What are the exact tax rules for profitable businesses in Canada?

Canada’s most profitable businesses, consulting, coaching, real estate, and tech, are taxed under a dual-rate corporate structure. Canadian-Controlled Private Corporations (CCPCs) benefit from the Small Business Deduction (SBD), paying as little as 9% federal tax on the first $500,000 of active business income.

Combined with provincial rates, total tax on qualifying income typically lands between 9% and 13%, depending on the province. Income above that threshold is taxed at the general corporate rate, which ranges from 23% to 31% combined. Access to the SBD can be reduced by passive investment income and eliminated entirely if the business is classified as a Personal Services Business. Real estate income is treated as active or passive depending on the scale and nature of operations.

Key Takeaway:

- Profitable Canadian businesses must manage multiple tax obligations including corporate income tax, GST/HST, payroll deductions, and provincial taxes, with compliance requirements increasing as revenue grows. [1]

- Incorporated businesses can benefit from lower small business tax rates through the Small Business Deduction, allowing many Canadian-controlled private corporations (CCPCs) to pay reduced taxes on active business income. [2]

- Tax efficiency often depends on how owners pay themselves salary, dividends, or a combination with each approach affecting CPP contributions, personal taxes, and corporate deductions differently. [3]

- Businesses can legally reduce taxable income through eligible deductions such as home office expenses, vehicle use, software, salaries, professional services, marketing costs, and capital asset depreciation. [4]

- The most profitable businesses typically focus on proactive tax planning year-round rather than reacting at tax season, helping improve cash flow, reinvestment capacity, and long-term growth.

Bottom Line: Canadian business tax rules reward proactive planning. Businesses that understand deductions, corporate structures, and compensation strategies can improve cash flow, reduce unnecessary taxes, and retain more profit for long-term growth.

- Source: CRA – Corporation Income Tax Guide

- Source: CRA – Canadian Corporate Tax Rates and Small Business Deduction

- Source: BDO Canada – Salary vs Dividends

- Source: TurboTax Canada – Small Business Tax Deductions

For 2025 to 2026, the capital gains inclusion rate remains at 50%, and accelerated depreciation incentives allow qualifying businesses to write off assets up to three times faster in the first year. Profitable business owners must manage compensation, retained earnings, and corporate structure strategically to minimize total tax paid.

How Corporate Tax Works in Canada

Canada uses a dual-rate corporate tax system, and understanding it is the foundation of everything else in this guide. There are two core rates: a lower rate for qualifying small businesses and a general rate for everyone else.

The system is built around the concept of integration. The idea is that whether you earn income personally or through a corporation, the total tax paid should be roughly equal. In practice, the CCPC structure gives profitable business owners a meaningful window of tax deferral. Money left inside the corporation is taxed at the low corporate rate, and you only pay personal tax when you extract it as salary or dividends.

Active business income, money earned directly from your services or products, qualifies for the SBD. Passive income, like rental returns or investment gains held inside your corporation, is taxed at much higher rates. This one distinction determines whether you access the lowest corporate tax rates in Canada or not.

The Exact Corporate Tax Rates That Apply

The federal corporate tax rate starts at 38%, but most corporations never pay that. A 10% federal abatement reduces it to 28%, and the general rate reduction brings it further down to 15% for most businesses. CCPCs that qualify for the Small Business Deduction pay just 9% federally on income up to their business limit.

Provincial rates are added on top, and they vary meaningfully. In Ontario, the combined rate for a qualifying CCPC is approximately 12.2% on SBD income. Above the $500,000 threshold, combined federal and provincial rates rise to roughly 26.5% in Ontario, and up to 31% in some other provinces. Alberta tends to be lower; Quebec tends to be higher.

Province selection matters more than most business owners realize. If you are incorporated or planning to expand, understanding regional rate differences can meaningfully affect your bottom line, especially as you scale past the $500,000 mark.

Why the $500,000 Limit Is More Complicated Than It Looks

The $500,000 SBD limit applies across all associated corporations, not just one. If you own multiple businesses that the CRA considers “associated,” they share a single $500,000 limit. You do not get a fresh $500,000 per company, and this catches a lot of growing entrepreneurs completely off guard.

The Small Business Deduction: Your Most Powerful Tax Lever

The Small Business Deduction is the single most valuable tax tool available to Canadian business owners. The SBD reduces federal corporate tax from 15% to 9% on the first $500,000 of active business income for qualifying CCPCs. Most provinces offer a matching provincial SBD, bringing the combined rate to the 9% to 13% range.

To qualify, your business must be a Canadian-Controlled Private Corporation earning active business income in Canada. You cannot be a public company, a company controlled by non-residents, or a Personal Services Business.

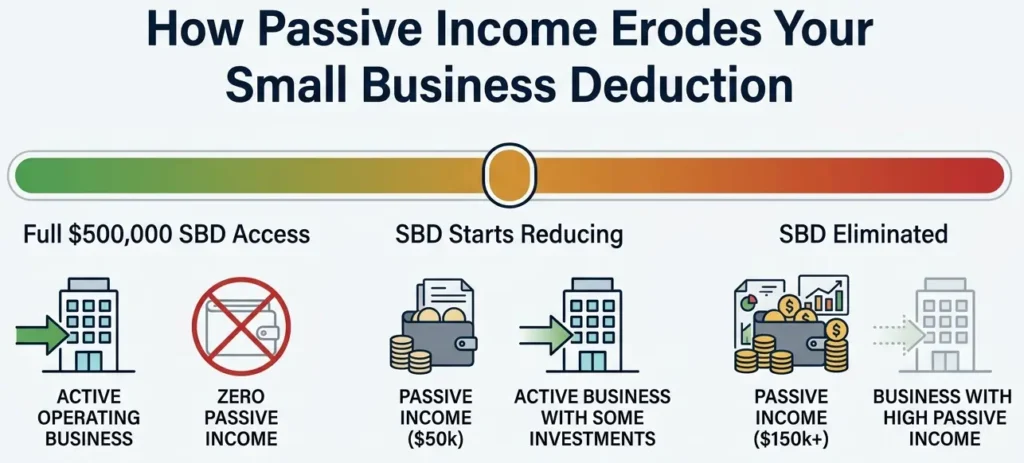

The Passive Income Grind When Your Investment Success Hurts You

Here is a rule that surprises many profitable business owners. If your corporation earns more than $50,000 in passive investment income in a year, your SBD access begins to shrink. For every dollar of passive income above $50,000, your $500,000 business limit is reduced by $5. At $150,000 of passive investment income, your SBD disappears entirely.

Keeping large investment portfolios inside your operating corporation can actively cost you, turning what feels like smart wealth-building into a real tax penalty. The practical fix is to separate investment assets into a holding company, leaving the operating corporation focused on active business income.

Tax Treatment by Business Type

Not all profitable businesses face the same rules. Here is how the most common high-margin business types are treated under Canadian tax law.

| Business Type | Key Tax Rule | Primary Risk | Recommended Strategy |

| Consulting | PSB classification risk | Loss of SBD | Multiple clients, independent operations |

| Coaching | Often flagged as PSB | High CRA scrutiny | Strong branding, contract structure |

| Tech / SaaS | Active income eligible | Scaling past $500K | Retained earnings and reinvestment |

| Real Estate | Active vs. passive split | Passive income SBD grind | Holdco structure and operational scale |

| Digital Services | Generally active income | Association rules | Careful structure across entities |

Each category is covered in detail in the sections below. Use this table as your orientation map, then read the relevant section for your situation.

The Personal Services Business Trap

This is the most expensive mistake a Canadian consultant, coach, or contractor can make, and it is easier to fall into than most people think.

A Personal Services Business (PSB) is what the CRA calls a corporation that looks like an employment relationship in disguise. If you are incorporated but providing services to a single client in a way that resembles an employee-employer relationship, the CRA can reclassify your corporation as a PSB. The Small Business Deduction disappears entirely, and your income is taxed at the full corporate rate, typically 28% federally before provincial rates are added.

How the CRA Defines a Personal Services Business

The test is whether you would reasonably be considered an employee of the client if the corporation did not exist. Factors that raise the PSB flag include having a single primary client, working exclusively at the client’s location, operating under the client’s direction and control, and not carrying on business independently. Coaches and consultants are flagged more than almost any other business type, particularly when working in long-term retainer arrangements with one organization.

How to Protect Your SBD as a Coach or Consultant

You do not need dozens of clients; you need to demonstrate genuine independence. Practical steps that strengthen your position include working with multiple clients throughout the year, maintaining your own workspace, controlling your own schedule and methods, holding business insurance, and marketing your services under your own brand. Contracts that emphasize deliverables and outcomes rather than hours worked under direction hold up much better under CRA scrutiny.

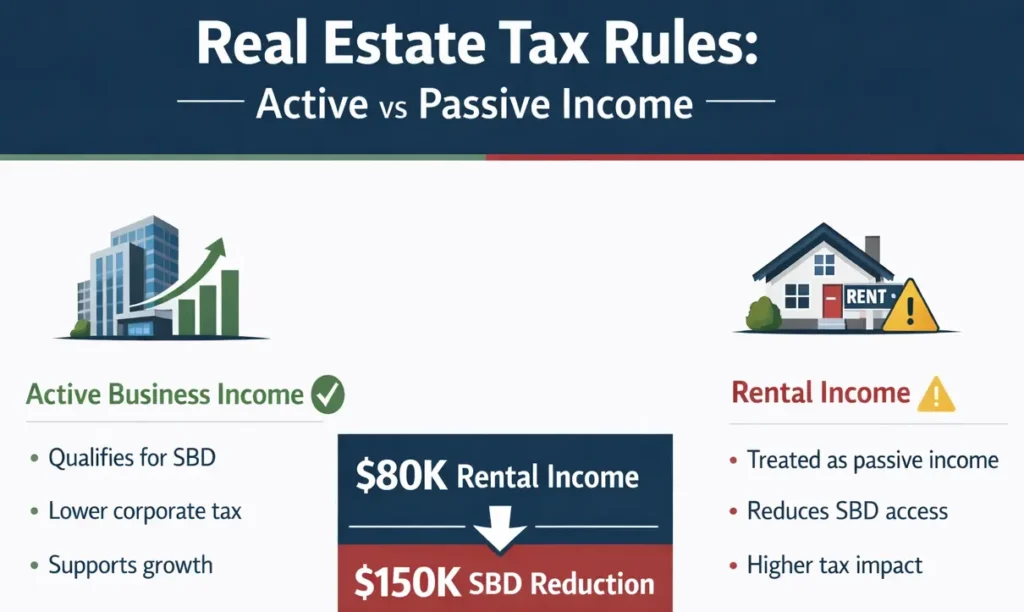

Real Estate Business Tax Rules: Active vs. Passive

Real estate is profitable. It is also one of the more complicated areas of Canadian tax, because the treatment of income depends heavily on what you are doing and how much of it.

Rental income is generally treated as passive income, not active business income. That means it does not qualify for the SBD, and it drags down your SBD access on other income through the passive income grind. A CCPC earning $80,000 in net rental income will see its $500,000 business limit reduced by $150,000, a real cost if you also run an active business inside the same corporation.

Active Real Estate: When It Qualifies Differently

Property management at scale, real estate development, and businesses that actively provide services to tenants can qualify as active business income. Courts have generally looked at whether the owner is materially involved and whether the operation has the character of a business rather than a passive investment. The practical answer for most real estate investors is structural: keep rental properties in a separate holding corporation so your operating company’s SBD eligibility is protected.

How to Pay Yourself: The Salary vs. Dividends Decision

Every profitable Canadian business owner faces this question, and there is no universal answer, but there is a clear framework for making the right call.

Salary is deductible to the corporation, reducing corporate taxable income. You pay personal income tax on it, contribute to CPP, and build RRSP contribution room (18% of earned income, up to $33,810 for 2026). It shows up on a T4, which simplifies mortgage applications and credit qualification.

Dividends are paid from after-tax corporate profits. They are taxed at a preferential personal rate through the dividend tax credit. No CPP contributions are required, saving roughly $8,860 in combined employer-employee contributions annually. But dividends do not create RRSP room and can complicate mortgage applications.

When Salary Wins

Take salary when you need RRSP contribution room, want to build CPP entitlement for retirement, are qualifying for a mortgage or major credit facility, or your corporation’s income is well above the SBD limit.

When Dividends Win

Dividends make more sense when your personal income is already moderate and the dividend tax credit brings your effective rate down meaningfully, when your corporation has built a General Rate Income Pool allowing eligible dividends at lower rates, or when you want to reduce payroll complexity in the short term.

The Blend Most Accountants Recommend

Most incorporated business owners benefit from a combination: a base salary sufficient to generate meaningful RRSP room and CPP participation, topped up with dividends as the business generates profit above personal needs. A commonly modeled approach is $70,000 to $80,000 in salary, with the remainder as dividends. Your exact number depends on province, personal tax situation, and how much you plan to retain for future reinvestment.

Real-World Tax Scenarios for Canada’s Most Profitable Businesses

Scenario 1. Consultant earning $300,000 in corporate income.

The full amount qualifies for the SBD, with a combined rate of approximately 12.2% in Ontario. The key risk is PSB classification. With multiple clients and independent operations, the SBD is protected. A blended salary and dividend strategy extracts personal income efficiently while retaining earnings in the corporation for growth.

Scenario 2. Tech founder earning $800,000 in active income.

The first $500,000 is taxed at the SBD rate. The remaining $300,000 is taxed at the general combined rate of approximately 26.5% in Ontario. The priority shifts to reinvesting retained earnings using the Accelerated Investment Incentive to write off technology assets faster, and considering a holding company structure to manage surplus.

Scenario 3. Real estate investor with $120,000 in annual rental income.

Passive income at this level triggers the SBD grind. If this investor also runs an active business in the same corporation, the $500,000 business limit is significantly reduced. The fix is structural: separate the rental portfolio into a holding company so the operating corporation’s SBD eligibility is fully preserved.

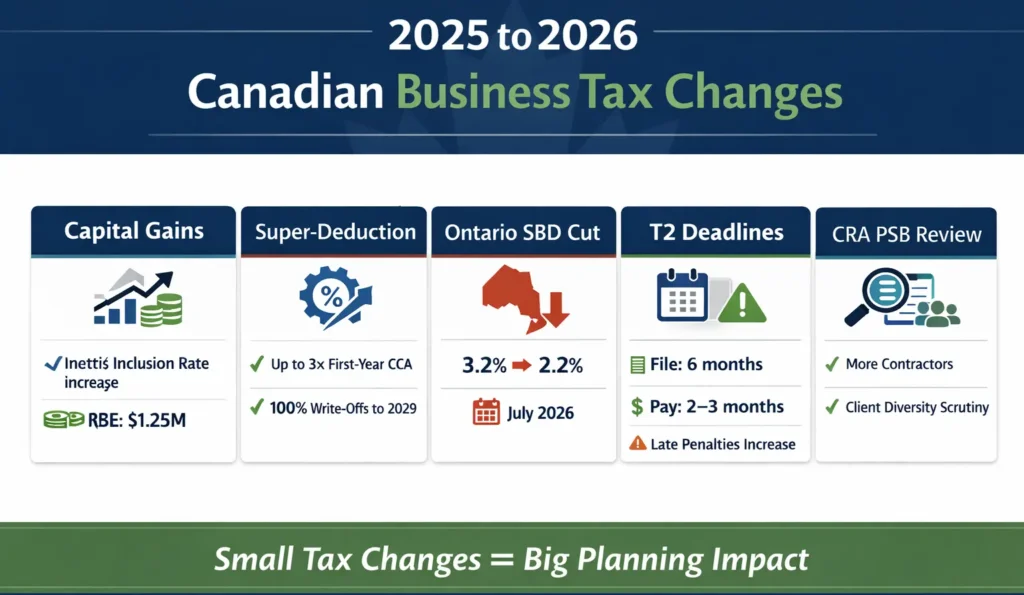

2025 to 2026 Tax Changes Every Profitable Canadian Business Must Know

Several changes are active now and directly affect planning decisions for incorporated businesses.

Capital gains inclusion rate stays at 50%

The proposed increase to 66.7% was cancelled. Half of any capital gain remains the taxable amount, preserving the value of existing strategies around business sales, estate freezes, and the Lifetime Capital Gains Exemption. The LCGE increased to $1,250,000 and is indexed for inflation going forward.

Productivity Super-Deduction is active

For assets acquired on or after January 1, 2025, businesses can claim up to three times the normal first-year Capital Cost Allowance deduction on most capital additions. Manufacturing equipment, clean energy assets, and zero-emission vehicles qualify for 100% immediate write-off through 2029.

Ontario SBD rate drops in July 2026

The Ontario small business deduction rate drops from 3.2% to 2.2% effective July 1, 2026, a real reduction worth factoring into current planning.

T2 filing and payment deadlines

Corporations must file a T2 return within six months of their fiscal year-end. Payment is due within two months for most corporations, and three months for qualifying CCPCs. Late-filing penalties start at 5% of the balance owing, plus 1% per month for up to 12 months. Prior late filers can see those penalties double.

PSB enforcement is increasing

The CRA is applying heightened scrutiny to incorporated professionals in 2025. Contract structure, client diversity, and operational independence are all under closer review.

Data and Findings

According to patterns observed across Unleash Your Power’s 2026 business coaching client engagements, the majority of incorporated entrepreneurs have never had a structured conversation with their accountant about PSB risk, passive income grind thresholds, or salary-dividend optimization.

Among those who worked through a deliberate tax clarity process as part of their business planning, the results were consistent. Business owners who separated operating and investment income across entities preserved full SBD access, keeping their effective corporate rate under 13% rather than paying general rates above 26%.

Entrepreneurs who implemented a blended salary-dividend strategy reported stronger outcomes on mortgage applications and retirement savings compared to those relying entirely on dividends. Business owners who addressed tax structure before crossing the $500,000 SBD threshold had significantly more retained capital available for reinvestment and development.

The cost difference between an unstructured and a structured approach routinely exceeded $30,000 to $60,000 annually for businesses earning between $300,000 and $800,000 in corporate income. You can read more of these transformation stories on the Unleash Your Power testimonials page.

One client, Darren G., came to James feeling stuck despite running a profitable business. He had strong revenue but no structure, and the numbers were not working the way they should. After working through both the limiting beliefs holding him back and the practical business decisions that needed changing, Darren described radical shifts in his thinking, his actions, and his financial results. Tax clarity and business clarity, it turns out, often come from the same conversation.

Who Should Use This Guide?

This guide is for you if you are an incorporated Canadian business owner earning consistent active business income, a consultant, coach, tech entrepreneur, or real estate operator trying to understand which rules apply to your specific situation, a sole proprietor considering incorporation who wants to understand what the structure actually gains you, or an entrepreneur approaching the $500,000 SBD threshold who needs to plan for what comes next.

It is also useful if you advise small business owners and want a clear overview of the rules across business types.

Who Should Get Professional Tax Advice Now?

Some situations need more than a guide. Connect with a qualified tax professional immediately if you are earning over $400,000 in corporate income and have not reviewed your PSB exposure, if you are holding investment assets inside your operating corporation, if you have multiple corporations or are planning to add one, if you are approaching a business sale and have not structured around the Lifetime Capital Gains Exemption, or if you have been paying yourself entirely through dividends for several years without modeling the RRSP and CPP impact.

The cost of getting these decisions wrong compounds over the years. The cost of a good tax advisor is typically recovered in the first conversation. If you need help thinking through your business structure and growth strategy, start there.

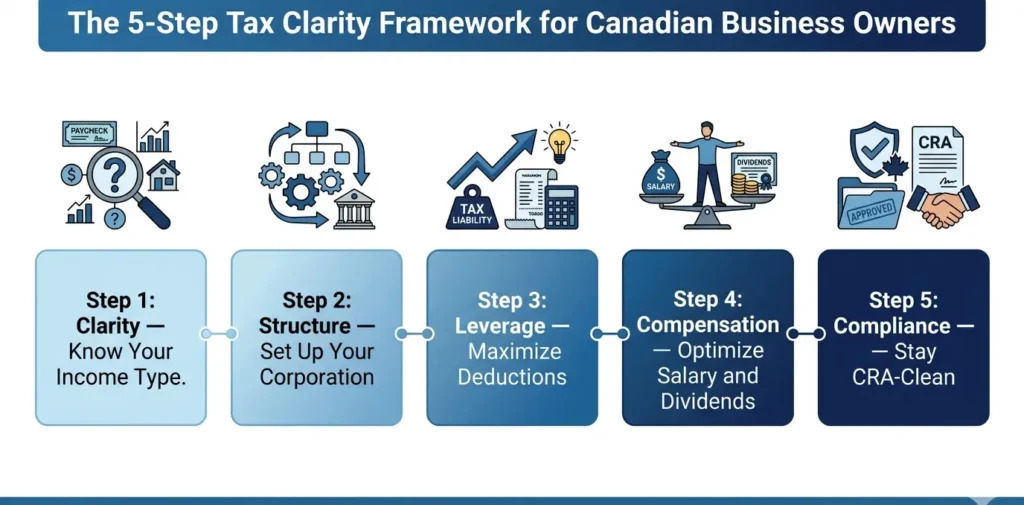

The 5-Step Tax Clarity Framework

Most profitable businesses in Canada are not paying too much tax because the rates are too high. They are paying too much because they have not built a clear structure. Here is the framework James uses with business coaching clients to bring real clarity to their financial picture.

Step 1. Clarity: Know Your Income Type.

Identify whether your corporate income is active business income, passive investment income, or a mix of both. This single distinction determines which tax rates apply and whether you access the SBD. Without this clarity, every other decision is guesswork. Understanding how much profit your business should actually keep starts with knowing what type of income you are generating.

Step 2. Structure: Set Up Your Corporation Correctly.

Confirm your operating corporation qualifies as a CCPC. If you hold investment assets or rental properties, separate them into a holding company. If you have associated corporations, understand how they share the $500,000 limit. Structure needs review as your business grows, not just when you first incorporate.

Step 3. Leverage: Use Every Deduction Available.

Maximize the SBD before crossing the $500,000 threshold. Use the Productivity Super-Deduction for any qualifying capital purchases. Claim all legitimate business expenses. Explore smart reinvestment strategies to make retained earnings work harder inside your corporation.

Step 4. Compensation: Optimize Your Salary and Dividends.

Run the numbers on a blended compensation model annually. Your ideal mix changes as corporate income changes and as your personal financial goals evolve. The goal is not to minimize corporate tax in isolation; it is to minimize total tax paid across both the corporation and your personal return.

Step 5. Compliance: Stay Clean with the CRA.

File your T2 on time. Maintain proper corporate records, including board minutes for dividend declarations. If you pay family members through the corporation, make sure compensation is reasonable and documented. If you have had shareholder loans outstanding, clear them before they become deemed income. In my 20+ years working with entrepreneurs, the businesses that grow cleanly are the ones that treat compliance as part of strategy, not an afterthought.

Frequently Asked Questions

What is the corporate tax rate for small businesses in Canada?

CCPCs pay a combined federal and provincial corporate tax rate of approximately 9% to 13% on the first $500,000 of active business income, depending on the province. In Ontario, the combined SBD rate is currently 12.2%. Income above the $500,000 threshold is taxed at the general combined rate of 23% to 31%.

What is the Small Business Deduction and who qualifies?

The Small Business Deduction (SBD) is a federal tax reduction that lowers the corporate tax rate from 15% to 9% on the first $500,000 of active business income for qualifying CCPCs. To qualify, your business must be a private corporation resident in Canada, controlled by Canadian residents, earning active business income, and not classified as a Personal Services Business. The $500,000 limit is shared across all corporations the CRA considers associated.

Can a Canadian coaching or consulting business lose the Small Business Deduction?

Yes. If the CRA classifies your corporation as a Personal Services Business, you lose the SBD entirely. A PSB is a corporation through which you deliver services to a single client in a way that resembles employment. To protect your SBD, demonstrate genuine business independence: multiple clients, your own workspace, your own branding, and contracts that focus on deliverables rather than hours worked under direction.

Is rental income from real estate active or passive for tax purposes?

Rental income from real estate held inside a corporation is generally treated as passive income by the CRA. It does not qualify for the Small Business Deduction, and if it exceeds $50,000 in a year, it begins reducing the SBD available on your other active business income. Most accountants recommend holding investment properties in a separate holding corporation to protect the operating company’s SBD eligibility.

Is it better to pay yourself a salary or dividends as a Canadian business owner?

There is no single right answer. The optimal approach depends on your corporate income level, personal financial goals, RRSP room, CPP objectives, and province. Most incorporated business owners benefit from a blended approach: a base salary to build RRSP room and CPP participation, with dividends used for flexibility and potential rate advantages above that baseline.

Build a Business That Keeps What It Earns

The tax rules for Canada’s most profitable businesses are specific, knowable, and manageable, but only when you understand which ones apply to your situation. Most business owners are leaving money on the table not because the rules are stacked against them, but because no one has walked them through their actual structure with fresh eyes.

In over 20 years working with entrepreneurs and business leaders, I have seen this pattern more times than I can count: strong revenue, real potential, and a nagging sense that the numbers should be working better. The right structure, combined with the right mindset and strategy, changes that picture fast.

If you are ready to build a business that keeps more of what it earns, connect with a business coach in Toronto or explore how business coaching at Unleash Your Power can help you take decisive action. Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.