For Canadian side-hustlers and early-stage founders, passive income and active profit are not interchangeable, and choosing the wrong one at the wrong stage is one of the most expensive mistakes a founder can make. Active profit is income you earn through direct work: consulting, coaching, freelancing, or running a service business. The CRA taxes the first $500,000 of this at 9 to 12% through the Small Business Deduction.

Passive income, including dividends, rental income, and investment returns, faces tax rates approaching 50% inside a corporation. In 2026, the smarter path for most early-stage founders is to master active profit first, build capital and systems, then introduce passive income from a position of genuine strength.

Key Takeaway:

- In Canada, active profit (earned through direct work like consulting or freelancing) is taxed more favorably via the Small Business Deduction (9–12% on the first $500,000 in a CCPC), while passive income (rentals, dividends, investments) faces much higher taxes (up to 50%) and erodes the Small Business Deduction once it exceeds $50,000 annually. [1]

- Active profit offers faster results with lower upfront capital but is limited by time and energy; passive income provides scalability and eventual freedom but requires significant upfront effort/capital and carries higher tax drag plus burnout risk if started too early without a strong active foundation. [1]

- Follow the 3-Stage Income Architecture: Earn (build consistent active revenue first), Build (systematize and scale your active business), then Automate (add passive streams like digital products or investments); keep passive income under $50,000 initially to protect your Small Business Deduction and use TFSAs for tax-efficient investing. [2]

- Caveats: Most people fail at passive income because they skip the active foundation—67% of side-hustlers burn out and the median passive side income is only $200/month; passive is not truly “set and forget” early on; always consult a tax advisor for your specific situation in Canada. [2]

Bottom Line: In Canada, focus on building strong active profit first to take advantage of lower tax rates and create capital — then strategically add passive income streams. Chasing passive income too early often leads to higher taxes, burnout, and slower progress.

The Idea That Sounds Like Freedom and Acts Like a Trap

Most Canadian side-hustlers are not broke because they lack ideas. They are stuck because they are chasing the wrong type of income at the wrong stage.

Here is the number that should give you pause. Bankrate’s 2025 side hustle data puts the median monthly income from a side hustle at $200. Not $2,000. Not the $10,000 a month your social media feed keeps suggesting is normal. Two hundred dollars. The average sits higher at $885, but the median is the honest number. It tells you what most people are actually earning while they wait for their passive streams to mature.

That gap between the average and the median is not a mystery. It reflects a single mistake playing out at scale: chasing passive income before building a proven active income foundation. This article cuts through the noise and gives you a framework for sequencing your income so that the passive streams you eventually build actually have something to stand on.

What Is the Real Difference Between Passive Income and Active Profit in Canada?

Active profit is money you earn through direct, ongoing effort. When you stop working, it stops arriving. Consulting, coaching, freelancing, and any business where your skills drive the revenue all fall here.

Passive income generates returns after an upfront investment of time or capital, with less direct involvement once the system is running. Dividend stocks, rental properties, digital product sales, and investment portfolios are common examples. Even the most credible financial voices in 2026 describe this as “set-and-optimize” income, not hands-off income. The work shifts rather than disappears.

The word “after” is where most founders get tripped up. Every passive income stream requires either significant capital or significant front-loaded effort before it produces anything worth talking about. For an early-stage founder without both in place, that starting point is further away than the content makes it look.

How Does the CRA Actually Tax Passive Income for Canadian Entrepreneurs?

The tax difference between active and passive income in Canada is not a rounding error. It is the kind of gap that changes a business plan entirely.

The first $500,000 of active business income earned by a Canadian-controlled private corporation qualifies for the Small Business Deduction. Depending on your province, that brings your effective corporate tax rate down to between 9% and 12%. A meaningful advantage designed to help small businesses reinvest and grow.

Passive income earned inside a corporation is taxed at a rate approaching 50%. The CRA classifies it as Adjusted Aggregate Investment Income and applies a much higher rate to prevent business owners from using their corporations as personal investment shelters.

There is also a threshold that most founders learn about too late. Once your corporation earns more than $50,000 in passive income in a given year, the Small Business Deduction begins eroding. By the time passive income hits $150,000, the deduction is gone entirely, and your active income gets taxed at the general corporate rate of around 27%. A passive income stream that looks like progress on paper can quietly cost you tens of thousands in lost deductions.

Quick reference: Active business income for a CCPC: 9 to 12% tax rate on the first $500K. Passive income inside the same corporation: up to 50%. That is not a small difference.

The Passive Income Myths That Keep Canadian Founders Stuck

Myth 1: You can start building passive income without capital or an existing audience.

Every sustainable passive income stream is either capital-intensive or time-intensive to build. Dividend investing requires capital you have to earn first. Digital products require an audience you have to build first. Real estate in most Canadian markets requires a down payment that does not materialise from thin air. The shortcut people are hunting for does not exist. What exists is a front-loaded investment that eventually pays off, on a timeline that is almost always longer than the content suggests.

Myth 2: Once it is set up, it runs itself.

The word “passive” is doing a lot of work it cannot back up. A course that sells overnight still needs marketing, updates, and customer support. A rental property still needs to be managed. An investment portfolio still needs to be reviewed. The work shifts from daily to periodic, but it does not disappear. Most founders underestimate how much setup and maintenance is involved, which is why so many passive income projects quietly stall after the initial push fades.

Myth 3: Passive income is always the smarter tax play.

As the CRA rules above show, passive income inside a corporation is taxed at nearly 50% and can erode your Small Business Deduction once it crosses $50,000 per year. That is not a tax advantage. Understanding how the CRA classifies income types is one of the most important financial decisions a Canadian founder can make, and this particular myth is one of the costliest to act on without that knowledge in place.

Is Passive Income Worth Pursuing at the Early Stage?

For most early-stage founders, passive income is the right destination and the wrong starting point. The reasons most small businesses stop growing almost always trace back to one thing: trying to do too many things before one thing is working.

The $200 median tells a clear story. The founders below that number are typically building passive systems before they have mastered active profit. They are creating digital products for audiences they have not built yet. They are launching affiliate sites with no content strategy. They are waiting for returns from systems they set up and then left alone.

The founders above that number, and the more than 25% of Canadian side-hustlers earning over $10,000 per year, have almost always done one thing first: mastered a single active income stream, built consistent clients, and used that capital and credibility to layer in passive income later.

Passive income without a proven active foundation is like building the penthouse before you have poured the concrete. The vision is sound. The sequence is off.

Darren came to James R. Elliot financially frustrated and stuck. A solid job, but no way through to the income and business ownership he wanted, no matter how much effort he put in. James helped him identify the goal blocks and limiting beliefs keeping him locked in an active income ceiling. Once those were shifted, Darren stopped chasing passive shortcuts and built from a foundation of proven active profit first. The results carried across his career, his income, and his relationships.

Try this: Write down every income stream you are currently pursuing or planning. Put a date next to each one showing when it last produced a dollar. If most are blank, you are spreading effort across systems with no foundation yet. Pick the one with the most traction and go all in on that first.

What Does the Active-to-Passive Transition Actually Look Like?

Founders who build durable income do not skip stages. They work through them in order. Before you start, a clear goal-setting strategy for business growth gives each stage a measurable target so you know exactly when you are ready to move forward.

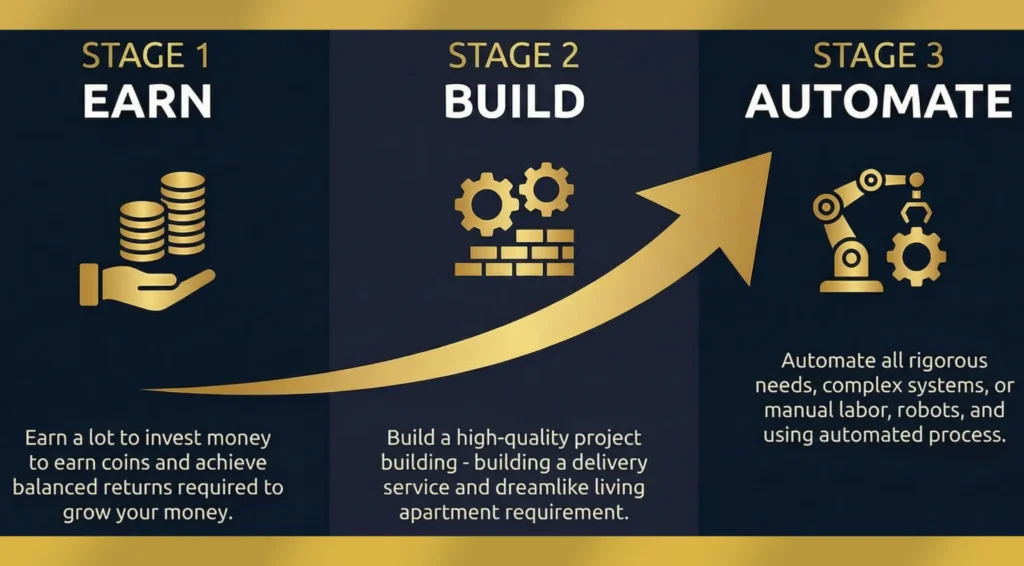

The 3-Stage Income Architecture

After 20+ years of working with founders and side-hustlers, one pattern shows up without fail. The people who build income that actually scales do not try to skip the stages that make it possible.

Stage 1: Earn

Pick one active income stream and get good at it. The goal here is repeatable, consistent monthly revenue from a single skill or service. Not two ideas, not three platforms. One thing, done well enough that people keep paying for it. Do not move forward until you are hitting a revenue target you have set for yourself, consistently, for at least 90 days.

Try this: Set a monthly revenue target for your core offer. Track it for 90 days straight. If you miss it, stay in Stage 1 and find out why. Discipline at this stage is what makes Stages 2 and 3 possible.

Stage 2: Build

Systematize what is working. Write down how you get clients, how you deliver results, and how you follow up. Raise your prices based on the results you have already demonstrated. Start handing off the tasks that do not need your direct expertise. This is where smart reinvestment strategies compound your active income and build the capital that funds Stage 3.

Stage 3: Automate

Now you introduce passive income, backed by Stage 1 proof and Stage 2 capital. You know what works. You have money to put to work. Your business no longer depends entirely on your daily presence. Dividend ETFs inside a TFSA, digital products backed by a real audience, investment vehicles that fit your tax profile. These all make sense at Stage 3. Not before.

Founders who skip straight to Stage 3 without the foundation almost always end up burned out, in debt, or months into projects that have never earned a dollar. If you have been wondering whether you are spreading yourself too thin across income sources, the answer is probably yes. The fix is almost always returning to Stage 1 and doing it properly.

The entrepreneurial mindset shift that separates founders who break through from those who stay stuck is this: they stop treating passive income as a starting point and start treating it as something you earn the right to build.

Who Should Focus on This Approach?

This framework fits you if any of these are true:

- You are generating active income from a skill or service but feel like the only way to grow is to work more hours.

- You have been chasing passive income for months with little to show for it and are starting to think the sequence might be the problem.

- You have a service business with repeatable results and want to use those results as the foundation for something that scales.

- You want income that holds up across economic shifts and does not depend on a single platform, algorithm, or client.

Who Should Hold Off on Passive Income Right Now?

Passive income strategies can wait if any of the following apply:

- You have not validated a single active income source yet. Proof of concept comes first. Someone has to be willing to pay you for something before any other conversation matters.

- You are already spread across too many income streams with none of them producing consistent results. Adding a passive layer to scattered active income deepens the problem rather than fixing it.

- Your active income is not covering your core expenses yet. Building passive income while running a deficit is not a strategy. It leads to exhaustion and makes the underlying problem harder to solve.

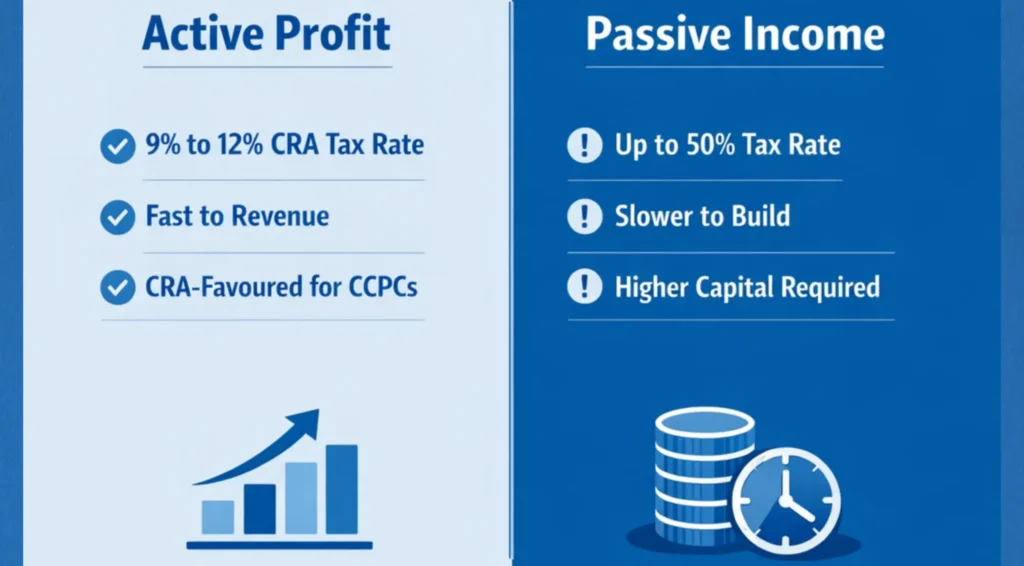

Active Profit vs. Passive Income: Side-by-Side

For most Canadian side-hustlers and early-stage founders, active profit is the right starting point. Faster results, better tax treatment under the Small Business Deduction, and the capital base needed to eventually build passive income that holds up.

| Factor | Active Profit | Passive Income |

|---|---|---|

| CRA Tax Rate (CCPC) | 9-12% via Small Business Deduction | Up to 50% (Adjusted Aggregate Investment Income) |

| Time to First Dollar | Days to weeks | Months to years |

| Upfront Capital | Low to moderate | Moderate to high |

| Ongoing Effort | Active but predictable | Front-loaded, then lower maintenance |

| Burnout Risk | Moderate with clear boundaries | High without an active income foundation first |

| Scalability | Capped by hours until systematized | High once Stages 1 and 2 are complete |

| SBD Erosion Risk | None at the early stage | Starts above $50K passive income per year |

| Recommended Stage | Stage 1: All early-stage founders | Stage 3: After active income is proven and stable |

Data and Findings

The CRA taxes active business income for Canadian-controlled private corporations at 9 to 12% on the first $500,000 through the Small Business Deduction. Passive income inside the same corporation faces rates approaching 50%.

Once corporate passive income crosses $50,000 in a fiscal year, the Small Business Deduction starts to erode. At $150,000, it disappears entirely, pushing active income up to the general corporate tax rate of approximately 27%.

Bankrate’s 2025 data shows average monthly side hustle income at $885, while the median sits at $200. That spread reflects the difference between founders who built a proven active income base first and those who tried to bypass that stage.

67% of side-hustlers report burnout. The most common cause is splitting effort across multiple income streams before any one of them has reached consistent revenue.

Among founders who worked through James R. Elliot’s business coaching program, those who sequenced their income correctly, mastering active profit before introducing passive streams, built more durable businesses and reported significantly lower burnout along the way.

The Bottom Line

Passive income is not a bad idea. Getting the sequence wrong is.

When you understand the real tax implications, what most side-hustlers are actually earning, and how the founders who break through build their income, the path forward gets clear. Master active profit first. Build the systems. Then layer in passive income from a position of strength, not from a position of hoping something sticks.

That is not a slower path. It is the one that actually gets you somewhere.

Once you see your situation clearly, the real question becomes: what should you be focused on right now? If you are ready to stop guessing and start building with a real strategy behind you, that is exactly what James R. Elliot’s business coaching program is built for. Book a call and let’s map out your next stage.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.

Frequently Asked Questions

Is passive income taxed differently from active income in Canada?

Yes, by a significant margin. Active business income for a Canadian-controlled private corporation benefits from the Small Business Deduction, which drops the effective corporate tax rate to 9 to 12% on the first $500,000. Passive income inside the same corporation is taxed at rates approaching 50%. For early-stage founders without significant capital to deploy, active income is the far more tax-efficient starting point.

How much capital do I need before I can build passive income in Canada?

It depends on the stream. Dividend ETFs inside a TFSA can be started with regular small contributions. Rental property in most Canadian markets requires a substantial down payment. Digital products require audience-building first, which is a time investment before it becomes a financial one. Most founders underestimate both the upfront requirements and the realistic timeline, regardless of which route they choose.

What is the fastest way to build passive income as a Canadian entrepreneur?

The closest thing to fast is selling a digital product or service to an audience that already trusts you, because the existing relationship does the heavy lifting. Without that foundation, most passive income streams take 12 to 24 months of consistent effort before producing meaningful monthly returns. Anyone selling a faster timeline than that is selling a myth.

Can earning too much passive income cost me my Small Business Deduction?

Yes. Once your corporation earns more than $50,000 in passive income in a fiscal year, the Small Business Deduction begins to phase out. It disappears entirely at $150,000 in passive income, at which point your active income is taxed at the general corporate rate of approximately 27%. This is a critical planning consideration for any founder thinking about passive income inside a corporation, and one worth discussing with a qualified accountant before you structure anything.

How do I know when I am actually ready to move from active to passive income?

Three conditions: your active income is consistent month over month, your core business processes are documented and no longer fully dependent on your daily involvement, and you have capital available to invest without touching your operating cash flow. If any of those three are not in place, you are still in Stage 1 or Stage 2. Stay there, do the work, and move forward when the foundation is real.