Starting a business is exciting, but buying equipment can be a major financial hurdle. Whether it’s laptops, office furniture, machinery, or vehicles, these costs add up fast and can drain your cash flow before you even get started.

Equipment leasing offers a smarter alternative, giving you the tools you need for a fixed monthly fee instead of a massive upfront investment. This frees up cash for marketing, payroll, and growth while keeping your business financially flexible.

Key Takeaway:

- Equipment leasing allows startups to access essential tools, technology, vehicles, and machinery without the large upfront costs of purchasing. By spreading costs into predictable monthly payments, businesses can preserve cash flow for marketing, payroll, inventory, and growth initiatives. [1]

- Key benefits include lower startup costs, easier budgeting, access to newer equipment, potential tax advantages, reduced maintenance responsibilities, and the ability to keep business credit available for other financing needs. [1]

- Startups can choose from several lease structures, including operating leases for short-term flexibility, capital leases for eventual ownership, and leaseback agreements that unlock cash from existing assets. Selecting the right lease depends on equipment lifespan, upgrade needs, and long-term business goals. [2]

- To maximize value, businesses should lease only revenue-generating equipment, compare multiple providers, review contract terms carefully, understand end-of-lease options, and align lease commitments with projected cash flow and growth plans. [3]

Bottom Line: Equipment leasing helps startups acquire the tools they need while protecting cash flow and financial flexibility. When paired with careful provider selection and strategic planning, leasing can accelerate growth, reduce financial strain, and help new businesses scale without large upfront investments.

- Source: Unleash Your Power – Equipment Leasing for Startups: How To Get The Tools You Need Without Breaking the Bank

- Source: Unleash Your Power – Canada Small Business Financing Loan (CSBFL)

- Source: Unleash Your Power – Smart Reinvestment Strategies for Startups

Many entrepreneurs assume they need to buy everything outright, but leasing can provide the same essential equipment at a fraction of the cost. Whether you’re launching a construction company, restaurant, photography studio, or e-commerce brand, leasing can help you get started without the financial strain.

In this guide, we’ll break down how equipment leasing works and why it might be the perfect solution for your startup.

Equipment Leasing for Startups

Equipment leasing allows startups to acquire essential business equipment without paying the full purchase price upfront. Instead of making a large capital investment, businesses pay fixed monthly amounts while preserving cash flow for growth, hiring, inventory, and marketing.

For many startups, leasing provides a cost-effective way to access technology, vehicles, machinery, and office equipment while maintaining financial flexibility.

Equipment Leasing at a Glance

| Key Factor | Details |

|---|---|

| Best For | Startups preserving cash flow |

| Upfront Cost | Low |

| Monthly Payments | Fixed |

| Ownership | Optional |

| Equipment Upgrades | Easier than buying |

| Common Lease Terms | 12–84 months |

| Suitable Industries | Construction, healthcare, retail, technology, hospitality |

What Is Equipment Leasing?

Equipment leasing is a business financing arrangement that allows companies to use equipment in exchange for fixed monthly payments instead of purchasing the equipment outright.

The leasing provider owns the equipment during the lease term while the business gains immediate access to the asset. At the end of the agreement, businesses can typically return the equipment, renew the lease, or purchase the asset, depending on contract terms.

Startups commonly use equipment leasing to acquire technology, vehicles, machinery, office furniture, medical devices, and specialized equipment without making large upfront investments.

Equipment Leasing vs Buying

| Factor | Leasing | Buying |

|---|---|---|

| Upfront Cost | Lower | Higher |

| Ownership | Optional | Immediate |

| Cash Flow Impact | Lower | Higher |

| Upgrade Flexibility | High | Low |

| Maintenance Coverage | Often Included | Business Pays |

| Risk of Obsolescence | Lower | Higher |

Why Equipment Leasing Matters for Startups

Cash flow is often one of the biggest challenges facing new businesses. Large equipment purchases can consume capital that would otherwise be used for hiring, inventory, marketing, product development, or customer acquisition.

Equipment leasing helps startups preserve working capital while still accessing the tools needed to operate and grow. This allows founders to scale more efficiently without delaying critical business investments.

Why Startups Should Consider Leasing Instead of Buying

New businesses need cash flow to survive. Tying up thousands of dollars in equipment can limit your ability to cover marketing, payroll, and other growth expenses. Leasing offers a smarter alternative; you get the tools you need while keeping cash in your pocket. Here’s why leasing is a game-changer for startups:

Low Upfront Costs

Buying business equipment, whether it’s computers, industrial machinery, or vehicles, can cost hundreds of thousands of dollars. Leasing allows you to spread the cost over time, making it much easier to afford.

Easier Budgeting

Since leasing comes with fixed monthly payments, you always know how much you need to pay. This makes financial planning easier with no unexpected expenses and no surprise breakdown costs.

Access to the Latest Technology

Technology evolves fast. When you buy equipment, you’re stuck with it even when a newer, better model comes out. Leasing allows you to upgrade easily at the end of your contract, so your business always has cutting-edge tools.

Tax Benefits

Leasing payments are often tax-deductible as a business expense. This means you can write off your lease costs each year, reducing your taxable income. Always check with an accountant, but in many cases, leasing can save you money at tax time.

No Maintenance Headaches

When you own equipment, you’re responsible for repairs and maintenance, which can get expensive. Many leasing agreements include maintenance and servicing, so you don’t have to worry about costly breakdowns.

Preserves Business Credit

Since leasing doesn’t require a large loan, it keeps your credit lines open for other business needs. If you plan to apply for a business loan later, leasing ensures you still have borrowing power.

Why Businesses Use Equipment Leasing

Equipment financing and leasing have become common business funding strategies because they help organizations preserve capital while accessing essential operational assets.

According to industry research from the Equipment Leasing and Finance Association (ELFA), equipment leasing and financing remain widely used across industries because they support cash-flow management, technology upgrades, and business growth.

For startups, preserving capital during the early stages can improve flexibility and reduce dependence on additional debt.

Data & Findings

Equipment leasing is a widely used financing solution for Canadian businesses because it helps preserve cash flow while providing access to essential equipment. Rather than making a large upfront purchase, businesses can spread costs through predictable monthly payments and keep capital available for growth, hiring, inventory, and operations.

According to the National Bank of Canada, leasing can improve financial flexibility and make it easier for businesses to acquire equipment without significantly impacting working capital. This is especially valuable for startups and small businesses that need to manage cash flow carefully while scaling their operations.

Source: National Bank of Canada; Equipment Leasing Guide: https://www.nbc.ca/en/article/equipment-leasing-small-business.html, Canadian Equipment Financing; Benefits of Equipment Leasing

Should Your Startup Lease or Buy Equipment?

Leasing may be the better choice if:

- Cash flow is limited

- Equipment becomes outdated quickly

- You need flexibility

- Growth is the priority

- You want predictable monthly costs

Buying may be the better choice if:

- The equipment will be used for many years

- Ownership is strategically important

- The asset has strong resale value

- Long-term cost savings outweigh flexibility

What Type of Equipment Can You Lease?

Just about anything! Startups across all industries can benefit from equipment leasing. Here are some common examples:

Tech & Office Equipment

- Laptops & desktops

- Printers & scanners

- Office furniture

- Phone systems

- POS (Point-of-Sale) systems

Construction & Industrial Equipment

- Forklifts & cranes

- Excavators & bulldozers

- Power tools & generators

- Welding & manufacturing machines

Restaurant & Food Service

- Ovens & grills

- Refrigerators & freezers

- Coffee machines

- Dishwashers & prep stations

Retail & E-Commerce

- Display fixtures

- Security systems

- Warehouse shelving

- Packaging equipment

Medical & Healthcare

- X-ray machines

- Lab equipment

- Patient beds & exam tables

- Dental chairs & imaging devices

No matter what industry you’re in, leasing can help you access high-quality equipment without the upfront costs.

Types of Equipment Leasing: Which One Is Right for Your Startup?

Equipment Lease Types at a Glance

| Lease Type | Best For | Ownership Option | Flexibility |

|---|---|---|---|

| Operating Lease | Technology and short-term needs | No | High |

| Capital Lease | Long-term equipment use | Yes | Medium |

| Sale-Leaseback | Unlocking cash flow | No | Medium |

Choosing the right type of equipment lease can make a huge difference in your start-up’s growth, cash flow, and flexibility. Depending on your business needs, you may find that one lease option works better than another. Let’s dive into the three main types of equipment leasing and how they can benefit your business.

Operating Lease

An operating lease is a short-term lease where you rent equipment for a period shorter than its useful life. At the end of the lease, you return the equipment. This type of lease typically comes with lower monthly payments compared to a capital lease and doesn’t result in ownership.

Start-ups that need equipment temporarily or anticipate upgrading to newer models regularly will benefit most from an operating lease. This option offers maximum flexibility, allowing your business to avoid the burden of owning outdated or underused equipment.

Example: A tech start-up needs cutting-edge computers and software for a short-term project or an upcoming year but plans to upgrade in the near future. An operating lease allows them to stay current with the latest technology without committing to ownership.

Capital Lease

A capital lease is a long-term arrangement where the lease term covers a significant portion of the equipment’s useful life. The key difference from an operating lease is that at the end of the term, the business has the option (and often the obligation) to purchase the equipment, typically for a nominal fee.

Businesses that require equipment for a long-term investment will benefit most from a capital lease. It’s ideal if your start-up plans to use the equipment for several years and would prefer ownership at the end of the lease.

Example: A construction company leases heavy machinery like bulldozers or cranes on a capital lease, using the equipment for years. By the end of the lease term, the company can buy the equipment for a fraction of its value, making it a long-term asset for the business.

Leaseback Agreements

A leaseback agreement involves a start-up selling its existing equipment to a leasing company and then leasing it back. This unique type of lease offers immediate capital by turning your owned equipment into liquid assets, all while still allowing you to use the equipment in your operations.

If your start-up needs quick cash flow but still wants to retain the use of your equipment, a leaseback agreement can be an excellent option. It’s perfect for businesses that own valuable assets but need to free up funds for other business operations or growth initiatives.

Example: A manufacturing start-up owns high-value machinery but needs additional capital to expand its workforce. By entering a leaseback agreement, they sell the equipment to a leasing company, immediately receiving cash, while continuing to use the machinery in day-to-day operations.

When deciding between different equipment lease types, consider your business needs and long-term goals.

Real-World Example: Equipment Leasing for a Landscaping Startup

A landscaping startup requires the following equipment:

| Equipment | Estimated Cost |

|---|---|

| Commercial Truck | $45,000 |

| Trailer | $8,000 |

| Commercial Mower | $15,000 |

| Equipment Package | $12,000 |

Total upfront purchase cost: $80,000

Instead of spending $80,000 immediately, the business leases the equipment and preserves working capital for marketing, payroll, fuel, insurance, and customer acquisition.

The result is faster market entry without significantly reducing available cash reserves.

How Equipment Leasing Works: A Step-by-Step Guide

Starting the leasing process is easier than you think. Here’s how it works:

Step 1: Determine What You Need

Before you start shopping for leasing options, make a list of the essential equipment your business requires. Consider:

- What equipment is necessary to run your business smoothly?

- How long will you need it? Some equipment may only be needed short-term, while others will be part of your operations for years.

- Will you need to upgrade frequently? Technology changes fast, and leasing makes it easier to stay current.

- How will this equipment impact your business growth? Focus on equipment that boosts productivity or revenue.

Example: A restaurant owner might need commercial ovens, refrigerators, and espresso machines, while a digital marketing agency may prioritize high-performance computers and software.

Step 2: Research Leasing Companies

Not all leasing companies are the same. Some specialize in specific industries, while others offer more flexible terms. Finding the right provider ensures you get the best deal and avoid hidden costs.

What to Look for in a Leasing Company:

- Industry expertise: Some leasing companies specialize in medical, restaurant, or construction equipment. Choose one that understands your field.

- Competitive pricing: Compare interest rates and lease terms to find the best offer.

- Flexible contract terms: Look for options like early buyout clauses, upgrade flexibility, and maintenance coverage.

- Customer support & reputation Read online reviews and check their Better Business Bureau (BBB) rating.

How to Evaluate Equipment Leasing Companies

When comparing leasing providers, consider:

- Interest rates and fees

- Industry expertise

- Contract flexibility

- Maintenance coverage

- Customer reviews

- Early buyout options

- End-of-lease terms

Comparing multiple providers can help reduce costs and improve lease flexibility.

Step 3: Compare Lease Options

There are two main types of leases, each suited to different business needs. Understanding the differences helps you choose the right fit for your company.

Operating Lease (Best for Short-Term Use & Frequent Upgrades)

- Lower monthly payments.

- The leasing company retains ownership.

- You return the equipment at the end of the lease. Ideal for businesses that need to upgrade regularly (e.g., tech, medical, or creative industries).

Example: A graphic design agency leases high-end computers and design software for two years. Instead of owning outdated equipment, they upgrade to the latest models when the lease ends.

Finance Lease (Best for Long-Term Use & Ownership)

- Higher monthly payments.

- The business owns the equipment at the end of the lease.

- Best for long-term investments in essential equipment (e.g., construction machinery, restaurant ovens, trucks).

Example: A construction company leases bulldozers and forklifts under a finance lease. After five years, they own the equipment for a fraction of its original cost.

Step 4: Submit an Application

Once you choose a leasing provider and lease type, you’ll need to apply for approval. Each company has different requirements, but most will ask for:

- A Business plan or financial projections: help the lender understand your growth potential and ability to make payments.

- Credit history (personal or business): Strong credit improves approval chances and secures better terms. Startups with no credit may need a personal guarantee.

- Proof of business registration: shows your company is legally established.

Pro Tip: If your startup has a limited credit history, consider working with a leasing company that specializes in new businesses or offers lower-credit financing options.

Step 5: Get Approved & Sign the Agreement

Once approved, review the contract carefully before signing. Leasing agreements can include hidden fees or strict terms that may not benefit your business.

Key Terms to Pay Attention To:

- Lease Length: How long is the lease term? Does it align with your business plan?

- Monthly Costs: Understand the breakdown of payments, including any fees or taxes.

- Maintenance Responsibilities: Some leases include maintenance, while others leave repairs up to you.

- End-of-Lease Options: Can you buy the equipment, renew the lease, or return it?

Pro Tip: If the contract is unclear or overly complex, have a business attorney review it before signing.

Step 6: Receive & Use Your Equipment

Once the lease is finalized, the provider delivers the equipment, and you can start using it immediately!

Common Mistakes to Avoid When Leasing Equipment

While leasing is a great option, it’s important to avoid these common pitfalls:

- Leasing unnecessary equipment: Don’t overextend yourself. Lease only what you need to start and grow your business.

- Ignoring the fine print: Always read the contract carefully. Check for hidden fees, early termination penalties, or required insurance policies.

- Not comparing multiple offers: Shop around! Some companies charge higher interest rates or have less flexible terms than others.

- Forgetting about the end-of-lease options: Will you upgrade, renew, or buy? Make sure you plan before the lease ends.

Equipment Leasing Pros and Cons

| Pros | Cons |

|---|---|

| Lower upfront costs | Can cost more over time |

| Better cash flow management | No immediate ownership |

| Easier upgrades | Early termination fees may apply |

| Predictable monthly payments | Usage restrictions may exist |

| Preserves credit lines | Long-term contracts |

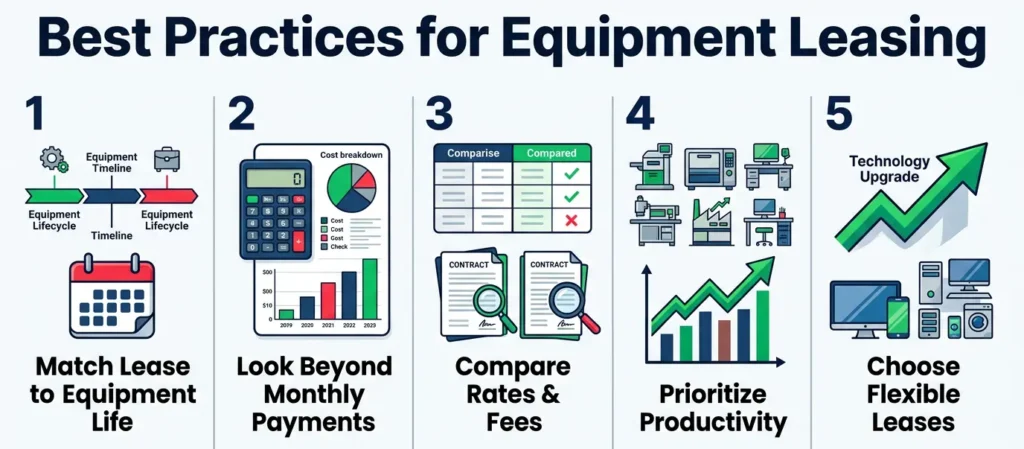

Best Practices for Equipment Leasing

Match Lease Length to Equipment Life

Avoid leasing equipment significantly longer than its expected useful life.

Understand Total Cost

Evaluate total lease expenses, not just monthly payments.

Compare Multiple Providers

Review rates, fees, maintenance obligations, and buyout options.

Prioritize Revenue-Generating Assets

Focus on equipment that directly improves productivity or generates revenue.

Review Upgrade Options

Businesses relying on technology should prioritize lease agreements that allow future upgrades.

Final Thoughts

Equipment leasing provides startups with access to essential tools while preserving valuable working capital. By replacing large upfront purchases with predictable monthly payments, businesses can improve cash flow, maintain financial flexibility, and invest more aggressively in growth initiatives.

The best leasing strategy depends on your equipment needs, growth plans, and long-term financial goals. Before signing any agreement, compare providers, understand total lease costs, and evaluate end-of-lease options.

For many startups, leasing offers a practical path to obtaining the equipment needed to compete, grow, and scale without placing unnecessary strain on cash reserves.

Frequently Asked Questions About Equipment Leasing for Businesses

Is equipment leasing better than buying for startups?

For many startups, equipment leasing is a better option because it requires less upfront capital and preserves cash flow for growth activities such as hiring, marketing, and inventory. Buying may be more cost-effective over the long term if the equipment will be used for many years and is unlikely to become obsolete.

Can a startup with no business credit qualify for equipment leasing?

Yes. Many leasing companies offer startup programs that consider the owner’s personal credit score, industry experience, business plan, and projected revenue. Some providers specialize in working with new businesses that have limited or no established business credit history.

What credit score is needed for equipment leasing?

Credit requirements vary by lender and equipment type, but many leasing providers prefer credit scores of 600 or higher. Businesses with stronger credit profiles typically qualify for lower rates, better terms, and larger leasing amounts.

What happens at the end of an equipment lease?

At the end of an equipment lease, businesses usually have three options: return the equipment, renew the lease, or purchase the equipment at an agreed-upon price. The available options depend on the lease structure and contract terms.

Is equipment leasing tax-deductible?

In many jurisdictions, lease payments may be treated as a deductible business expense, which can reduce taxable income. However, tax treatment varies based on location, lease type, and business structure, so consulting a qualified accountant is recommended.

What types of equipment can businesses lease?

Businesses can lease a wide range of equipment, including computers, office furniture, vehicles, construction machinery, manufacturing equipment, medical devices, restaurant equipment, warehouse systems, and point-of-sale technology. Leasing is available across most industries and business sizes.

How long do equipment leases typically last?

Equipment lease terms commonly range from 12 to 84 months, depending on the equipment’s value, expected lifespan, and the needs of the business. Technology equipment often has shorter lease terms, while heavy machinery and vehicles may have longer agreements.