. Corporate tax installments for CCPCs with a prior-year tax liability over $3,000 are generally due quarterly, and for rapidly scaling businesses, these installment amounts can increase faster than owners anticipate as revenue grows.

Missing any of these creates immediate CRA penalties and interest. Build these obligations as fixed line items in your monthly cash flow model, not as year-end surprises. Treating tax reserves as a separate, non-touchable allocation throughout the year is one of the simplest and highest-impact cash flow disciplines a scaling business can adopt.

The Cash Flow Metrics Canadian Founders Should Track Monthly

Most scaling businesses track revenue and net profit. The founders make consistently better reinvestment decisions, tracking six additional metrics that reveal what revenue alone cannot.

Operating Cash Flow Ratio

Calculated as operating cash flow divided by current liabilities. A ratio above 1.0 means your business generates enough cash from operations to cover near-term obligations without credit dependency. Below 1.0 signals structural vulnerability that should be resolved before increasing reinvestment rates.

Cash Conversion Cycle (CCC)

The CCC measures how long it takes to convert receivables and inventory into usable cash. Shorter cycles free up reinvestment capital faster and reduce dependence on credit lines. For Canadian service businesses, Accounts Receivable Days, the average time between invoicing and collection, is the primary variable to compress. Every day shortened is a day of capital freed for growth.

Payroll Runway

How many months of full payroll can your current cash reserves cover without new revenue? This metric is critical for scaling businesses, considering a tipping-point hire. A minimum payroll runway of two months before adding a significant headcount is a sound operational threshold. Below that, a new hire represents cash flow risk rather than growth investment.

Tax Reserve Ratio

The percentage of net profit actively held for upcoming CRA obligations, including income tax, GST/HST, and payroll source deductions. For most incorporated Canadian businesses, 25-30% of net profit should sit in a dedicated tax reserve account throughout the year. Treating this as a separate allocation prevents the common and costly mistake of spending tax obligations before they fall due.

Reinvestment ROI Payback Period

For every significant reinvestment decision, estimate the payback period: total investment divided by the expected monthly return it generates. People investments typically pay back in 6 to 18 months; technology investments in 3 to 12 months; established marketing channels in 1 to 6 months. Tracking estimated versus actual payback periods over time builds your organisation’s reinvestment intelligence and improves every future allocation decision. Additional ROI tracking frameworks are available in this guide to tracking ROI from reinvestment for scaling Canadian businesses.

Who Should Reinvest Aggressively?

Aggressive reinvestment of 50-70% of net profit is appropriate when your business has stable recurring revenue with strong margins, a proven and repeatable sales process, a cash buffer covering at least three months of operating expenses, and a specific growth initiative with a defined payback period. If all of these conditions are met, holding cash conservatively is not prudent. It is the cost of missed compounding.

Who Should Pull Back on Reinvestment Right Now?

Reduce your reinvestment rate if your business is experiencing seasonal revenue dips without adequate reserves, if payroll runway is below two months, if you are carrying high-interest debt with a rate exceeding your expected reinvestment return, or if your cash conversion cycle is lengthening. In these cases, strengthening reserves and reducing high-cost debt is itself a form of strategic reinvestment in your business’s resilience and future reinvestment capacity.

Data and Findings

The following sourced data points support the guidance in this article:

- 60% of Canadian SMEs report ongoing cash flow management challenges (Canadian Western Bank / Leger study, 2024, sample of 501 SME owners)

- 42% of Canadian SMEs in professional services, manufacturing, and agriculture still use manual cash flow processes (CWB, 2024)

- 50% of small businesses in Canada identify cash flow as a direct barrier to investment (Canadian Federation of Independent Business, via BOMCAS Canada, 2025)

- Scaling businesses reinvesting 30-50% of net profit consistently outperform conservative-reinvestment peers over 3-5 year horizons (Sandler Research, 2026)

- SR&ED refundable credits now available up to $2.1M annually for qualifying CCPCs, effective for tax years beginning December 16, 2024 (KPMG Canada, PwC Canada, DLA Piper confirmed in Bill C-15, March 2026)

- Loss aversion causes founders to underweight optimal reinvestment, with research from Tversky and Kahneman on prospect theory showing losses are weighted approximately twice as heavily as equivalent gains

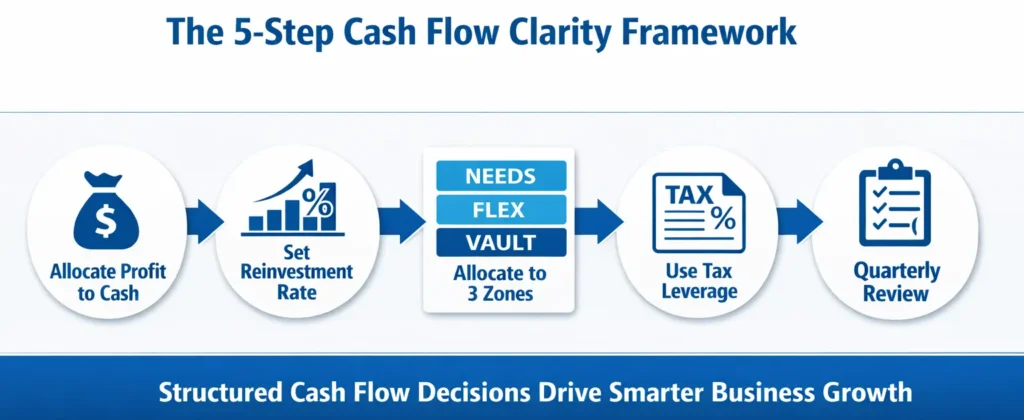

The 5-Step Cash Flow Clarity Framework

A structured approach prevents reinvestment decisions from being reactive or driven by short-term emotion.

Step 1: Separate profit from available cash.

Run a net profit calculation that accounts for all operating expenses, owner salary, debt obligations, and tax reserves. Do not plan reinvestment against revenue or gross profit. The only number that matters is deployable cash.

Step 2: Set your reinvestment rate by growth stage.

Use the tier benchmarks in the table above to establish a baseline percentage. Commit to it as a standing policy, not a decision made fresh each quarter. For a deeper look at stage-appropriate rates, this guide on how much profit a small business should retain covers the calculation model in detail.

Step 3: Allocate to three priority zones.

Every reinvestment dollar goes into one of three categories: people, systems, or market. Avoid unallocated reinvestment; it disappears into operating expenses without a trackable return.

Step 4: Activate Canadian tax leverage.

Before any significant capital reinvestment, evaluate SR&ED eligibility and Accelerated Investment Incentive applicability. Reducing tax drag on the same capital spend increases the effective return of every reinvestment dollar without requiring additional revenue.

Step 5: Review quarterly with a decision gate.

Each quarter, compare actual reinvestment ROI against your estimates. Adjust allocations based on what is producing results and what is not. This is your reinvestment intelligence loop and its value compounds over time.

Scenario-Based Decision Table

| Business Scenario | Recommended Reinvestment Approach |

| Stable recurring revenue + strong margins | Aggressive growth (50-70%) scale what is already working |

| Seasonal cash flow pattern | Conservative, reserve-first buffer before reinvesting |

| A hiring bottleneck is limiting output | People-first allocation highest near-term ROI at the scaling stage |

| Fulfillment or delivery delays | Systems and automation reduce operational friction first |

| High tax burden reduces available cash | Tax-efficient capex and SR&ED claim strategy before other reinvestment |

| High-interest debt above expected ROI | Debt reduction first, a guaranteed return beats a speculative one |

Ready to Deploy Your Cash Flow with Confidence?

Optimizing your cash flow is not just a financial discipline; it is a leadership one. The founders who build businesses that feel as strong on the inside as they appear on the outside are not those with the most revenue. They are the ones who have learned to see clearly, decide intentionally, and deploy capital with confidence rather than anxiety.

If you are at the scaling stage and feeling the friction between strong revenue and unclear reinvestment direction, that is not a cash problem. It is a clarity problem and it is solvable.

James works directly with Canadian entrepreneurs and business leaders who are ready to remove the internal blocks and build the systems that create lasting results. Book a complimentary strategy call and take the next step toward reinvesting with purpose.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.

Frequently Asked Questions

What is the right reinvestment rate for a scaling Canadian business?

Most scaling businesses between $500K and $5M in annual revenue perform best by reinvesting 30-50% of net profit. The exact percentage depends on your margin, growth stage, and cash buffer. Businesses with stable recurring revenue and a three-month reserve can generally reinvest more aggressively than those with seasonal or irregular cash inflows.

How is cash flow different from profit for reinvestment planning?

Profit is what your financial statements report after expenses. Cash flow reflects what is actually available in your account at any given moment. A profitable business can still face reinvestment constraints if receivables are slow, remittances are due, or debt service is consuming cash before it can be deployed for growth.

What Canadian tax programs support business reinvestment in 2026?

The SR&ED program offers refundable credits up to $2.1M annually for qualifying R&D expenditures, confirmed under Bill C-15 (Royal Assent March 26, 2026). The Accelerated Investment Incentive allows faster CCA deductions on capital purchases and has been reinstated until 2030. Both programs directly improve the after-tax return on reinvestment capital for CCPCs and qualifying Canadian corporations.

Which cash flow metrics matter most at the scaling stage?

Six metrics provide the clearest reinvestment signal: operating cash flow ratio, cash conversion cycle, accounts receivable days, payroll runway, tax reserve ratio, and reinvestment ROI payback period. Tracking these monthly creates the visibility needed for data-backed allocation decisions rather than reactive ones.

Why do scaling founders consistently under-reinvest even when cash flow supports it?

Behavioral finance research on loss aversion shows that losses register psychologically as roughly twice as painful as equivalent gains feel rewarding. The survival mindset that protected a business in early stages protects cash, avoids risk, and staying conservative can become an active ceiling at the growth stage. Structured decision frameworks and coaching help founders shift from reactive protection to intentional, evidence-based deployment.