The Bank of Canada held its overnight interest rate at 2.25% through January 2026, pausing after nine cumulative cuts since mid-2024. But Canada’s major banks are sharply divided on what comes next, some forecasting further cuts, others projecting hikes by year-end, with the outcome tied heavily to US-Canada trade negotiations.

Key Takeaway:

- Interest rate uncertainty in 2026 (Bank of Canada at 2.25% with mixed forecasts from major banks) will create cash flow pressure for Canadian small businesses with variable-rate debt or pandemic-era loans, especially amid US tariff risks and CUSMA review. [1]

- Variable rates expose businesses to payment swings, while high-leverage, low-margin companies with thin cash reserves face the highest risk of strain or insolvency. Fixed rates offer predictability but may cost more if rates fall further. [1]

- Action steps: Audit all debts, model cash flow under different rate scenarios (hold, cut, or rise), refinance proactively 6–12 months before maturity from a position of strength, build 3+ months of operating reserves, and prepare a “Debt Clarity Brief” for lender negotiations. [2]

- Use the 5-Step Debt Clarity Framework: Audit debts → Analyze scenarios → Act on highest-impact moves → Align with lenders/accountants → Review quarterly. Fixed rates suit seasonal or tight-margin businesses; variable may work for stable cash-flow operations. [2]

Bottom Line: Don’t try to predict exact 2026 rates—focus on debt clarity, cash reserves, and proactive refinancing. Businesses that audit their debt and negotiate from strength will turn rate uncertainty into a strategic advantage rather than a threat.

For small business owners, that uncertainty is the real problem. If you’re carrying variable-rate loans, lines of credit tied to prime, or pandemic-era debt that was never restructured, every rate shift directly affects your cash flow. The practical response isn’t to predict where rates go; it’s to audit your current debt structure, evaluate refinancing proactively, choose the right fixed/variable mix for your revenue profile, and open conversations with lenders before pressure builds.

The businesses that navigate 2026 successfully won’t be the ones who guessed the rate path correctly. They’ll be the ones who made decisive decisions about their debt.

What’s Actually Happening With Canadian Interest Rates in 2026

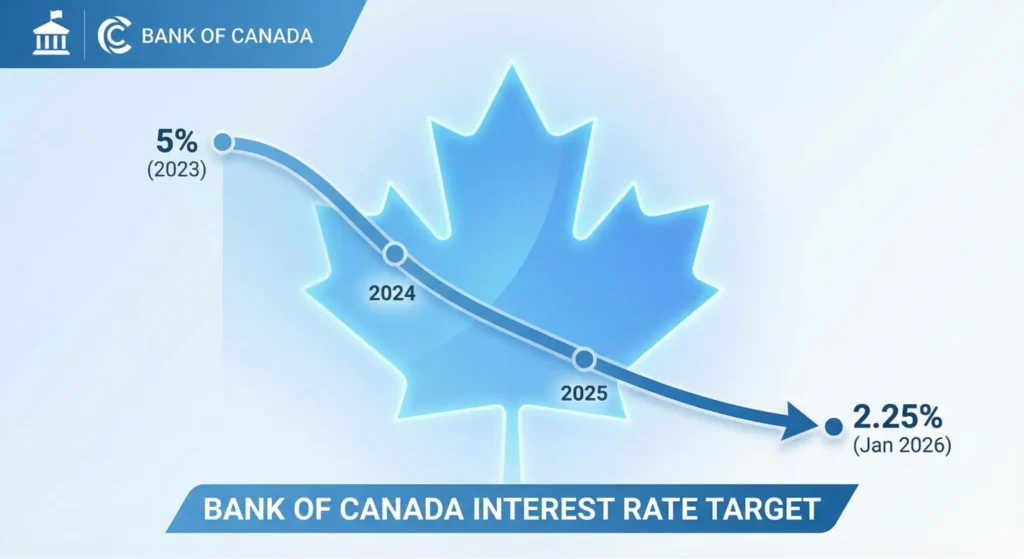

After cutting its benchmark rate nine times between June 2024 and October 2025, a total reduction of 275 basis points, the Bank of Canada held steady at 2.25% in its January 2026 meeting. The central bank flagged significant uncertainty, noting that ongoing US tariff threats and the upcoming CUSMA review make the direction of future moves genuinely difficult to predict.

Canada’s major banks reflect that uncertainty in sharply divergent forecasts. The Big Six are split on the 2026 rate path: BMO sees the rate falling further, potentially to 1.75%, to support a sluggish economy. Scotiabank expects a hike back toward 2.75% if inflation accelerates. CIBC believes the Bank should cut further but predicts it will hold. RBC and TD both project an extended pause through much of 2026.

The takeaway for every small business owner: plan for a range of outcomes, not a single rate path. Build your debt strategy around your cash flow reality, not where you think rates might land.

How Rate Uncertainty Is Hitting Canadian Small Business Debt Right Now

Canadian small businesses are navigating compound pressure: elevated borrowing costs layered on top of tariff-driven expense increases. According to research from the Canadian Federation of Independent Business (CFIB), 63% of SMEs report higher costs directly linked to US tariffs, 53% have seen reduced profits, and 79% say unpredictable trade and monetary policy is a direct barrier to planning.

The lending picture adds further pressure. Canada’s prime rate sits at 4.45%, significantly lower than 2023 peaks, but still far above the pandemic-era lows many owners used to structure their original debt. The Bank of Canada’s own financial stability research identifies businesses with high leverage, low profitability, and thin cash reserves as those facing the greatest insolvency exposure in the current environment.

Many owners are still carrying pandemic-era debt that was always meant to be a temporary structure. In 2026, “getting around to it” is no longer a low-risk approach.

Should You Refinance Your Business Loan in 2026?

This is the question most small business owners are circling and the honest answer is: it depends on your numbers, not the headlines.

Refinancing makes sense when you can meaningfully reduce your cost of capital, improve cash flow predictability, or extend your repayment timeline without draining liquidity. Debt financing strategists at Cerebro Capital are clear on timing: start the refinancing process 6 to 12 months before your loan matures. Negotiating from a position of financial strength always produces better terms than refinancing under pressure. Waiting until the last minute gives leverage to your lender.

The critical distinction every business owner needs to understand: refinancing is opportunistic; it’s something you do when you’re in a position of strength. Restructuring is defensive; it’s what happens when options narrow. If your business is performing well and rates are genuinely lower than what you locked in previously, refinancing can reduce total interest expense and free up working capital. If you’re already under cash flow pressure, you’re moving into restructuring territory, which requires a different conversation entirely.

Try This: Run a side-by-side 12-month cash flow projection: your current loan structure versus a refinanced scenario. Compare total interest paid, the change in monthly payment, and remaining liquidity after each option. Numbers clarify what emotion cannot.

Fixed vs. Variable Rate: Which Side Should You Be On in 2026?

With Canada’s prime rate at 4.45% and forecasts running in every direction, the fixed vs. variable decision comes down to one core question: how much payment volatility can your business genuinely absorb? True North Mortgage’s 2026 rate analysis shows variable rates currently sitting roughly 49 basis points below five-year fixed equivalents, a meaningful difference on large loan balances. But that spread disappears quickly if rates move upward.

| Fixed Rate | Variable Rate | |

| Payment predictability | High same payment every month | Low changes with prime rate movements |

| Best for | Seasonal revenue, tight margins | Stable revenue, strong cash buffer |

| 2026 rate risk | May overpay if rates fall further | Exposure if rates rise (Scotiabank hike scenario) |

| Planning advantage | Budget with certainty for 12+ months | Lower entry cost; flexibility if rates drop |

| Current spread (Jan 2026) | ~49 bps above the current variable rate | Lower entry point; higher payment sensitivity |

For businesses with tight margins or revenue that fluctuates seasonally, retail, hospitality, and construction predictability has real dollar value. A slightly higher fixed rate that lets you plan hiring, inventory, and payroll with full confidence is often the smarter business decision, regardless of what the rate comparison shows on paper. As the BDC’s guide to fixed vs. variable lending puts it: if rate variations would seriously impact your financial viability, a fixed rate is the responsible choice.

How to Negotiate With Your Lender (Before You Miss a Payment)

One of the most underused tools in a small business owner’s toolkit is the direct, proactive conversation with your lender before things get critical.

Canada’s Business Development Bank (BDC) is explicit about what lenders actually want: businesses that know their situation, have a clear turnaround plan, and approach the conversation before a payment is missed. Coming to your bank with a realistic proposal and solid numbers puts you in a fundamentally different position than calling in distress.

The Canadian Association of Insolvency and Restructuring Professionals (CAIRP) advises business owners to maintain open communication with creditors and operate transparently, including suppliers and trade creditors, not just banks. Options your lender may agree to when approached proactively include: extending your amortisation period, deferring principal payments temporarily, switching rate structure (fixed to variable or vice versa), or consolidating multiple debts into a single, more manageable facility.

Try This: Before your next lender meeting, prepare a one-page “Debt Clarity Brief” with three short paragraphs covering: (1) the source of the cash flow pressure, (2) your plan to address it, and (3) the specific ask you’re making. A lender who sees a business owner in control of their narrative is far more likely to say yes.

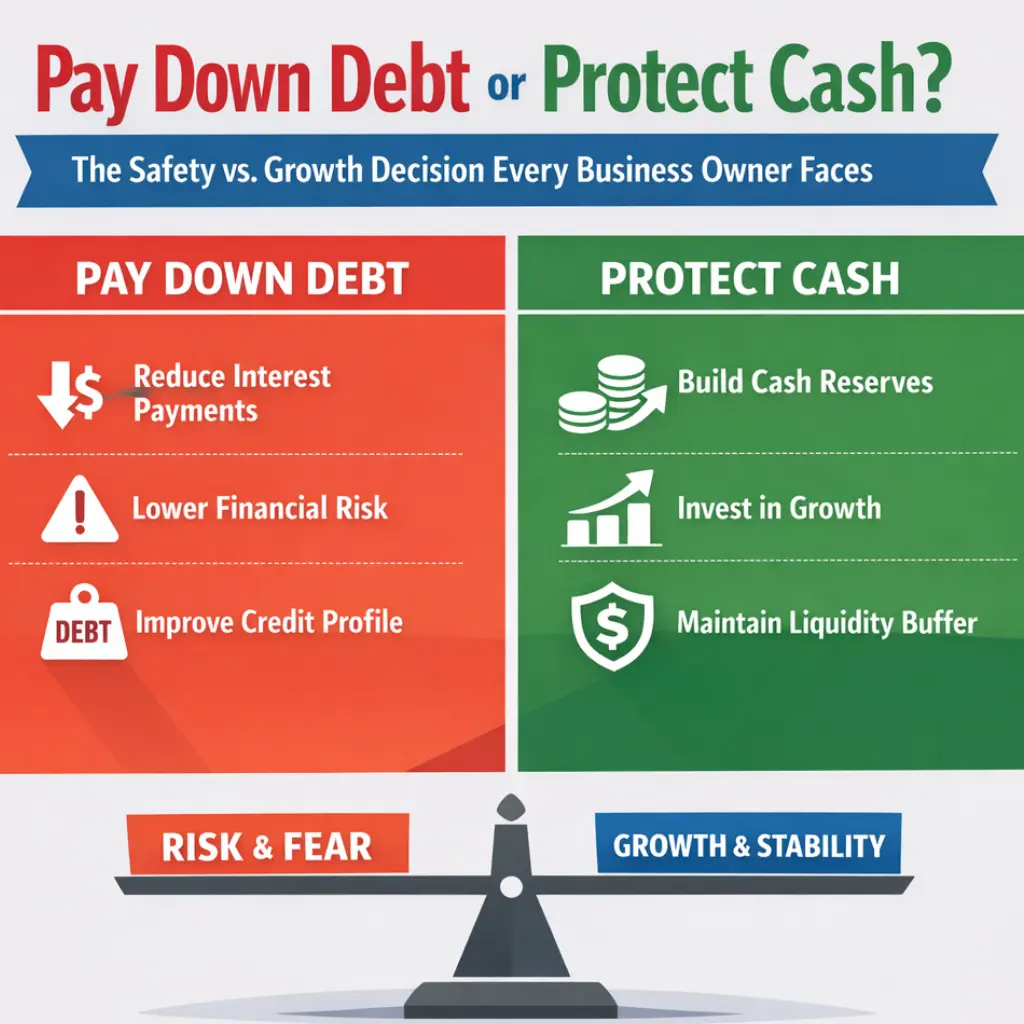

Pay Down Debt Faster or Protect Cash? (The Safety vs. Growth Question)

This is where smart financial math and business psychology collide and where many owners unknowingly make fear-based decisions that slow their growth far more than the debt itself.

Here’s the logic trap: paying down debt aggressively feels responsible. It reduces interest expense, strengthens your balance sheet, and improves your leverage ratios. All true. But draining working capital to eliminate debt faster than required also kills your flexibility, your ability to absorb a slow month, fund a strategic marketing push, or move quickly on an unexpected opportunity. Liquidity is your growth fuel. Without it, you’re debt-free and stuck.

In over 20 years of working with business owners, James has seen this pattern consistently: founders who carry what might be called a “debt-weight” goal block a fear-based relationship with money that drives them to optimise for safety rather than growth.

One client, Darren G., came to James feeling completely blocked in his business despite hard work and a solid track record. Through their work together, Darren discovered that his financial decisions were being driven by scarcity thinking rather than strategic clarity. He wasn’t choosing to pay down debt because the math said so; he was choosing it because debt felt dangerous, and eliminating it felt like relief.

Once Darren could separate what was logically sound from what was fear-driven, his actions and his results shifted radically. The key question isn’t just “Should I pay down debt or protect cash?” It’s “Am I making this decision from clarity or from fear?”, and being honest about the answer.

The practical rule: build a cash reserve covering at least three months of operating expenses before accelerating debt repayment. If you have that buffer, put extra cash toward your highest-interest debt first. If you don’t yet have that buffer, building it takes priority over acceleration. As Simpli Bookkeeping’s 2026 small business debt strategy analysis notes plainly, cash flow forecasting in 2026 is no longer optional. It is the foundation of responsible borrowing.

Warning Signs Your Business Debt Is Getting Dangerous

Not all debt pressure announces itself loudly. These are the signals to watch:

- You’re using your line of credit to cover regular operating expenses, not to bridge a timing gap, but as routine funding

- Debt service costs are consuming more than 30–40% of your gross revenue on a consistent monthly basis

- You haven’t modelled what a 0.5% rate increase would do to your monthly cash flow obligations

- You’re avoiding conversations with your accountant or lender because you don’t want to see the numbers

- Your cash reserve has dropped below one month of operating expenses

Any one of these signals warrants immediate attention. Two or more means your debt structure needs a dedicated review, not next quarter, now. Understanding why small businesses fail to grow often reveals the same financial patterns at the root and the same clarity-driven decisions that resolve them.

The 5-Step Debt Clarity Framework

Most business owners approach debt reactively, responding to problems as they surface instead of managing structure proactively. This framework changes that. Use it to build a living debt strategy that holds up regardless of what rates do.

| Step | Action | What It Produces |

| 1. Audit | List every debt: type, rate (fixed/variable), maturity date, and monthly payment | A complete debt map, no surprises at renewal |

| 2. Analyse | Model cash flow under three scenarios: rate holds/cuts 0.5% / rises 0.5% | A stress-tested picture of your real exposure |

| 3. Act | Identify the single highest-impact move: refinance, negotiate, or consolidate | A clear priority, not a sprawling to-do list |

| 4. Align | Brief your lender, accountant, and key business partners on the plan | Shared direction with everyone who needs to know |

| 5. Advance | Set a 90-day review cadence to reassess debt structure as conditions shift | A living debt strategy, not a one-time fix |

This five-step process draws directly on Pillar 1 Clarity of Vision from the Unleash Your Power framework. Clarity about your debt position isn’t just a financial win. It’s a leadership win. Decisive owners who see their debt structure clearly make better financial decisions than reactive ones, every single time. For a deeper look at the mindset that drives this kind of strategic action, explore smart reinvestment strategies for your business and how high-performance entrepreneurs think about capital allocation.

Data & Findings

According to Olympia Benefits research cited by Swoop Funding, Canadian SMEs collectively carried approximately $1.7 trillion in outstanding debt as of late 2022, much of it accumulated during the pandemic period. That debt hasn’t disappeared from the balance sheets of Canadian businesses.

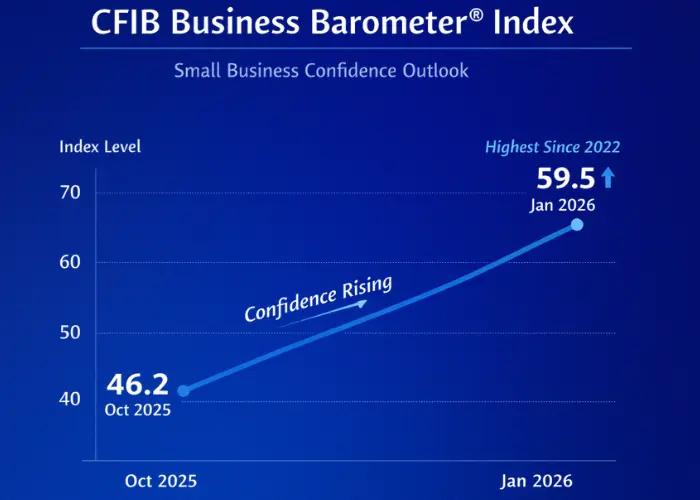

The CFIB Business Barometer rose to a near three-year high of 59.9 in December 2025 before settling at 59.5 in January 2026. Long-term optimism is present, but short-term confidence remains subdued across all provinces, reflecting the real economic uncertainty heading into the year.

79% of Canadian business owners report that unpredictable policy environments directly block business planning (CFIB). Bank of Canada financial stability research confirms that businesses combining high leverage, low profitability, and thin cash reserves carry the greatest insolvency risk in the current environment.

Knowing how much profit your business should retain as a buffer is directly tied to debt resilience. See our breakdown of how much profit a small business should keep, including the reserves that insulate you from rate volatility.

Who Should Use This Framework?

This approach is built for:

- Owners carrying variable-rate loans or prime-linked lines of credit with no rate-scenario modelling in place

- Businesses still carrying pandemic-era loans that were meant to be short-term structures

- Entrepreneurs in tariff-sensitive sectors, such as manufacturing, retail, food service, and construction, where margins are already compressed

- Any owner planning to refinance or renew a major credit facility within the next 12 months

If your debt situation is already stable and you’ve modelled your rate exposure, you’re ahead of the curve. Use this framework to lock in a 90-day review cadence and maintain that advantage. For context on the right banking infrastructure to support your strategy, see our guide to the best bank accounts for Canadian small businesses.

Who Should Consider Professional Help Instead?

If debt service is consistently consuming more than 50% of gross revenue, or if you’ve already missed payments or breached loan covenants, informal negotiation may not be enough. Two resources are purpose-built for this situation:

- BDC Advisory Services: Canada’s Business Development Bank offers restructuring guidance and specialised financing for businesses in difficulty, with advisors experienced in exactly this kind of turnaround work

- A Licensed Insolvency Trustee (LIT): A federally regulated professional who can guide you through formal restructuring options under Canadian insolvency legislation, including options that protect your business while restructuring its obligations

Reaching out for professional help early is a sign of strong leadership, not failure. The sooner you engage the right expertise, the more options remain on the table.

Take Decisive Control of Your Debt Strategy

Interest rates in 2026 are uncertain. Your debt decisions don’t have to be.

The business owners who look back on 2026 as a turning point will be the ones who used the uncertainty as a reason to get clear about their debt structure, model their rate exposure, and make deliberate choices rather than reactive ones. That clarity is available to you right now. It starts with an honest look at your numbers and the willingness to act on what you find.

If you’re ready to harness decisive financial leadership and master the mindset that drives it, James R. Elliot’s business coaching programs are built exactly for this moment. With 20+ years of guiding entrepreneurs from financial anxiety to confident, strategic action, James delivers the proven tools that make transformation real. Explore your goal-setting framework for business growth and take the first step today.

Unleash Your Power: Stand Out, Take Action, and Create the Success You Want.

Frequently Asked Questions

What is the Bank of Canada’s current interest rate in 2026?

The Bank of Canada held its overnight rate at 2.25% following its January 28, 2026, decision, pausing after nine consecutive cuts between mid-2024 and October 2025. The central bank flagged that the direction of future moves is genuinely uncertain, with the CUSMA trade agreement review and ongoing US tariff dynamics as the key variables. The next scheduled rate announcement was set for March 18, 2026.

How do rising interest rates affect small business loans in Canada?

Rising rates directly increase the cost of any variable-rate business debt, including loans tied to the prime rate (currently 4.45%) and revolving lines of credit. For businesses with large balances, a 0.25% rate increase meaningfully raises monthly payments and reduces available working capital. Fixed-rate loans aren’t affected during their term but will reprice at renewal, making proactive scenario modelling critical before that date arrives.

When does it make sense to refinance a small business loan in Canada?

Refinancing makes the most sense when you can lower your effective interest rate, extend amortisation to improve your monthly cash flow, or consolidate multiple debts into a single facility and when you’re approaching the conversation from financial stability rather than distress. Starting 6 to 12 months before your current loan matures gives you the most negotiating leverage and the broadest range of options.

Should Canadian small businesses choose fixed or variable rate loans in 2026?

For businesses with seasonal revenue, tight margins, or uncertain cash flow, a fixed rate provides planning certainty that typically outweighs a slightly higher entry rate. For businesses with stable, predictable revenue and a healthy cash buffer, a variable rate may still deliver cost savings, particularly given the current 49-basis-point spread below five-year fixed rates. The right choice depends on your specific cash flow profile and risk tolerance, not on rate predictions.

What are my options if my business is struggling to repay debt in Canada?

Before you miss a payment, speak directly with your lender. Most creditors will negotiate adjusted terms, extended amortisation, deferred principal, or a rate structure change when approached proactively with a clear plan. If informal negotiation isn’t sufficient, Canada’s Business Development Bank (BDC) offers advisory services and restructuring financing, and a Licensed Insolvency Trustee (LIT) can guide you through formal restructuring options under Canadian insolvency legislation.