Asset protection for Canadian entrepreneurs means legally separating your personal wealth from your business’s liabilities before a lawsuit, creditor claim, or failed venture can reach your house, savings, or personal assets.

The core tools available to new Canadian founders include incorporation as a Canadian-Controlled Private Corporation (CCPC), strict separation of business and personal finances, business liability insurance, a holding company (Holdco) structure for surplus profits, and awareness of the Lifetime Capital Gains Exemption (LCGE).

These strategies work best when implemented early. Once a legal claim is already in motion, options narrow fast.

Key Takeaway:

- Asset protection is essential for Canadian entrepreneurs as business risks are rising (70% faced legal disputes recently). The foundation is incorporating as a Canadian-Controlled Private Corporation (CCPC) to create legal separation between personal and business assets, while enjoying low tax rates (as low as 9-12.2% on the first $500,000 of active income). [1]

- Key mechanisms include maintaining strict financial separation (dedicated business bank account and credit card, no commingling) to prevent “piercing the corporate veil,” obtaining proper insurance (general liability, professional liability, D&O), and using a holding company (Holdco) to protect surplus profits and investments from operating company creditors. [1]

- Protect your future sale with the Lifetime Capital Gains Exemption (up to $1.25M tax-free) by keeping 90% of assets active in the business and holding shares for at least 24 months. Implement early—ideally in the first 1–3 years—before problems arise, using the 5-step Canadian Asset Shield framework. [2]

- Avoid common pitfalls: personal guarantees on loans, mixing personal/business finances, delaying incorporation, or leaving too much retained earnings in the operating company. Always consult a lawyer and CPA for setup and ongoing compliance. [2]

Bottom Line: Proactive asset protection through early incorporation as a CCPC, financial firewalls, insurance, a Holdco for surplus, and LCGE planning is one of the smartest moves Canadian entrepreneurs can make to safeguard personal wealth from business risks—start now before it’s too late.

You Incorporated: You’re Still Not as Protected as You Think

You registered your corporation. You’ve got a business bank account. You feel like the hard part is done.

Then your bank asks for a personal guarantee on your credit line, and suddenly your house is back on the line. Or a client threatens legal action over a deliverable dispute, and you realize your corporate structure won’t protect you as cleanly as you assumed. Or you accumulate two years of retained earnings inside your operating company, completely unaware that they’re sitting exposed to any creditor who comes knocking.

This is where most new Canadian entrepreneurs are right now. Not unprotected exactly, but not properly shielded either.

According to a 2023 ARAG Legal Solutions study, seven out of ten Canadian small businesses dealt with at least one legal dispute in the previous three years. That’s a 230% increase since 2015. More than half of those owners said the dispute had a large or moderate financial impact on their operation.

Asset protection isn’t a topic for when you’re wealthy. It’s a topic for right now, in years one through three, while the cost of setting up the right asset protection strategies for Canadian entrepreneurs is still low and no one is at your door yet.

What Is Asset Protection for Canadian Entrepreneurs?

Asset protection for Canadian entrepreneurs is the legal and financial practice of separating personal wealth from business liabilities so that lawsuits, creditor claims, or business failures cannot reach personal assets such as a home, savings account, or personal investments. It involves using structures like incorporation, holding companies, and insurance to create enforceable legal boundaries between the person and the business. In Canada, the most common and accessible tools are the Canadian-Controlled Private Corporation (CCPC), the holding company (Holdco), and business liability insurance.

What Asset Protection Really Means for New Canadian Entrepreneurs

Asset protection is the practice of legally organizing your business and personal finances so that your personal wealth, your home, savings, investments, and other assets are separated from your business’s risks.

When you operate as a sole proprietor, there is no legal line between you and your business. If your business gets sued, you get sued. If your business can’t pay a debt, creditors can pursue your personal bank account.

The goal of implementing asset protection strategies for Canadian entrepreneurs is to create layers between your personal life and your business operations. Each layer adds time, complexity, and legal friction that protects your personal wealth when things go wrong. None of this is about hiding money or avoiding taxes. It’s about building a structure that reflects the actual risks you’re taking as a founder.

To put it simply: a sole proprietorship offers no legal separation between you and your business, a CCPC creates a distinct legal entity that shields personal assets from most business liabilities, and a CCPC paired with a Holdco adds an additional layer of creditor protection and tax-efficient asset management on top.

Why Incorporation Is the First Line of Defence

For most new Canadian entrepreneurs, incorporating is the single most important first step in protecting personal assets. When you incorporate, your business becomes a separate legal entity. That corporation can enter into contracts, take on debt, and be sued, and in most cases, your personal assets are not directly on the line.

A Canadian-Controlled Private Corporation (CCPC) also gives you access to the Small Business Deduction, which reduces your federal corporate tax rate from 28% to 9% on the first $500,000 of active business income. In Ontario, the combined federal and provincial rate drops to as low as 12.2% on that income. That’s roughly half the tax rate of operating as a sole proprietor. More money stays in the business, and more money protected inside a corporation is harder for creditors to reach. Our guide on why small businesses fail to grow in Canada covers why structural decisions made early have outsized effects on long-term outcomes.

The Personal Guarantee Problem

Here’s what incorporation does not protect you from: personal guarantees.

When banks, commercial landlords, or suppliers extend credit to a new corporation, they often require the business owner to personally guarantee the debt. That means if the corporation can’t pay, they come after you personally, regardless of your corporate structure.

This is one of the most common exposure points for new Canadian entrepreneurs, and it catches founders off guard because they believe incorporation fully shields them. It doesn’t shield you from obligations you’ve personally signed. Know what you’re signing before you sign it, and build your protection layers in every other area so personal guarantees are the exception, not the rule.

The Personal-Business Firewall: Why It Matters More Than You Think

Incorporation creates a legal wall between you and your business. But that wall only holds if you treat it like one.

Commingling personal and business finances is one of the most common mistakes new Canadian founders make. Courts can apply a legal doctrine known as “piercing the corporate veil” when business owners routinely blur the line between personal and corporate funds. When that happens, your liability protection can be stripped away, and creditors can reach your personal assets even though you incorporated.

The rules are simple but easy to neglect when you’re busy building something:

- Open a dedicated business bank account and keep it completely separate from your personal account

- Use a business credit card exclusively for business expenses

- Pay yourself a salary or dividends through proper bookkeeping, not informal transfers

- Keep meticulous records of all business transactions

- Never pay personal expenses from the business account, even temporarily

If you’re still working out which banking setup makes the most sense for your stage, see our guide to bank accounts for Canadian startups.

Asset Protection Mistakes That Expose New Canadian Entrepreneurs

Most asset protection breakdowns happen not because founders made a deliberate bad decision, but because they assumed protection existed where it didn’t.

- Staying as a sole proprietor too long: Operating without incorporation means zero legal separation between you and your business. Every lawsuit is a personal lawsuit.

- Mixing personal and business finances: This can invalidate your corporate protection entirely through the “piercing the corporate veil” doctrine.

- Signing personal guarantees without understanding them: Many founders sign these reflexively without knowing they’ve re-exposed their personal assets.

- Skipping business insurance: Incorporation limits liability for some risks but not all. Gaps in coverage can be expensive.

- Leaving retained earnings in the operating company: Profits you don’t need for operations are better swept into a Holdco, where they’re out of reach of creditors.

- Waiting until there’s a problem: Courts look at timing. A trust or Holdco established after a dispute is already brewing carries much less legal weight.

What Is a Holding Company and Do You Need One?

A holding company (Holdco) is a separate corporation that exists to own assets, not to run the day-to-day business. Your operating company (Opco) is where revenue comes in and expenses go out. The Holdco sits above it, holding surplus cash, investments, real estate, or shares of the Opco itself.

The core protection benefit is straightforward. If your Opco faces a lawsuit, only the assets inside the Opco are at risk. Cash and investments you’ve moved into the Holdco through tax-free intercorporate dividends are legally separate and out of reach.

A Holdco also keeps your operating company’s assets clean and primarily active, which protects your eligibility for the Lifetime Capital Gains Exemption covered in the next section.

When Does a Holdco Make Sense?

A Holdco is generally worth the additional cost and administrative complexity when your corporation is consistently generating more profit than you need for operations or personal income. A commonly cited threshold is around $50,000 or more in retained earnings that you don’t plan to withdraw personally in the short term.

At that point, the combination of creditor protection and tax deferral that a Holdco enables typically outweighs the setup cost, which generally runs between $2,500 and $4,000 in professional fees plus annual compliance costs.

For early-stage founders still building toward consistent profitability, getting the operating company structure right first is the priority. See our guide on smart reinvestment strategies for Canadian business owners for how to think about retained earnings and capital allocation in the early years.

Business Insurance: The Layer That Fills the Gaps

Incorporation and a Holdco structure protect you from many risks, but not all of them. Business insurance is the layer that covers what the corporate structure leaves exposed.

The coverage most new Canadian entrepreneurs need to evaluate:

- General Liability Insurance: Covers third-party claims for bodily injury, property damage, and some personal injury scenarios. This is foundational for most businesses.

- Professional Liability (Errors and Omissions): Essential for service-based businesses. Covers claims that your work caused a financial loss to a client.

- Business Interruption Insurance: Covers lost revenue when operations are disrupted by an insurable event.

- Directors and Officers (D&O) Insurance: Protects founders and executives personally from claims related to management decisions.

Review your coverage limits annually. The coverage that felt adequate in year one may leave significant gaps as your revenue and client base grow. Insurance premiums are almost always a fraction of the potential cost of an uninsured claim.

The LCGE: A Tax Shield You’re Building Right Now Without Knowing It

If you ever sell your business, the Lifetime Capital Gains Exemption (LCGE) can shelter up to $1.25 million in capital gains from taxation. As of 2026, that figure is $1,250,000 and is indexed to inflation going forward.

Here’s what makes this relevant for new founders: the clock on LCGE eligibility starts ticking from day one of your corporation’s existence. To qualify when you eventually sell, your business needs to meet several conditions, including:

- The corporation must qualify as a Canadian-Controlled Private Corporation (CCPC)

- At least 90% of the corporation’s assets must be used in an active business at the time of sale

- The shares being sold must have been owned by you for at least 24 months

That 90% active asset test is where retained earnings sitting inside your operating company can create a problem. If you’ve accumulated significant surplus cash or passive investments inside the Opco, they count against that threshold. This is one of the strongest structural reasons to sweep excess cash into a Holdco regularly, keeping your Opco clean so that when a buyer eventually comes, you qualify for the full exemption.

Data and Findings

Key Statistics on Canadian Entrepreneur Risk

- 70% of Canadian small businesses faced at least one legal dispute in the three years preceding 2023 a 230% increase from 2015 (ARAG Legal Solutions, 2023)

- 53% of business owners who faced legal disputes reported a large or moderate financial impact on their operation

- Approximately 21.5% of Canadian small businesses fail within their first year; roughly 50% don’t reach year five

- CCPC small business deduction reduces the federal corporate tax rate from 28% to 9% on the first $500,000 of active business income; the combined federal and Ontario rate can be as low as 12.2%

- The 2026 LCGE allows qualifying CCPC shareholders to shelter up to $1,250,000 in capital gains from taxation on a business sale

- Holdco setup typically costs $2,500 to $4,000 in professional fees; annual compliance adds cost but is generally far less than a single unprotected creditor event.

These numbers point to a clear pattern: legal risk isn’t rare for Canadian small businesses, it’s normal. Seven in ten founders will face a dispute. The difference between those who absorb it and those who are devastated by it almost always comes down to whether protection was built before the problem arrived. The strategies covered in this article aren’t advanced planning for large companies. They’re the baseline every new Canadian founder should have in place before revenue grows and the stakes get real.

The Canadian Asset Shield: A 5-Step Protection Framework for New Founders

In 20+ years of working with entrepreneurs, one thing stands out: the founders who build lasting businesses don’t just work harder, they build smarter structures underneath the work. Asset protection is one of those structures. Here’s a practical five-step framework you can apply at any stage.

Step 1: Incorporate as a CCPC Before Your Revenue Grows

Incorporation is the foundation. Without it, everything else is built on unstable ground. Set up your Canadian-Controlled Private Corporation early, before revenues scale, so the structure is in place when the risks start to matter. Work with a business lawyer in your province to handle this properly.

Step 2: Build the Personal-Business Firewall Immediately

The day your corporation exists, open a dedicated business bank account. Get a business credit card. Set up proper bookkeeping from day one. Discipline here protects your corporate veil and keeps your personal life legally separate from your business operations.

Step 3: Get the Right Insurance Coverage in Place

Assess your specific risk profile, including the nature of your work, your client contracts, and your physical assets, and build an insurance program that actually covers your exposure. Revisit this annually as the business grows.

Step 4: Sweep Surplus Profits into a Holdco as You Scale

Once you’re consistently generating retained earnings beyond your operating and personal needs, usually in the range of $50,000 or more, explore setting up a holding company. Work with a CPA experienced in corporate structures to move surplus cash out of the operating company tax-efficiently and into a protected vehicle.

Step 5: Protect Your LCGE Eligibility from Day One

Structure your corporation to maintain CCPC status, keep your operating company’s assets primarily active, and avoid letting passive investments accumulate inside the Opco. These habits, built early, can mean hundreds of thousands of dollars in tax savings when you eventually sell.

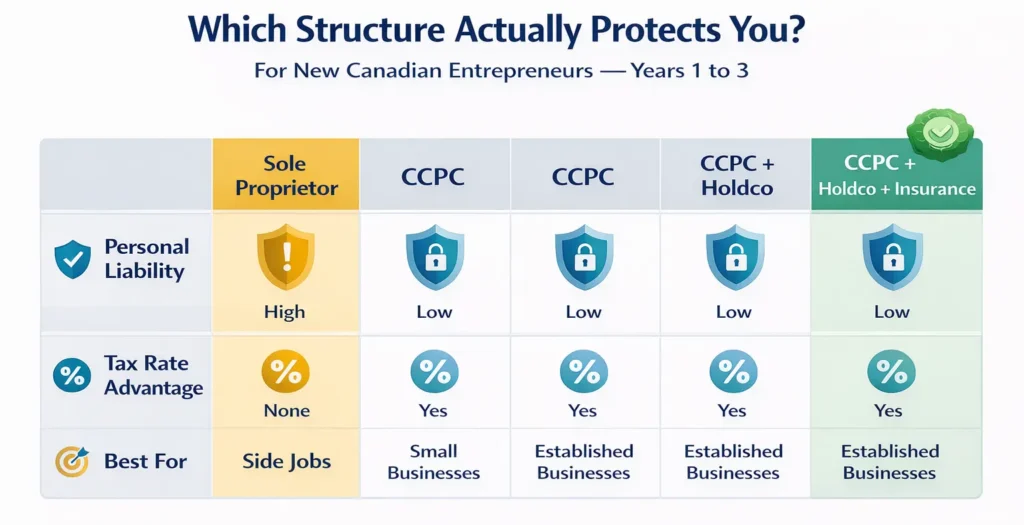

Business Structure Comparison for New Canadian Entrepreneurs

| Structure | Personal Liability | Tax Advantage | Best For |

| Sole Proprietor | Full personal exposure | None specific to structure | Testing an idea only |

| CCPC | Limited (corporate assets) | 9% federal rate on first $500K | Most new Canadian entrepreneurs |

| CCPC + Holdco | Strong creditor separation | Tax-free dividend sweep to Holdco | Founders with $50K+ retained earnings |

| CCPC + Holdco + Insurance | Most comprehensive | Full structural + coverage protection | Scaling businesses with real liability exposure |

Who Should Prioritize Asset Protection Strategies Right Now?

These strategies are urgent if you fit any of these descriptions:

- You’re operating as a sole proprietor with growing revenue and haven’t incorporated yet

- You’ve incorporated but are commingling personal and business funds

- You work in a field with real liability exposure: consulting, construction, professional services, healthcare-adjacent businesses, food and beverage, or product-based companies

- You’re signing commercial leases or taking on business debt that requires personal guarantees

- You’ve started generating consistent retained earnings, and you’re not withdrawing personally

Who Can Wait on More Advanced Structures?

If you’re still in the earliest stages of testing an idea, pre-revenue or generating very modest income, a full Holdco structure may be premature. Start with incorporation, open proper business banking, and get basic liability insurance. Those three steps alone put you ahead of most founders at your stage.

Build the advanced layers as your revenue and retained earnings grow. The structure should match the actual risks you’re carrying, not jump ahead of them.

Asset Protection Setup Checklist: Your First 30 Days

Most of the foundational work covered in this article can be started within your first month of operation. Use this as your action sequence:

- Week 1: Consult a corporate lawyer in your province and begin the incorporation process as a CCPC

- Week 1: Open a dedicated business bank account the day your corporation number is issued

- Week 2: Apply for a business credit card and establish your bookkeeping system; even a simple spreadsheet beats nothing

- Week 2: Review any contracts, leases, or loan agreements you’ve signed or are about to sign for personal guarantee clauses

- Week 3: Contact a commercial insurance broker and get quotes for general liability and professional liability coverage appropriate to your industry

- Week 4: Book a session with a CPA who works with incorporated owner-managers to map out your compensation structure and identify when a Holdco should enter the picture

None of these steps requires significant capital. Most require two to three hours of focused attention each. But taken together, they represent the core asset protection strategies every new Canadian entrepreneur should have locked in before revenue grows and the stakes get real.

Building a Business Is Hard Enough Without the Wrong Structure Underneath It

The difference between entrepreneurs who struggle through setbacks and those who build resilient, scalable businesses isn’t just effort. Its structure and decision-making clarity. The founders who come out ahead aren’t luckier; they’re better organized underneath the work where it’s harder to see.

The asset protection strategies covered in this article aren’t reserved for established companies or high-net-worth founders. They’re the baseline structure every new Canadian entrepreneur should have in place before revenue grows and real liability begins to accumulate.

If you want to build not just a protected business but one that performs at the highest level, working with a coach who understands both the structural and mindset dimensions of entrepreneurship makes a real difference. James R. Elliot’s business coaching program helps Canadian entrepreneurs make clearer decisions, remove the mental blocks that slow progress, and build businesses that are built to last.

You can also explore the entrepreneurial mindset principles through NLP that underpin the kind of decisive, clear-headed action that asset protection decisions require.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.

Frequently Asked Questions

Does incorporating protect all of my personal assets from business lawsuits?

Incorporation creates significant protection, but not absolute protection. Your personal assets are generally shielded from business debts and lawsuits filed against the corporation. However, personal guarantees you’ve signed, unpaid taxes, fraud, and, in some cases, director liability can still create personal exposure. Maintaining strict separation between personal and business finances is essential for the protection to hold.

When should a new Canadian entrepreneur set up a holding company?

A Holdco typically makes sense once your operating company is consistently generating retained earnings of roughly $50,000 or more that you’re not planning to withdraw personally in the short term. Below that threshold, the administrative cost and complexity of maintaining a second corporation often outweigh the benefits. Start with a well-structured CCPC, then add the Holdco as your profitability grows.

What is the Lifetime Capital Gains Exemption and does it apply to me?

The LCGE allows qualifying CCPC shareholders to shelter up to $1,250,000 in capital gains from taxation when selling their shares (2026 figure). To qualify, the shares must have been held for at least 24 months, the corporation must be a CCPC, and at least 90% of the corporation’s assets must be used in an active business at the time of sale. These conditions make it important to structure your corporation correctly from early on, particularly regarding where surplus cash and passive investments are held.

Can I set up asset protection structures after a legal dispute has started?

You can technically take protective steps at any time, but the effectiveness is significantly reduced once a dispute is underway. Courts can scrutinize transactions that appear designed to shield assets from a specific creditor. The strongest asset protection is built proactively, before any claim arises. Waiting until you’re facing legal action is one of the most common and costly mistakes Canadian entrepreneurs make.

Do I need a lawyer and an accountant to set up these structures?

For incorporation, you need a corporate lawyer or a well-reviewed online incorporation service, though a lawyer is strongly recommended for anything beyond the basics. For a Holdco structure, LCGE planning, or trust arrangements, you need a CPA with specific expertise in corporate tax planning. The cost of proper professional guidance is almost always a fraction of the cost of getting these structures wrong.